New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

auditing

Auditing and Assurance Services 6th edition Timothy Louwers, Robert Ramsay, David Sinason, Jerry Straws - Solutions

Aubrey Marblehead is conducting tests of controls on the control that quantities on Rock’s receiving reports are appropriately verified. In so doing, Marblehead has inquired of Rock’s receiving personnel, who said that they place a mark near the quantities verified and sign the receiving report

Monroe Curtis is auditing the revenue cycle of Kentucky Distilleries and has elected to perform a nonstatistical test of controls. Kentucky Distilleries sells Old Horse Bourbon to wholesale distributors around the country. Because the sale of bourbon is strictly controlled, Curtis does not expect

The firm of Buy and Best, CPAs, is engaged to conduct the audit of Radio Hut, a retailer of electronic and other high- technology products. Because of technological advances in Radio Hut’s inventory products, an important risk that it faces is that prices charged by suppliers reflect current

You overheard the following dialogue between Joe Ashley (a staff assistant) and Monique Estrada (his supervisor). Required: Referring to appropriate professional standards, comment on each of these statements. a. “It’s unfortunate that generally accepted auditing standards don’t allow us to

Marty Alewine, a newly pro-moted senior at your firm, has been assigned as in charge of the audit of Doxey Electron-ics. Doxey has been a client of your firm for years. Controls are considered effective, and statistical attributes sampling to test sales transactions has been used for several years.

Sydney Siebenthaler, the audit manager for Jennifer’s Running Shirts Inc., has just returned from a continuing education class on audit sampling and now wants to use discovery sampling or sequential sampling on the Jennifer’s audit because the class instructor said that the sample sizes would

Go to the Kaplan website link at www. mhhe.com /louwers6e, click on Abernathy Inc. (Sample Size) AUD TBS, and complete your answer.

Go to the ACL website link at www. mhhe. com/ louwers6e , click on ACL Assignments, and complete the assignment for Module F.

Define attributes sampling. In what stage of the audit would it be used?

How do the management assertions relate to the objectives of attributes sampling?

Define deviation condition. Why are deviation conditions so important in an attributes sampling application?

Why is appropriately defining the population of interest so important in an attributes sampling application?

In attributes sampling, why is the risk of overreliance more important than the risk of underreliance?

What are some important considerations for the audit team when selecting sample items?

What are tests of controls? What is the audit team’s goal in performing them in an attributes sampling application?

What factors influence the determination of the upper limit rate of deviation?

If the audit team examines a sample of 100 items, finds six deviations, and calculates an upper limit rate of deviation of 10.3 percent, what is the allowance for sampling risk?

What is the audit team’s decision rule with respect to the relationship between the upper limit rate of deviation and the tolerable rate of deviation?

What options are available to the audit team if the upper limit rate of deviation is higher than the tolerable rate of deviation?

Define discovery sampling. When is it typically used?

What are the advantages and disadvantages of using MUS? Under what conditions is it best used?

What are the two sampling risks associated with variables sampling? What types of losses are associated with each of these risks?

How does the audit team determine the acceptable level of the risk of incorrect acceptance? What is the relationship between this risk and sample size?

How does the audit team determine tolerable misstatement? What is the relationship between tolerable misstatement and sample size?

Describe the process used to select an MUS sample. Why does this process tend to select larger dollar components or transactions for examination?

Identify the three components of the upper limit on misstatements. How is each component calculated?

What is the upper limit on misstatements? What information does it provide the auditor?

What options are available to the audit team if the upper limit on misstatements exceeds the tolerable misstatement?

Define classical variables sampling. How does it provide the audit team evidence as to the fairness of an account balance or class of transactions?

What is the standard deviation? How does it affect the necessary sample size?

Define precision and the precision interval. What factors are used to determine the level of precision?

When selecting a variables sampling approach, when should the audit team use MUS and classical variables sampling?

What factors affect the size of a sample in a nonstatistical sampling application?

What information related to variables sampling applications does the audit team typically document?

Which of the following major stages of the audit is most closely related to variables sampling? a. Determining preliminary levels of performance materiality. b. Performing tests of controls procedures. c. Performing substantive procedures. d. Searching for the possible occurrence of subsequent

Which of the following types of variables sampling plans has a tendency to select higher-dollar items for examination? a. Difference estimation. b. Mean- per- unit estimation. c. Monetary unit sampling. d. Ratio estimation.

