New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

banking

Financial Markets and Institutions 6th edition Anthony Saunders, Marcia Cornett - Solutions

Consider two bonds a 10-year premium bond with a coupon rate higher than its required rate of return and a zero coupon bond that pays only a lump sum payment after 10 years with no interest over its life. Which do you think would have more interest rate risk— that is, which bond’s price would

Consider again the two bonds in Question. If the investment goal is to leave the assets untouched until maturity, such as for a child’s education or for one’s retirement, which of the two bonds has more interest rate risk? What is the source of this risk?

What is the nature of an off-balance-sheet activity? How does an FI benefit from such activities? Identify the various risks that these activities generate for an FI, and explain how these risks can create varying degrees of financial stress for the FI at a later time.

What is foreign exchange risk? What does it mean for an FI to be net long in foreign assets? What does it mean for an FI to be net short in foreign assets? In each case, what must happen to the foreign exchange rate to cause the FI to suffer losses?

If the Swiss franc is expected to depreciate in the near future, would a U. S. – based FI in Bern City, Switzerland, prefer to be net long or net short in its asset positions? Discuss.

If you expect the Swiss franc to depreciate in the near future, would a U. S. – based FI in Basel, Switzerland, prefer to be net long or net short in its asset positions? Discuss

What is country or sovereign risk? What remedy does an FI realistically have in the event of a collapsing country or currency?

What is the difference between technology risk and operational risk? How does internationalizing the payments system among banks increase operational risk?

Why can insolvency risk be classified as a consequence or outcome of any or all of the other types of risks?

Discuss the interrelationships among the different sources of FI risk exposure. Why would the construction of an FI risk management model to measure and manage only one type of risk be incomplete?

What two factors provide potential benefits to FIs that expand their asset holdings and liability funding sources beyond their domestic borders?

If an FI has the same amount of foreign assets and foreign liabilities in the same currency, has that FI necessarily reduced the risk involved in these international transactions to zero? Explain.

A U.S. insurance company invests $1,000,000 in a private placement of British bonds. Each bond pays £300 in interest per year for 20 years. If the current exchange rate is £1.5612 for U. S.$1, what is the nature of the insurance company’s exchange rate risk? Specifically, what type of

Characterize the risk exposure(s) of the following FI transactions by choosing one or more of the following: a. Credit risk b. Interest rate risk c. Off-balance-sheet risk d. Foreign exchange rate risk e. Country/ sovereign risk f. Technology risk (1) A bank finances a $ 10 million, six-year,

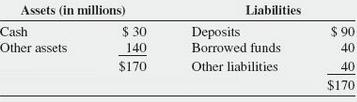

A financial institution has the following market value balance sheet structure:a. The bond has a 10-year maturity, a fixed-rate coupon of 10 percent paid at the end of each year, and a par value of $ 10,000. The certificate of deposit has a 1-year maturity and a 6 percent fixed rate of interest.

Consider the following income statement for WatchoverU Savings Inc. (in millions):a. What is WatchoverU€™s expected net interest income at year-end? b. What will be the net interest income at year- end if interest rates rise by 2 percent?

If a bank invested $ 50 million in a two-year asset paying 10 percent interest per year and simultaneously issued a $ 50 million one-year liability paying 8 percent interest per year, what would be the impact on the bank’s net interest income if, at the end of the first year, all interest rates

Assume that a bank has assets located in Germany worth € 150 million earning an average of 8 percent. It also holds € 100 in liabilities and pays an average of 6 percent per year. The current spot rate is € 1.50 for $ 1. If the exchange rate at the end of the year is € 2.00 for $ 1:a. What

Six months ago, Qualitybank issued a $ 100 million, one-year-maturity CD, denominated in British pounds (Euro CD). On the same date, $ 60 million was invested in a £-denominated loan and $ 40 million in a U.S. Treasury bill. The exchange rate on this date was £ 1.5382 for $ 1. If you assume no

Suppose you purchase a 10-year AAA-rated Swiss bond for par that is paying an annual coupon of 8 percent and has a face value of 1,000 Swiss francs (SF). The spot rate is U. S. $ 0.66667 for SF1. At the end of the year, the bond is downgraded to AA and the yield increases to 10 percent. In

Why is credit risk analysis an important component of FI risk management?

In what ways does the credit analysis of a mid-market borrower differ from that of a small-business borrower?

