New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

auditing

Auditing An International Approach 6th edition Wally J. Smieliauskas, Kathryn Bewley - Solutions

Why can some authorization procedures be performed by low-level managers? What kinds of authorizations need to come from the board of directors?

What are the risks related to cutoff procedures?

Match the seven control objectives to the five principal assertions.

How does the auditor’s control risk assessment relate to audit risk?

Why is there a cost-benefit trade-off involved in evaluating internal controls for planning the audit?

List some commonly used general controls related to IT.

What does the auditor need to understand about the auditee’s control environment?

What does the auditor need to understand about the flow of transactions in the auditee’s information systems?

What sources of information can auditors use to gain knowledge about the auditee’s internal controls?

Why is audit file documentation required for the auditor’s decision on whether to rely on controls in the audit planning?

Why do many organizations have documentation of their internal control system?

What is a substantive audit approach, and how does it differ from a combined audit approach?

What steps are involved in a control risk assessment?

What is a control strength? What is a control weakness? How do control strengths relate to control testing?

What is the purpose of a bridge working paper, and what information does it contain?

What are the implications for the audit program if tests of key controls indicate they are operating effectively for the whole period being audited? What are the implications if a key control is tested and a high degree of noncompliance is found?

What challenges arise for management and the auditor when an auditee uses complex IT and/or is involved in e-commerce?

In which situations are manual controls preferable, and in which are IT controls preferable?

What risks and controls relate to recording and processing e-commerce transactions?

List some fraud risks that may exist in e-commerce activities.

What risk arises if IT systems are not properly aligned to each other?

Categorize the eleven points of vulnerability to misstatement errors related to manual input, computer processing, and error correction activities in a computerized information system.

Why might manual control procedures differ from IT control procedures, even if both are directed at the same control objective?

Describe one manual and one IT control procedure designed to prevent a credit sale being processed without proper authorization by the credit manager.

What three conclusions about control risk can be reached based on internal control evaluation? What are the implications of each on the audit approach selected?

What do the terms “required degree of control compliance” and “actual degree of control compliance” mean?

What is a control test? Why do auditors perform control tests? What audit evidence is produced by control tests?

What is the difference between inspection and re-performance in control testing?

Why would controls be tested for the whole period being audited?

What are the auditors’s reporting responsibilities for internal control deficiencies?

How does professional skepticism help financial statement auditors meet their responsibilities to communicate internal control deficiencies?

Assume that when conducting procedures to obtain an understanding of the control structure in the Denton Seed Company, you checked “No” to the following internal control questionnaire items:• Does access to online files require specific passwords to be entered to identify and validate the

The auditor learns that the auditee has a control procedure in place that addresses the validity of sales and existence of accounts receivable. When a truck driver picks up goods from the warehouse, the warehouse employee has the driver sign a “shipper’s receipt” showing the quantities and

Online retailers, such as Amazon.com or Grocerygateway.com, make use of online customer order forms to allow customers to input all the required sale, delivery, and payment data.Required:a. Identify control procedures that can be used in an online sales order system and the risk(s) each

To test an organization’s internal control procedures, auditors design a test of controls audit program. This audit program is a list of control tests to be performed, and each is directly related to an important auditee control procedure. Auditors perform the tests to obtain evidence about the

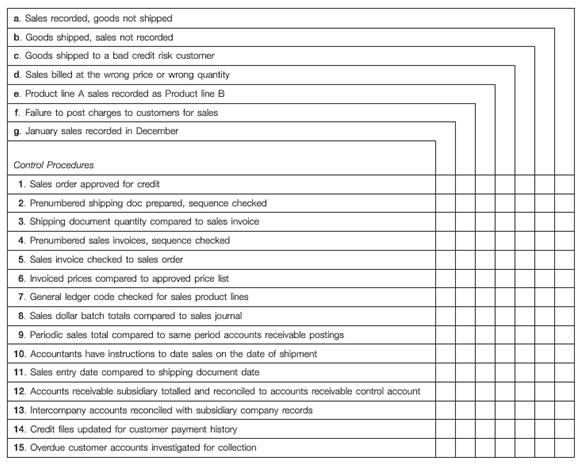

Exhibit EP9–6 contains an arrangement of examples of transaction errors (lettered a – g) and a set of auditee control procedures and devices (numbered 1–15). You should photocopy. Exhibit EP9–6 to use for completing the requirements of this questionRequired:a. Opposite the examples of