Variables sampling methods can be used toestimate

When evaluating the results of an MUS sampling application, the audit team should com-pare the upper limit on misstatements to the a. Expected misstatement. b. Incremental allowance for sampling risk. c. Projected misstatement. d. Tolerable misstatement.

When making a decision about the dollar amount in an account balance based on a sample, the audit team considers the risk of incorrect acceptance to be more serious than the risk of incorrect rejection because a. The incorrect rejection decision impairs the efficiency of the audit. b. The audit

The unique feature of monetary unit sampling is that a. Sampling units are not chosen at random. b. A dollar unit selected in a sample is not replaced before the sample selection is completed. c. Auditors need not worry about the risk of incorrect acceptance decision. d. The population is defined

When determining sample size under monetary unit sampling, an audit team does not need to make a judgment or estimate of a. Audit risk. b. Tolerable misstatement. c. Expected misstatement. d. Standard deviation.

Which of the following statements is correct about monetary unit sampling? a. The risk of incorrect acceptance must be specified. b. Smaller logical units have a higher probability of selection in the sample than larger units. c. Each logical unit in the population has an equally likely chance of

One of the primary advantages of monetary unit sampling is the fact that a. It is an effective method of sampling for evidence of understatement in asset accounts. b. The sample selection automatically achieves high- dollar selection and stratification. c. The sample selection provides for

Which of the following would not cause the audit team to select a larger sample of items under a monetary unit sampling application? a. A reduction in the risk of incorrect acceptance from 10 percent to 5 percent. b. An increase in the tolerable misstatement from $ 30,000 to $ 60,000. c. An

Assume that an account with a recorded balance of $ 5,000 has an audited balance of $ 3,000. By using monetary unit sampling, if the sampling interval is $ 1,500, the projected misstatement would be a. $ 600 . b. $ 900 . c. $ 2,000 . d. $ 3,000 .

If the _____ is less than the _____ , the audit team would conclude that the account balance is fairly stated. a. Projected misstatement; tolerable misstatement. b. Tolerable misstatement; projected misstatement. c. Upper limit on misstatements; tolerable misstatement. d. Tolerable misstatement;

If the upper limit on misstatements is calculated at $ 17,800 and the tolerable misstatement is $ 15,000, what is the minimum amount of adjustment necessary for the audit team to issue an unmodified opinion on the client’s financial statements?a. $ 0 b. $ 2,800 c. $ 4,800 d. $ 14,800

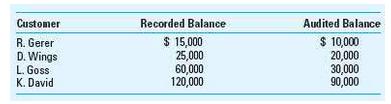

Alice Rathermel audited LoHo Company’s inventory using sampling. She examined 120 items from an inventory compilation list and discovered net overstatement of $ 480. The audited items had a book (recorded) value of $ 48,000. There were 1,200 inventory items listed, and the total recorded

To determine the sample size for a classical variables sampling application, an audit team should consider the tolerable misstatement, risk of incorrect acceptance, risk of incorrect rejection, population size, population variability, and a. Expected misstatement in the account. b. Overall

Which of the following components is not used in determining the upper limit on misstatements? a. Basic allowance for sampling risk. b. Incremental allowance for sampling risk. c. Projected misstatement. d. Tolerable misstatement.

The projected misstatement is determined by multiplying the sampling interval by the a. Risk of incorrect acceptance. b. Incremental confidence factor. c. Confidence factor. d. Tainting percentage.

Which of the following steps involved with determining the upper limit on misstatements is ordinarily performed earliest? a. Multiply the sampling interval by the tainting percentage. b. Determine the audited amount of the item and compare it to the recorded amount. c. Calculate the basic allowance

A component of an account balance has a recorded balance of $ 10,000 and an audited balance of $ 8,000. By using monetary unit sampling, if the sampling interval is $ 20,000, the projected misstatement would be a. $ 2,000 . b. $ 4,000 . c. $ 5,000 . d. $ 10,000.

