New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

auditing

Auditing and Assurance Services 6th edition Timothy Louwers, Robert Ramsay, David Sinason, Jerry Straws - Solutions

Assume that Stanford CPAs encountered the following issues during its various audit engagements in 2014: 1. It conducted the audit of Luck, a new client this past year. Last year, Luck was audited by another CPA, who issued an unmodified opinion on its financial statements. Luck is presenting

For each of the following situations, indicate the type of opinion(s) that auditors could issue (more than one opinion may be appropriate in each circumstance). Unless otherwise noted, assume that no departures from GAAP were identified in the audit engagement. In addition, indicate how the

On September 23, 2015, Betsy Ross drafted the following report on Continental Corporation’s financial statements.To Whom It May Concern: We have audited the accompanying financial statements of Continental Corporation, which comprise the balance sheet as of July 31, 2015, and the related

Adverse Opinion. The board of directors of Cook Indus-tries Inc. engaged Brown & Brown, CPAs, to audit the financial statements for the year ended December 31, 2014. Required: Identify the deficiencies in the following draft of the report. Do not rewrite the report.Independent Auditor’s Report

Comparative Reporting. An assistant drafted the following auditors’ report at the completion of the audit of Cramdon Inc. on March 5, 2015. The partner in charge of the engagement has decided the opinion on the 2014 financial statements should be modified only with reference to the change in the

Audit Report Deficiencies: Audits of Group Financial Statements and Other Operating Matters. Following is Rex Wolf’s report on Bonair Corporation’s financial statements. Bonair publishes general- purpose financial statements for distribution to owners, creditors, potential investors, and the

Your partner drafted the following auditors’ report yesterday. You need to describe the reporting deficiencies, explain the reasons for them, and discuss with the partner how the report should be corrected. You have decided to prepare a three- column worksheet showing the deficiencies, reasons,

Audit Report Deficiencies: Accounting Change and Uncertainty. The following auditors’ report was drafted by Quinn Moore, a staff auditor with Tyler & Tyler, CPAs, at the completion of the audit of the financial statements of Park Publishing Company for the year ended September 30, 2014. The

Internet Exercise: Reports on Financial Statements (Public Companies). One of the great resources for auditors is the SEC’s Electronic Data Gathering, Analysis and Retrieval (EDGAR) system database at www.sec.gov. Public companies file SEC- required documents electronically. The SEC makes

Financial Difficulty: The “Going- Concern” Problem. Pitts Company has experienced significant financial difficulty. Current liabilities exceed current assets by $ 1 million, cash has decreased to $ 10,000, the interest on the long- term debt has not been paid, and a customer has brought a

Officers of Richnow Company do not wish to disclose information about a product liability lawsuit filed by a customer seeking $ 500,000 in damages. They believe the suit is frivolous and without merit. Outside counsel is more cautious. The auditors insist on disclosure. Angered, Richnow’s chair

Anderson, Olds, & Watershed (AOW) has completed the audit of the financial statements of Musgrave Company for the year ended December 31, 2014, and is now preparing the report. AOW has audited Musgrave’s financial statements for several years, but this year Musgrave delayed the start of the

The firm of Anderson, Olds, & Watershed (AOW) is the group auditor for the December 31, 2014, consolidated financial statements of Ferguson Company and subsidiaries. However, component auditors perform the work on certain subsidiaries for the year under audit amounting to 29% of total assets

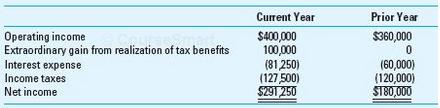

Gustav Humphreys (chair of the board) and Ingrid VanEns (vice president, finance) prepared the draft of the financial review section of the annual report. You are reviewing it for consistency with the audited financial statements. The draft contains the following explanation about income coverage

On January 1, Graham Company purchased land (the site of a new building) for $ 100,000. Soon thereafter, the state highway department announced that a new feeder road would run next to the site. The effect was a dramatic increase in local property values. Comparable land located nearby sold for $

In December of the current year, Williams Company changed its method of accounting for inventory and cost of goods sold from LIFO to FIFO. The account balances shown in the trial balance have already been recalculated and adjusted retroactively as required by ASC 250. The accounting change and the

Mini- Case: Component Auditors. Refer to the mini- case “Something Went Sour at Parmalat” on page C20 and respond to questionOn page C20There was much confusion when Italian dairy food giant Parmalat defaulted on a $ 187 million bond payment in mid- November 2002. Default on a bond payment

Mini- Case: Going- Concern Reporting. Refer to the mini- case “GM: Running on Empty†on page C11 and respond to questions 1, 2, and 3.On page C111. Reviewing GM’s financial information in GM Exhibit 1 and its stock price in GM Exhibit 2 , when do you first see signs of

To whom is the auditors’ report addressed?