Part AThe following are internal control procedures found in the purchases and payment process of your auditee, Integrated Measurement Systems Inc.Required:For each control procedure:a. Explain the type of control that is being applied.b. Identify the control objective(s) that the control procedure

At a meeting of the corporate audit committee attended by the general manager of the products division and you, representing the internal audit department, the following dialogue took place:• Jiang (committee chair): Mr. Marks has suggested that the internal audit department conduct an audit of

An experienced auditor remarked that it is only necessary to check the additions and extensions on one invoice generated by an IT-based system, because if the computer program does one invoice correctly it will do them all correctly, so there is no point in testing a statistical sample of

The four questions below are taken from an internal control questionnaire. For each question, state (i) one control test you could use to find out whether the control technique was really used, and (ii) what error could occur if the question were answered “no,” or if you found the control was

The strengths of the IT general controls collectively provide an appropriate foundation for maintaining the integrity of information, the security of data, and the efficient operation of application controls. Weaknesses in IT general controls increase the risk of material misstatement at the

The Canada Revenue Agency has introduced “e-filing.” Registered tax professionals can submit taxpayers’ annual income tax returns online over the Internet. The taxpayer’s annual return information is automatically entered into the tax department’s computer system. No paper forms or

One of the things you can do in a logical approach to the assessment of internal control is imagine what types of errors could occur with regard to each significant class of transactions. Assume a company has the significant classes of transactions listed below.Required:For each one, identify one

Whistler Corp. is a new audit engagement for your firm. Whistler backs up all its sales transaction detailed data for each month on a portable hand-held disk drive. The drive is retained offsite for three months and then reused. This system is used because the company only has four drives, which

The following are narrative descriptions of sales systems and controls for these two different businesses. Avocet Inc.Avocet is a franchise fast food restaurant business. When customers order food, the counter person presses the appropriate buttons on the cash register. There is a button for each

The following questions and cases deal with the subject of cost-benefit analysis of internal control. Some important concepts in cost-benefit analysis are as follows:1. Measurable benefit. Benefits or cost savings may be measured directly or may be based on estimates of expected value. An expected

The SB Construction Company has two divisions. The president, Su, manages the roofing division. Su has delegated authority and responsibility for management of the modular manufacturing division to Jon Gee. The company has a competent accounting staff and a full-time internal auditor. Unlike Su,

Sally’s Craft Corner was opened in 2003 by Sally Moore, a fashion designer employed by Bundy’s Department Store.Sally is employed full-time at Bundy’s and travels frequently to shows and marts in Vancouver, Montreal, and Toronto. She enjoys crafts, wanted a business of her own,

Garganey Corp. manufactures automobile dashboards and interior components for Big Motors Inc.(BMI). BMI requires that all its suppliers be connected to its computerized procurement and manufacturing system. BMI’s production planning system generates components requirements lists, which are then