Which of the following statements is not true with respect to the calculation of the upper limit on misstatements? a. The tainting percentage is determined based on the difference between the recorded balance and the audited balance. b. A separate incremental allowance for sampling risk is

Which of the following courses of action would an audit team most likely follow in planning a sample of cash disbursements if the audit team is aware of several unusually large cash disbursements? a. Increase the sample size to reduce the effect of the unusually large disbursements. b. Continue to

For each of the following independent situations, indicate the advantages and disadvantages of MUS and classical variables sampling.a. You are selecting a sample of customer accounts receivable balances for confirmation. The sample is to be selected from a population of customer accounts

Emerson Washburn is examining the accounts receivable of Anaheim Company and has decided to use MUS to select a sample of customer accounts for confirmation. Anaheim’s accounts receivable totaled $ 3,500,000 and comprised 3,000 different customer accounts ranging in amount from $ 200 to $

You have been assigned to select an MUS sample from Whitney Company's detailed inventory records as of September 30. Whitney's controller gave you a list of the 23 different inventory items and their recorded book amounts. The senior accountant told you to select a sample of 10 dollar units and the

The recorded accounts receivable balance for Warner Company was $ 500,000. Required: For each of the following independent sets of conditions, determine the appropriate sample size for the examination of Warner’s accounts receivable in MUS. Based on the differences in your calculations,

Reagan Simmons is conducting the audit of Ace Inc., and is using MUS to select a sample of inventory items for examination. The recorded balance in Ace’s inventory account was $ 1,200,000. In carrying out the sampling plan, Simmons established a risk of incorrect acceptance of 5 percent, a

Monetary Unit Sampling. Casey Paul is considering the use of MUS in examining Stanley’s accounts receivable, which were recorded at $ 300,000. Using the audit risk model, Paul has identified a necessary risk of incorrect acceptance of 10 percent and has established a tolerable misstatement of $

Monetary Unit Sampling. Blythe Drake is conducting an audit of Newman and is using MUS to select a sample of customer accounts receivable for confirmation. Newman’s accounts receivable are recorded at $ 10,000,000 and comprise 2,000 customer accounts. Drake has established the

For each of the following cases, provide the missing information.Noel Frehley is examining the accounts receivable of Kiss Company and is considering the use of MUS. Kiss’s accounts receivable are recorded at $ 400,000. Based on the necessary level of risk, Frehley has established a risk of

Monetary Unit Sampling. Noel Frehley is examining the accounts receivable of Kiss Company and is considering the use of MUS. Kiss’s accounts receivable are recorded at $ 400,000. Based on the necessary level of risk, Frehley has established a risk of incorrect acceptance of 5 percent. In

Monetary Unit Sampling. For each of the follow-ing independent misstatements, identify the missingvalue:

Monetary Unit Sampling. Jordan Thomas is using MUS to examine a client’s accounts receivable balance. Using a sample size of 100 items and a sampling interval of $ 12,300, Thomas identified the following misstatements:Required:a. Calculate the upper limit on misstatements assuming a risk of

Carson Allister is performing an MUS application in the audit of Bird Company’s accounts receivable. Based on the acceptable level of the risk of incorrect acceptance of 5 percent and a tolerable misstatement of $ 120,000, Allister has calculated a sample size of 75 items and a sampling

The auditors mailed positive confirmations on 60 customers’ accounts receivable balances. The company’s accounts receivable balance comprised 2,356 customer accounts with a total recorded balance of $ 19,600,000, and the sampling interval was $ 280,000. The auditors received four positive

Assume that Parker Fran has calculated a sampling interval for Tide Inc.’s inventory of $ 10,000 and has conducted an examination of a sample of inventory balances. Fran has identified the following three misstatements:Required:Calculate the upper limit on misstatements for the following

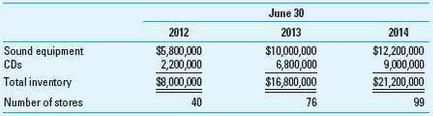

Clyde Billy is conducting the audit of Hoops Inc. and is examining Hoops’s inventory balances. Billy plans to select a sample of inventory items for examination and will verify quantities and perform price tests to ascertain that the items are properly recorded according to generally

Zachary Mayo is a new staff accountant participating on his first audit engagement. He has been assigned to the Foley Company engagement and is examining Foley’s accounts receivable. Foley maintains a computerized ledger of its accounts receivable balances, which are recorded at $ 5,000,000 and

Clint Walker was examining the accounts receivable of Country Music Inc. Its accounts receivable were recorded at $ 1,500,000. Based on past audits, Walker established tolerable misstatement at 10 percent of the recorded account balance and anticipated a very small level of misstatement in