What are compensating balances? What is the relationship between the amount of compensating balance requirement and the return on the loan to the FI? The following questions are related to the Appendix material.

How does loan portfolio risk differ from individual loan risk?

What are the primary considerations used by FIs to evaluate mortgage loans?

What are the purposes of credit scoring models? How do these models assist an FI manager to better administer credit?

How does an FI evaluate its credit risks with respect to consumer and small business loans?

What are some of the special risks and considerations when lending to small businesses rather than large businesses?

Why must an account officer be well versed in the FI’s credit policy before talking to potential mid-market business borrowers?

How does ratio analysis help to answer questions about the production, management, and marketing capabilities of a prospective borrower?

Why should a credit officer be concerned if a mid-market business borrower’s liquidity ratios differ from the industry norm?

What are conditions precedent?

Why is an FI’s bargaining strength weaker when dealing with large corporate borrowers than mid-market business borrowers?

Consider the coefficients of Altman’s Z-score. Can you tell by the size of the coefficients which ratio appears most important in assessing the creditworthiness of a loan applicant? Explain.

Explain how modern portfolio theory can be applied to lower the credit risk of an FI’s portfolio.

Jane Doe earns $ 30,000 per year and has applied for an $ 80,000, 30-year mortgage at 8 percent interest, paid monthly. Property taxes on the house are expected to be $ 1,200 per year. If her bank requires a gross debt service ratio of no more than 30 percent, will Jane be able to obtain the

In 2015, Webb Sports Shop had cash flows from investing activities of $ 2,567,000 and cash flows from financing activities of $ 3,459,000. The balance in the firm’s cash account was $ 950,000 at the beginning of 2015 and $ 1,025,000 at the end of the year. Calculate Webb Sports Shop’s cash flow

Industrial Corporation has a net income-to-sales (profit margin) ratio of 0.03, a sales-to-assets (asset utilization) ratio of 1.5, and a debt-to-asset ratio of 0.66. What is Industrial’s return on equity?

Suppose that the financial ratios of a potential borrowing firm took the following values: X1 = Net working capital/Total assets = 0.10, X2 = Retained earnings/Total assets = 0.20, X3 = Earnings before interest and taxes/ Total assets = 0.22, X4 = Market value of equity/Book value of long-term

Metrobank offers one-year loans with a 9 percent stated rate, charges a ¼ percent loan origination fee, imposes a 10 percent compensating balance requirement, and must pay a 6 percent reserve requirement to the Federal Reserve. What is the return to the bank on these loans?

Suppose you are a loan officer at Carbondale Local Bank. Joan Doe listed the following information on her mortgage application:Use the information below to determine whether or not Joan Doe should be approved for a mortgage from your bank.The loan is automatically rejected if the applicant’s

Use the balance sheet and income statement below to construct a statement of cash flows for 2016 for Clancy's Dog BiscuitCorp.

Harper Outdoor Furniture, Inc., has net cash flows from operating activities for the last year of $ 340 million. The income statement shows that net income is $ 315 million and depreciation expense is $ 46 million. During the year, the change in inventory on the balance sheet was $ 38 million, the

Consider the following company€™s balance sheet and income statement.For this company, calculate the following: a. Current ratio. b. Number of days€™ sales in receivables.c. Sales to total assets. d. Number of days in inventory. e. Debt-to-asset ratio. f. Cash-flow debt ratio.

Calculate the following ratios for Lake of Egypt Marina Inc. as of year-end 2016.Using these ratios for Lake of Egypt Marina, Inc., and the industry, what can you conclude about Lake of Egypt Marina's financial performance for 2016? (Ratios l, m, n, and o use net income available to common

The following is ABC, Inc.’s, balance sheet (in thousands):Also, sales equal $ 500, cost of goods sold equals $ 360, interest payments equal $ 62, taxes equal $ 56, and net income equals $ 22. The beginning retained earnings is $ 0, the market value of equity is equal to its book value, and

An FI is planning to give a loan of $ 5,000,000 to a firm in the steel industry. It expects to charge an up-front fee of 0.10 percent and a service fee of 5 basis points. The loan has a maturity of 8 years. The cost of funds (and the RAROC benchmark) for the FI is 10 percent. The FI has estimated

A bank has two loans of equal size outstanding, A and B, and the bank has identified the returns they would earn in two different states of nature, 1 and 2, representing default and no default, respectively.If the probability of state 1 is 0.2 and the probability of state 2 is 0.8, calculate: a.