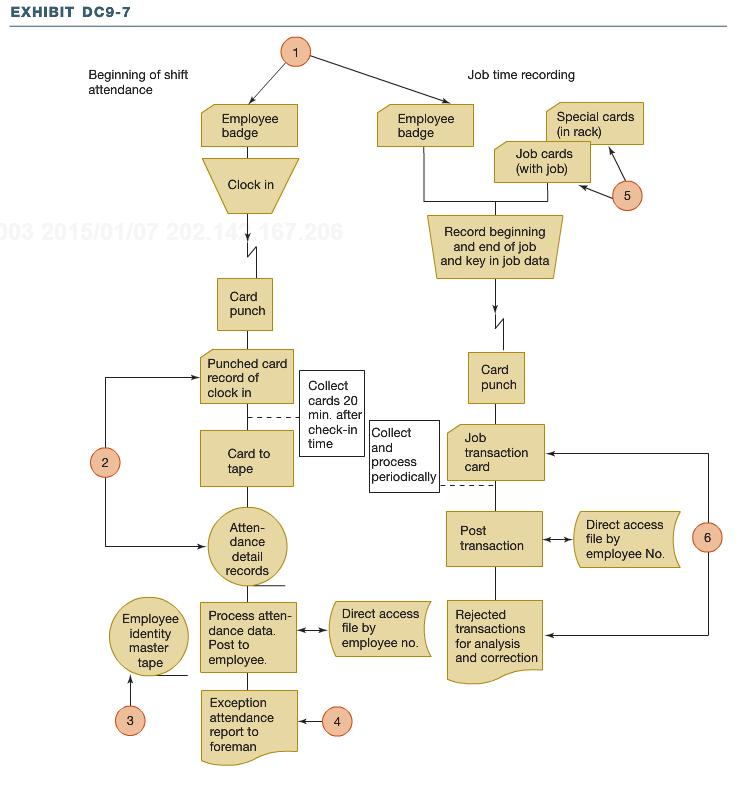

Each number of the flow chart in Exhibit DC9-7 locates a control point in the labor processing system of your auditee,Alouette Inc.Required:a. Make a list of the control points, and, for each point, describe the type or kind of internal control procedure that ought to be specified.b. Assume that

Eider Equipment Leasing Limited is in the financing lease business. It uses a service organization to compute lease payment schedules. Eider’s customers sign standard equipment leases ranging from 3 to 15 years. The details of the leases are summarized and sent to the service organization for

Golden Years Inc. owns and operates 20 rental retirement properties. It has a total of 9000 one-bedroom and 3000 two-bedroom rental units. Tenants pay rent monthly by giving a cheque to the property manager. The manager deposits the cheques at the nearest branch of Golden Years’ bank and sends

Define the following terms: audit sampling, population, population unit, and sample.

Distinguish between statistical and non-statistical sampling.

Differentiate between representative and non-representative testing. What client actors determine which is most appropriate in planning audit procedures?

What is the difference between a statistical representative test and a non-statistical representative test?

What is non-sampling risk? Give some examples.

In control testing, why is it necessary to define a compliance deviation in advance?

Which judgments must an auditor make when deciding on a sample size?

Describe the influence of each judgment on sample size.

Name and describe four sample selection methods.

What important decision must be made when test of controls auditing is performed and control risk is evaluated at an interim date several weeks or months before the client’s fiscal year-end?

Write the expanded risk model. What risk is implied for “test of detail risk” when IR = 1.0, CR = 0.40, APR = 0.60, AR = 0.048, tolerable misstatement = $10,000, and the estimated standard deviation in the population = $25?

What audit purpose is served by stratifying an account balance population and by selecting some units from the population for 100% audit verification?

What kind of evidence evaluation consideration should an auditor give to the dollar amount of a population unit that cannot be audited?

What are the three basic steps in quantitative evaluation of monetary amount evidence when auditing an account balance?

The projected likely misstatement may be calculated, yet further misstatement may remain undetected in the population. How can auditors take the further misstatement under consideration when completing the quantitative evaluation of monetary evidence?How is this done by formula?

What additional considerations are in order when auditors plan to audit account balances at an interim date several weeks or months before the client’s fiscal year-end date?

What role does professional judgment play in audit decisions regarding materiality, risk, and sampling?

Does sampling risk always exist in both statistical and non-statistical sampling? Explain your response.

What are control tests? What purpose do they serve?

In test of controls auditing, why should auditors be more concerned with the risk of assessing the control risk too low than with that of assessing it too high?

When auditing account balances, why is an incorrect acceptance decision considered more serious than an incorrect rejection decision?

What should be the relationship between tolerable misstatement in the audit of an account balance and the amount of monetary misstatement considered material to the overall financial statements?

What general set of audit objectives can you use as a frame of reference for specific objectives for the audit of an account balance?

The accounting firm of Mason & Jarr performed the work described in each separate case below. The two partners are worried about properly applying standards regarding audit sampling. They have asked for your advice.Required:Write a report addressed to them, stating whether they did or did not

This exercise asks you to specify control test objectives and define deviations in connection with planning the test of controls audit of Kingston Company’s internal controls.Required:a. For each control cited below, state the objective of an auditor’s test of controls audit procedure.b. For

Auditor Magann was auditing the authorization control over cash disbursements. She selected cash disbursement entries made throughout the year and vouched them to paid invoices and cancelled cheques bearing the initials and signatures of people authorized to approve the disbursements. She performed

Assume you audited control compliance in the Kingston Company for the deviations related to a random selection of sales transactions, as shown in Exhibit EP 10-4. For different sample sizes, the number of deviations was as Exhibit EP 10-4.Required:For each deviation and each sample,