What alternatives are available to auditors for reporting on the financial statements and internal control over financial reporting in the audit of public entities?

Explain the effect of pervasiveness on the auditors’ report when the entity uses an accounting method that departs from

What are the major differences in wording for qualified opinions and adverse opinions issued as a result of departures from GAAP?

What are auditors’ reporting options when going- concern uncertainties are noted?

What are comparative financial statements ? What issue is introduced when entities present information in comparative format?

What is attestation? Provide some examples of attestation engagements.

What is a responsible party? Why is it necessary for the accountant to identify one?

What are the differences among an examination, a review, and agreed- upon procedures?

Identify several points of similarity between a compliance examination and an audit of financial statements.

What is the difference between a review service engagement and a compilation service engagement regarding historical financial statements? Compare both of these with an audit engagement.

In what respects is a review of interim financial information similar to a review of the unaudited annual financial statements of a nonissuer?

Is interim financial information required to be presented by (a) U. S. GAAP and (b) SEC filing requirements?

Regarding special purpose frameworks, (a) Why do they exist and (b) Can financial statements prepared using special purpose frameworks be audited?

What are some examples of special purpose framework?

How could “opinion shopping” be (a) Suspect or (b) Helpful?

What must a CPA do when reporting on the application of requirements of an appropriate financial reporting framework?

What makes CPAs qualified to perform the assurance services discussed here?

Briefly describe the two trust services in terms of those provided and of intended customers.

What is sustainability reporting? Why would a company choose to provide a sustainability report? Why would it pay for independent assurance?

To perform an attestation engagement on prospective information or pro forma information, accountants must do all of the following except a. Obtain knowledge about the entity’s business and accounting principles. b. Understand the internal controls used in the processes that generated the

If a non-issuer wants an accountant to perform an examination of its internal controls, the accountant should follow: a. PCAOB AS 5, “An Audit of Internal Control over Financial Reporting That Is Integrated with an Audit of Financial Statements.” b. AICPA AT 501, “ An Examination of an

A review service engagement involving unaudited financial statements involves a. More work than a compilation and an audit. b. Less work than an audit but more work than a compilation. c. Less work than a compilation but more work than an audit. d. More work than an audit but less work than a

When accountants are not independent, which of the following reports can they nevertheless issue? a. Compilation report. b. Standard unmodified audit report. c. Examination report on a forecast. d. Examination of internal control over financial reporting.

For a compliance engagement, three conditions must be met. Which of the following is not one of the three conditions? a. Management accepts responsibility for compliance. b. Management’s evaluation of compliance is capable of evaluation and is measured against reasonable criteria. c. Sufficient

Accountants are permitted to express “negative assurance” in which of the following reports? a. Standard unmodified audit report on financial statements. b. Compilation report on unaudited financial statements. c. Review report on unaudited financial statements. d. Adverse opinion report on

Which of the following conditions must be met before an accountant can conduct an examination of an entity’s internal control? a. Management must present its assertion about the effectiveness of its internal control in a written report. b. Management must represent that there are no internal

When interim financial information is presented in a footnote to annual financial statements, the standard audit report on the annual financial statements should a. Not mention the interim information unless there is an exception that the auditors need to include in the report. b. Contain an

During a review of a non-issuer’s financial statements, accountants are required to make certain inquiries of management. Which of the following inquiries is not required by the SSARS? a. The basis for the preparation of financial statements. b. Internal control deficiencies. c. Significant

According to auditing standards, financial statements presented on a special purpose frame-work should not a. Contain a note describing the special purpose framework. b. Describe in general how the special purpose framework differs from generally accepted accounting principles. c. Be accompanied

To be useful, an audit of a service organization’s controls should cover a minimum of a. Three months. b. Six months. c. One year. d. The user entity’s fiscal period.

In providing assurance services to clients, CPAs are building on their reputations for a. Knowledge and integrity.b. Objectivity and integrity. c. Independence and due professional care. d. Professionalism and trust.

The AICPA Special Committee on Assurance Services identified five global “mega trends” that can affect a CPA’s business. Which of the following is not one of these mega trends? a. The decreasing supply of natural resources. b. Information technology. c. New social structures. d. Demands for

An assurance service is defined as a service that a. Provides auditing services to nonfinancial information. b. Reviews unaudited financial information. c. Improves the quality of information for decision makers. d. Reduces the risk in management decision making.