How does the degree of liquidity risk differ for different types of financial institutions?

Why would a DI be forced to sell assets at fire- sale prices?

What are core deposits? What role do core deposits play in predicting the probability distribution of net deposit drains?

How is asset-side liquidity risk likely to be related to liability-side liquidity risk?

What are two ways a DI can offset the effects of asset-side liquidity risk, such as the drawing down of a loan commitment?

What are the two reasons liquidity risk arises? How does liquidity risk arising from the liability side of the balance sheet differ from liquidity risk arising from the asset side of the balance sheet? What is meant by fire-sale prices?

The probability distribution of the net deposit drain of a DI has been estimated to have a mean of 2 percent. a. Is this DI increasing or decreasing in size? Explain. b. If a DI has a net deposit drain, what are the two ways it can offset this drain of funds? How do the two methods differ?

How is a DI’s distribution pattern of net deposit drains affected by the following?a. The holiday season. b. Summer vacations. c. A severe economic recession. d. Double- digit inflation.

What are two ways a DI can offset the liquidity effects of a net deposit drain of funds? How do the two methods differ? What are the operational benefits and costs of each method?

Define each of the following four measures of liquidity risk. Explain how each measure would be implemented and utilized by a DI.a. Sources and uses of liquidity. b. Peer group ratio comparisons. c. Liquidity index. d. Financing gap and financing requirement.

What are the several components of a DI’s liquidity plan? How can such a plan help a DI reduce liquidity shortages?

What is a bank run? What are some possible withdrawal shocks that could initiate a bank run? What feature of the demand deposit contract provides deposit withdrawal momentum that can result in a bank run?

Describe the unprecedented steps the Federal Reserve took with respect to the discount window operations during the financial crisis.

Why does deposit insurance deter bank runs?

What is the greatest cause of liquidity exposure that property–casualty insurers face?

How is the liquidity problem faced by investment funds different from the liquidity problem faced by DIs and insurance companies?

The AllStar Bank has the following balance sheet:Its largest customer decides to exercise a $ 15 million loan commitment. Show how the new balance sheet changes if AllStar uses?(a) Stored liquidity management(b) Purchased liquidity management.

Consider the balance sheet for the DI listed below:The DI is expecting a $ 15 million net deposit drain. Show the DI's balance sheet under these two conditions:a. The DI purchases liabilities to offset this expected drain.b. The stored liquidity management is used to meet the liquidity shortfall.

A DI has $ 10 million in T-bills, a $ 5 million line of credit to borrow in the repo market, and $ 5 million in excess cash reserves (above reserve requirements) with the Fed. The DI currently has borrowed $ 6 million in fed funds and $ 2 million from the Fed discount window to meet seasonal

An investment fund has the following assets in its portfolio: $ 40 million in fixed- income securities and $ 40 million in stocks at current market values. In the event of a liquidity crisis, it can sell its assets at a 96 percent discount if they are disposed of in two days. It will receive 98

An investment fund has $ 1 million in cash and $ 9 million invested in securities. It currently has 1 million shares out-standing.a. What is the NAV of this fund? b. Assume that some of the shareholders decide to cash in their shares of the fund. How many shares, at its current NAV, can the fund

Central Bank has the following balance sheet (in millions of dollars):Cash inflows over the next 30 days from the FI's performing assets are $ 7.5 million. Calculate the LCR for Central Bank.

WallsFarther Bank has the following balance sheet (in millions of dollars):Cash inflows over the next 30 days from the FI's performing assets are $ 5.5 million. Calculate the LCR for WallsFarther Bank.

FirstBank has the following balance sheet (in millions of dollars):Calculate the NSFR for FirstBank.

BancTwo has the following balance sheet (in millions of dollars):Calculate the NSFR forBancTwo.

A DI has assets of $ 10 million consisting of $ 1 million in cash and $ 9 million in loans. It has core deposits of $ 6 mil-lion. It also has $ 2 million in subordinated debt and $ 2 mil-lion in equity. Increases in interest rates are expected to result in a net drain of $ 1 million in core

The Plainbank has $ 10 million in cash and equivalents, $ 30 million in loans, and $ 15 million in core deposits. Calculate (a) The financing gap (b) The financing requirement.

How do monetary policy actions by the Federal Reserve impact interest rates?