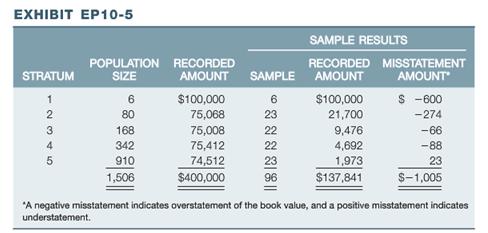

The stratification calculation example in the chapter shows the results of calculating the projected likely misstatement using the difference method. Assume the results shown in Exhibit EP 10-5 were obtained from a stratified sample.Required:Apply the ratio calculation method to each stratum

In the dialogue between the Kingston auditors, Fred said, “Our analytical procedures related to receivables didn’t show much. The total is down, consistent with the sales decline, so the turnover is up a little. If any misstatement is in the receivables total, it may be too small to be obvious

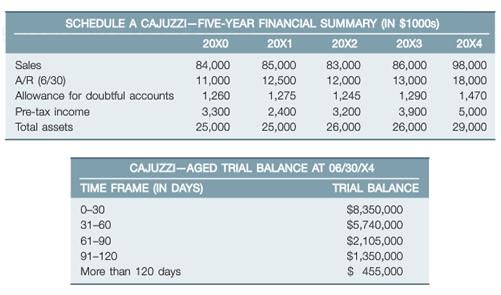

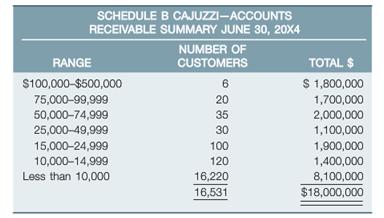

Toni Tickmark has been assigned to plan the audit of the Cajuzzi Corporation, and is currently planning the circularization (confirmation) of accounts receivable. Cajuzzi sells a number of products in the personal health care field but its mainstay is a portable whirlpool unit for use in bathtubs

You are about to commence the audit of Delta Ltd. (See Exhibit DC 10-2) This is the first time you have worked in the field without direct supervision by a senior, and you are, of course, anxious to do a good job. The senior has preceded you in visiting the client and has left you an audit

When Marge Simpson, PA, audited the Candle Company inventory, a random sample of inventory types was chosen for physical observation and price testing. The sample size was 80 different types of candles and candle-making inventory. The entire inventory contained 1740 types, and the amount in the

The following Exhibit DC 10-4 gives auditor judgment and audit sampling results for six populations. Assume large population sizes.Required:a. For each population, did the auditor select a smaller sample size than is indicated by using the tables for determining sample size (assume K 5

Does non-sampling risk include improper application of GAAP? Discuss.

What is the basic sequence of activities and related accounting in the revenues, receivables, and receipts process?

What are some risks of material misstatement in the assertions for revenues?

Why should a list of cash remittances be made and sent to the accounting department?

Suppose you selected a sample of customers’ accounts receivable and wanted to find supporting evidence for the entries in the accounts. Where would you go to vouch the debit entries? What would you expect to find? Where would you go to vouch the credit entries? What would you expect to find?

What specific control policies and procedures (in addition to separation of duties and responsibilities) should be in place and operating in control structure governing revenue recognition and cash accounting?

What is a walk-through of a sales transaction? How can the walk-through work complement the use of an internal control questionnaire?

What is dual-direction testing of controls? What are the objectives of dual-direction testing in auditing the revenues, receivables, and receipts process?

Why is it important to place emphasis on the existence and ownership (rights) assertions when auditing cash and accounts receivable?

Which audit procedures are usually the most useful for auditing the existence and ownership (rights) assertions? Give some examples.

List the information an auditor should ask for in a standard bank confirmation sent to an auditee’s bank.

Distinguish between positive and negative confirmations. Under what conditions would you expect each type of confirmation to be appropriate? Discuss.

What special care should be taken with regard to examining the sources of accounts receivable confirmation responses? Discuss.

What is a cutoff bank statement? How is it used by auditors?

What is lapping? What procedures can auditors employ for its detection?

Showing 6000 - 6100

of 10291

First

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

Last

Step by Step Answers

.png)

.png)

.png)

.png)

.png)