Question: Lean Accounting. Flexible Security Devices (FSD) has introduced a just-in-time production process and is considering the adoption of lean accounting principles to support its new

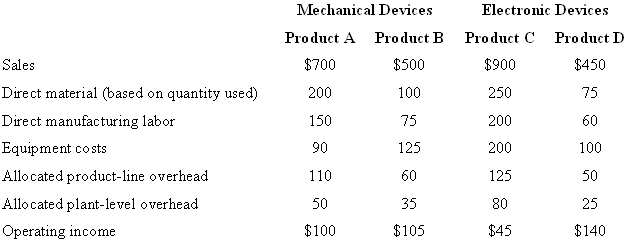

Lean Accounting. Flexible Security Devices (FSD) has introduced a just-in-time production process and is considering the adoption of lean accounting principles to support its new production philosophy. The company has two product lines: Mechanical Devices and Electronic Devices. Two individual products are made in each line. The company’s traditional cost accounting system allocates all plant-level overhead costs to individual products. Product-line overhead costs are traced directly to product lines, and then allocated to the two individual products in each line. Equipment costs are directly traced to products. The latest accounting report using traditional cost accounting methods included the following information (in thousands of dollars).

FSD has determined that each of the two product lines represents a distinct value stream. It has also determined that$120,000 of the allocated plant-level overhead costs represents occupancy costs. Product A occupies 20% of the plant’s square footage, Product B occupies 20%, Product C occupies 30%, and Product D occupies 15%. The remaining square footage is occupied by plant administrative functions or is not being used. Finally, P50 has decided that direct material should be expensed in the period it is purchased, rather than when the material is used. According to purchasing records, direct material purchase costs during the period were:

1. What are the cost objects in FSD’s lean accounting system? Which of P80’s costs would be excluded when computing operating income for these cost objects?

2. Compute operating income for the cost objects identified in requirement 1 using lean accounting principles. Why does operating income differ from the operating income computed using traditional cost accounting methods?

Mechanical Devices Electronic Devices Product D Product A Product B $700 Product C Sales 006$ 250 $500 $450 75 Direct material (based on quantity used) 200 100 200 Direct manufacturing labor 60 150 75 200 Equipment costs 90 125 100 Allo cated product-line overhead 110 60 50 125 25 Allo cated plant-level overhead Operating income 35 50 80 $105 $45 $100 $140

Step by Step Solution

3.39 Rating (171 Votes )

There are 3 Steps involved in it

Lean accounting 1 The cost object in lean accounting is the value stream not the individual productF... View full answer

Get step-by-step solutions from verified subject matter experts

Document Format (1 attachment)

24-B-C-A-C-P-A (264).docx

120 KBs Word File