B. Harper is surfing the Internet and finds a great pair of rollerblades at a really low price but he has never heard of the company and is concerned that the product he ordered may not be the product he receives. Harper may be more willing to place an order with this company if a. The website

Which of the following is not a principle of trust services? a. Security. b. Authentication. c. Privacy. d. Confidentiality.

Which of the following statements should be included in a practitioner’s report on the application of agreed- upon procedures? a. A statement that the practitioner performed an examination of prospective financial statements. b. A statement of scope limitation that will qualify the

The official Statements on Standards for Accounting and Review Services are applicable to practice with a. Audited financial statements of public companies. b. Unaudited financial statements of public companies. c. Unaudited financial statements of non-issuers. d. Audited financial statements

Which of the following is a generally accepted attestation standard but is not a fundamental auditing principle? a. Appropriate competence and capability. b. Adequate knowledge of the subject matter. c. Independence. d. Due care.

The performance of an attestation engagement on prospective financial information does not require which of the following? a. If the basis of the prospective financial information is different than the financial statements, a reconciliation of the two must be provided. b. Management must disclose

If the auditor expresses an adverse or disclaimer of opinion on the complete set of financial statements, she or he is not permitted to: a. Express an unmodified opinion on a single financial statement. b. Express an unmodified opinion on an element of the financial statements. c. Express a similar

An accountant may allow general distribution of reports based on a. An agreed- upon- procedures engagement. b. An examination of prospective financial information. c. An examination of forecasted financial information. d. None of the above.

M. Jordan & E. Stone, CPAs, audited the financial statements of Tech Company, a non-issuer, for the year ended December 31, 2013, and expressed an unmodified opinion. For the next year, ended December 31, 2014, Tech issued comparative financial statements. Jordan & Stone reviewed Tech’s 2014

Dodd Manufacturing Corporation has engaged you to attest to the reasonableness of the assumptions underlying its forecast of revenues, costs, and net income for the next calendar year, 2015. Four of the assumptions follow. 1. The company intends to sell certain real estate and other facilities held

Internet Exercise: Reporting on Service Organization Controls. Search for a service organization auditor’s report on internal controls on the web. If you cannot find an auditor’s report, find a company’s news release describing its auditor’s service organization report. Required: a. Why do

The following numbered items 1– 10 state procedures accountants should consider in review engagements and compilation engagements on the annual financial statements of non-issuers (performed in accordance with AICPA Statements on Standards for Accounting and Review Services). Required: For each

Jimmy C. operates a large service station, garage, and truck stop on Interstate 95 near Plainview. His brother, Bill, has recently joined him as a partner, even though he will continue his small CPA practice. One slow afternoon, they were discussing financial statements with Bert, the local CPA

A. 46 Negative Assurance in Review Reports. One portion of the report on a review services engagement is the following: “ Based on my review, I am not aware of any material modifications that should be made to the accompanying financial statements in order for them to be in conformity with

The following abstracted report is a report on a trust fund that refers to a statutory basis of accounting (special purpose framework) as well as to generally accepted accounting principles (GAAP). Independent Auditor‘ s ReportTo Natalia National Bank Association (Trustee) and the Unit Holders of

Prepare a Compilation Report. The Coffin brothers have engaged you to compile their financial schedules from books and records maintained by James Coffin. The brothers own and operate three auto parts stores in Central City. Even though their business is growing, they have not wanted to employ a

A. Jones, CPA, performed a review service for the Independence Company in 2014. He wants to present comparative financial statements. However, the 2013 statements were compiled by Able and Associates, CPAs, and Able does not want to cooperate with Jones by reissuing the prior-year compilation

June’s Java provides coffee services (coffee, cups, cream, sugar, and coffee makers) to local companies for use in their offices. Each of five drivers has a truck with inventory and has a different route each day to replenish coffee sup-plies to the companies on the route. In past audits, the

Baker & Baker, CPAs, pre-pared the following report on the interim financial information of Micro Mini Company. The interim financial information was presented in the first quarterly report for the three-month period ended March 31, 2015. No comparative quarterly information of the first

Brooklyn Life Insurance Company prepares its financial statements on a statutory basis in conformity with the accounting practices pre-scribed and permitted by the Insurance Department of the State of New York. This statutory basis produces financial statements that differ materially from

Visit the AICPA WebTrust site (www. webtrust. org ).Required:a. What is WebTrust?b. Why is WebTrust needed?c. How does an Internet user know that a website has received the WebTrust service?d. Where can a person obtain copies of the Trust service principles?