Dylan Mays is auditing the accounts receivable of Channel Company. Channel’s accounts receivable were recorded at $ 2,000,000 and comprised more than 1,500 customer accounts. However, Channel’s 10 largest customers’ balances comprised a high percentage of the recorded

The recorded inventory balance for Faulk Company was $ 1,000,000 and comprised 2,500 customer accounts.Required:For each of the following independent sets of conditions, determine the appropriate sample size for the audit of Faulk’s inventory using classical variables sampling (mean- per- unit

Shannon Solomon, CPA, is auditing the accounts receivable of Warner Company and is using mean- per- unit estimation. Accounts receivable were recorded at $ 2,000,000 and comprised 1,250 individual customer accounts. Solomon established the following parameters for the audit of accounts

You are auditing Hernandez Inc.’s accounts receivable balance using classical variables sampling. Hernandez’s accounts receivable comprised 2,500 customer accounts and were recorded at $ 3,500,000. Using a risk of incorrect acceptance and a risk of incorrect rejection of 5 percent, you

Jessie Howe is examining Met Company’s accounts receivable balance and has decided to use mean- per- unit estimation. Met’s accounts receivable were recorded at $ 650,000 and comprised 2,000 individual customer accounts. Howe established tolerable misstatement at 5 percent of the recorded

Wade Wallace designed a classical variables sampling application to examine the accounts receivable for Rasheed Inc. After considering several possibilities, Wallace decided to use mean- per- unit estimation. The following parameters are noted through a review of Wallace’s audit

Finley Gunny is using nonstatistical sampling in the examination of Highway Company’s accounts receivable, which were recorded at $ 350,000. Gunny determined a tolerable misstatement of $ 15,000 and a sample size of 49 items. Required: a. How does Gunny determine sample size using non-statistical

Marley Brown is planning the substantive procedures for the audit of Longhorn Company’s inventory, which had a recorded (unaudited) balance of $ 6,500,000. In prior audits, Brown used monetary unit sampling but is now considering the use of non-statistical sampling. Brown has established a

Kelsey Mead, CPA, was engaged to audit Jiffy Company’s financial statements for the year ended August 31.Required:Describe each incorrect assumption, statement, and inappropriate application of sampling in Mead’s procedures in the following.For the current year, Mead decided to use MUS to

The law firm of Spade & Associates hired Dylan Sayers to review the audit of the 2014 financial statements that Hammer & Wimsey, CPAs, had completed for Golden Sound and Records Company. Specifically, the attorneys engaged Sayers to determine whether the audit of Golden Sound’s inventory

Indicate whether each of the following characteristics applies to monetary unit sampling (MUS), classical variables sampling (CVS), both MUS and CVS ( both), or neither MUS nor CVS ( neither). a. May be used in conjunction with substantive procedures. b. Tends to select higher dollar items for

Georgie Costanza, CPA, is auditing the accounts receivable of Vandalay Industries and is considering the use of MUS techniques. Costanza has a number of questions regarding the use of MUS and has asked you to provide answers to them. Required: a. Under generally accepted auditing standards, can

Required: Refer to the mini- case “Unhealthy Accounting at HealthSouth” on page C14 and respond to question 6.On page C14HealthSouth concealed the fraud by keeping the fraudulent transactions below $ 5,000. What recommendation would you have to E& Y to improve its sampling practices?

In what stage of the audit is variables sampling used?

Define monetary unit sampling ( MUS). What is the unique feature of MUS?

What is the typical attribute of interest in an MUS application?

How does the audit team determine expected misstatement? What is the relationship between expected misstatement and sample size?

In an MUS application, how is the population size defined? What is the relationship between population size and sample size?

What is the sampling interval? How is it calculated?

What is stratification? What are the benefits to the audit team of stratifying the sample?

Identify differences between the determination of sample size under classical variables sampling and MUS.

How does sample selection under classical variables sampling differ from sample selection under?

What is the audit team’s decision rule when comparing the recorded balance to the precision interval?

How does nonstatistical sampling differ from statistical sampling?

Identify five major considerations that are introduced when the client uses information technology.

What are the three major phases in the audit team’s evaluation of internal control? How does the use of information technology affect the procedures performed in those phases?

Identify and define the two major types of controls in an accounting information system.

Showing 5500 - 5600

of 10291

First

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

Last

Step by Step Answers

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)