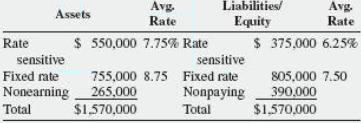

What is the repricing gap? In using this model to evaluate interest rate risk, what is meant by rate sensitivity? On what financial performance variable does the repricing model focus? Explain.

What is a maturity bucket in the repricing model? Why is the length of time selected for repricing assets and liabilities important when using the repricing model?

What is the CGAP effect? According to the CGAP effect, what is the relation between changes in interest rates and changes in net interest income when CGAP is positive? When CGAP is negative?

Which of the following is an appropriate change to make on a bank’s balance sheet when GAP is negative, spread is expected to remain unchanged, and interest rates are expected to rise? a. Replace fixed-rate loans with rate-sensitive loans. b. Replace marketable securities with fixed-rate loans.

If a bank manager was quite certain that interest rates were going to rise within the next six months, how should the bank manager adjust the bank’s repricing gap to take advantage of this anticipated rise? What if the manager believed rates would fall?

Which of the following assets or liabilities fit the one-year rate or repricing sensitivity test?a. 91-day U. S. Treasury bills.b. 1-year U. S. Treasury notes.c. 20-year U. S. Treasury bonds.d. 20-year floating-rate corporate bonds with annual repricing.e. 30-year floating-rate mortgages with

Consider the repricing model. a. What are some of its weaknesses? b. How have large banks solved the problem of choosing the optimal time period for repricing?

How is duration related to the interest elasticity of a fixed-income security? What is the relationship between duration and the price of the fixed-income security?

If you use duration only to immunize your portfolio, what three factors affect changes in an FI’s net worth when interest rates change?

If a bank manager was quite certain that interest rates were going to rise within the next six months, how should the bank manager adjust the bank’s duration gap to take advantage of this anticipated rise? What if the manager believed rates would fall?

What are the criticisms of using the duration model to immunize an FI’s portfolio?

What is convexity?

What is the difference between book value accounting and market value accounting? How do interest rate changes affect the value of bank assets and liabilities under the two methods?

What are the differences between the economist’s definition of capital and the accountant’s definition of capital? a. How does economic value accounting recognize the adverse effects of credit risk? b. How does book value accounting recognize the adverse effects of credit risk?

What are some of the arguments for and against the use of market value versus book value of capital?

What is the gap-to-total-assets ratio? What is the value of this ratio to interest rate risk managers and regulators?

What is the spread effect?

Calculate the repricing gap and impact on net interest income of a 1 percent increase in interest rates for the following positions: a. Rate-sensitive assets = $ 100 million; Rate-sensitive liabilities = $ 50 million. b. Rate-sensitive assets = $ 50 million; Rate-sensitive liabilities = $ 150

Consider the following balance sheet positions for a financial institution: • Rate-sensitive assets = $ 200 million; Rate-sensitive liabilities = $ 100 million. • Rate-sensitive assets = $ 100 million; Rate-sensitive liabilities = $ 150 million. • Rate-sensitive assets = $ 150 million;

Consider the following balance sheet for Watchover Savings Inc. (in millions):a. What is Watchover's expected net interest income at year-end? b. What will be the net interest income at year-end if interest rates rise by 2 percent? c. Using the one-year cumulative repricing gap model, what is

Consider the following balance sheet for Watchovia Bank ( in millions):a. What is Watchovia's expected net interest income at year-end? b. What will net interest income be at year-end if interest rates rise by 2 percent? c. Using the one-year cumulative repricing gap model, what is the

A bank has the following balance sheet:Suppose interest rates rise such that the average yield on rate- sensitive assets increases by 45 basis points and the average yield on rate- sensitive liabilities increases by 35 basis points.a. Calculate the bank’s repricing GAP and percentage gap.b.

Use the following information about a hypothetical government security dealer named J.P. Groman. (Market yields are in parentheses; amounts are in millions.)a. What is the repricing or funding gap if the planning period is 30 days? 91 days? 2 years? (Recall that cash is a noninterest-earning

Consider the following. a. What is the duration of a two-year bond that pays an annual coupon of 10 percent and whose current yield to maturity is 14 percent? Use $ 1,000 as the face value. b. What is the expected change in the price of the bond if interest rates are expected to decline by 0.5

Showing 2200 - 2300

of 5862

First

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

Last

Step by Step Answers

.png)

.png)

-1.png)

-2.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)