In 2008, the AICPA Assurance Services Executive Committee identified five global “mega trends” that can affect a CPA’s business. Required: a. Review the mega trends that were identified. Are these trends still viable in today’s society and economy? Which trends, if any, need to be

Davis has a store that sells old baseball cards. To expand the business, he has decided to open an Internet site where potential customers can view the cards and place orders. Davis hires Johnson, who is an expert in constructing websites for small businesses. She explains that even with a quality

Henry’s Health Food Store maintains a perpetual inventory on its computer. The sales representative from A- Plus Vitamins has recommended the following to Henry: • All the files should have password protection. •A- Plus Vitamins should be given the URL and the password for Henry’s inventory

Go to the TryXBRL website (www.tryxbrl.com) and examine the sample XBRL EDGAR filing. EDGAR is the SEC’s electronic financial reporting format that allows downloads of financial reports of public companies. Required: How can CPAs provide assurance for XBRL reporting as a service to their clients?

The local high school experienced trouble two years ago. Its graduation rates had declined to the bottom 10 percent in the state, college admission rates were low, and graduates had a high unemployment rate. The school board and administration have notified the state Department of Education and the

What is a service organization? Why would it engage an auditor to report on its controls?

Why should distribution be limited for reports on projections, agreed- upon procedures, and service organizations?

Why would a client ask a CPA to report on a financial statement element?

What roles must a professional accountant be prepared to perform in regard to ethical decision problems?

When might the rule “Let your conscience be your guide” not be a sufficient basis for (a) Your personal ethical decisions and (b) Your professional ethical decisions?

Assume that you accept the following ethical rule: “Failure to tell the whole truth is wrong.” In the textbook illustration about Santos’s problem with Ellis’s instructions, (a) What would this rule require Santos to do and (b) Why is an unalterable rule such as this classified as an

In regard to ethics rules, what are the jurisdictions of the (a) AICPA PEEC, (b) SEC, (c) PCAOB, (d) IFAC?

What organizations and agencies have rules of conduct that you must observe when you practice (a) Public accounting, (b) Internal auditing, (c) Management accounting, and (d) Fraud examination?

Yolanda is the executive in charge of the Santa Fe office of Best & Co, an international public accounting firm. She is responsible for the practice in all areas of audit, tax, and consulting, but she does not serve as a field audit partner or a reviewer. Javier is the partner in charge of the

Why do you think the SEC requires companies to disclose fees paid to independent accounting firms for audit and consulting services? What must be disclosed?

What rules of conduct apply specifically to members in government and industry?

What provisions of the AICPA Council Resolution on form of organization place control of accounting services in the hands of CPAs?

What penalties can be imposed by the AICPA and the state societies on CPAs in their “self- regulation” of ethics code violators?

What penalties can the SEC and PCAOB impose on CPAs who violate rules of conduct?

Auditors are interested in having independence in appearance becausea. They want to impress the public with their independence in fact.b. They want the public at large to have confidence in the profession.c. They need to comply with the fundamental principles of GAAS.d. Audits should be planned and

Under Sarbanes- Oxley and PCAOB rules, ensuring that the auditor is independent in appear-ance is the responsibility of a. The public accounting firm. b. Senior management. c. The audit committee. d. The PCAOB.

If a public accounting firm says it always follows the rule that requires adherence to FASB pronouncements in order to give a standard unmodified auditors’ report, it is following a philosophy characterized bya. The imperative principle.b. The utilitarian principle.c. Virtue ethics.d. Reliance on

Which of the following agencies issues independence rules for the auditors of public companies? a. Financial Accounting Standards Board (FASB). b. Government Accountability Office (GAO). c. Public Company Accounting Oversight Board ( PCAOB) d. AICPA Accounting and Review

Audit independence in fact is most clearly lost when a. A public accounting firm audits competitor companies in the same industry (e. g., Coca- Cola and Pepsi). b. An auditor agrees to the argument made by the client’s financial vice president that deferring losses on debt refinancing is in

The audit committee’s responsibility for auditor independence concerns a. Ensuring that partners of the public accounting firm are not stockholders in the company. b. Ensuring that nonaudit services provided by the auditor do not impair independence. c. Reporting on auditor independence to the

AICPA members who work in industry and government must always uphold which two of the following AICPA rules of conduct? a. Rule 101— Independence. b. Rule 102— Integrity and Objectivity. c. Rule 301— Confidential Client Information. d. Rule 501— Acts Discreditable.

A public accounting firm’s independence is not impaired when members of the audit engagement team does which of the following for a public company audit client? a. Prepares special purchase orders for active plutonium in secure national defense installations. b. Completes operational internal

Showing 5100 - 5200

of 10291

First

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

Last

Step by Step Answers

.png)

.png)