New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

accounting practice

Contemporary Environmental Accounting Issues Concepts And Practice 1st Edition Stefan Schaltegger, Roger Burritt - Solutions

What is an eco-asset sheet? Does the value of eco-assets balance with those of eco-liabilities and eco-equity?

What is critical natural capital? Provide examples. For a company, who determines whether natural capital is a ‘critical’ ecological resource? Is there a difference between ‘other’ natural capital and artificial capital? Are they substitutes for each other?

Why is it that techniques for putting financial values on eco-assets are fraught with difficulty?

Compare environmental stocks and flows with financial stocks and flows.When tracking and recording these stocks and flows, what are the similarities and differences in processes used?

List the main categories of data quality. Do environmental indicators use all, some or none of these categories. Provide an example to support your view based on one environmental medium (e.g. water quality, air quality).

Distinguish between the main approaches to impact assessment. Explain the three steps that lead to construction of an EIA index. Can environmental impact added ever be negative?

Construct an environmental profile for a company of your choice. How might the profile be of use to management?

The field of ‘ontology’ studies different views of reality. Why are different ontological viewpoints important when determining the volume of information that needs to be produced by an ecological accounting system for managers?

Name and explain two allocation rules and two allocation keys. Why are allocation rules and keys important to lower-level management? If you were a site manager in a chemical company, with a single incinerator for all sites located on your site and under your control, which rule and key would you

Can the environmental impacts of one EIA centre be linked to the environmental impacts of another EIA centre? Provide an example to confirm your view? Do any control or responsibility problems arise? If there are any problems, how might they be resolved?

Distinguish between direct and indirect environmental impacts of a division.Provide an example to illustrate the difference.Why is the difference important to a site manager?

‘Environment regulations require investments in end-of-pipe technology to clean up pollutants’: Explain whether you agree with this statement. Does this mean that a company should not undertake an economic appraisal of whether‘end-of-pipe’ investments are worthwhile? Give reasons for your

What is the main difference between core and supplemental ecological indicators?Provide an example of each.Would it be useful to have all production site managers to report to top management on a common set of ecological indicators? Explain.

Examine the suggestion that small and medium-sized companies do not need information from a core set of ecological indicators related to their business.

Net present value and net present environmental impact added have a number of similarities and differences. List and explain these. Consider the arguments for and against discounting future environmental impacts.

What are the pressures on managers to report biased ecological impact information to stakeholders? How might these be alleviated?

Regulation can no longer be viewed simply in terms of ‘command and control’over companies. Discuss two alternatives to direct regulation and explain, by using the notion of an enforcement pyramid, whether there is any link between these alternatives and ‘command-and-control’ methods.

By using the five principles of regulatory design outlined in this chapter, consider how ecological reporting to external stakeholders provides a fundamental foundation for regulation of relationships between companies and stakeholders.

Are conventional financial accounting and external ecological accounting complements to each other or substitutes for each other? Discuss.

What are the features of the US Toxic Release Inventory that other ecological reporting systems should consider adopting? Are there any problems with the TRI reporting system? If so, how can these be overcome?

How many chemicals should be reported on in toxic release and national pollutant inventories and polluting emissions registers? What criteria have affected your choice?

Why is monitoring and information disclosure critical for the success of emissions banking and trading?

Do the principles behind the indicators put forward by the UN Commission on Sustainable Development have any connection with the principles behind corporate external ecological reporting? Are there any important differences between the two sets of principles? Explain.

What are information quality and environmental quality? Are they related? Why is low-quality information said to drive out high-quality information?

How might low-quality information in ecological statements be improved? In your answer, name two specific institutional mechanisms.

What assumptions underlie ecological accounting? Consider whether one assumption behind ecological accounting and reporting is more important than the other assumptions.

How do the notions of ‘going concern’ and ‘gone concern’ affect ecological statements?

Do the needs for and uses of internal and consolidated ecological accounting differ? If so, how? Are the two related?

What is eco-efficiency? How is it measured? Why is it measured? Where is it reported?

List the main stakeholder groups in a company. Consider whether and why each stakeholder group might be interested in corporate eco-efficiency indicators.What level of information is each group most interested in for decision-making and accountability purposes? Explain.

What is an environmental intervention? How are environmental interventions and eco-efficiency related?

‘Eco-efficiency provides a measure of “win–win”—an action is undertaken if it saves money and environmental interventions are reduced.’ Is eco-efficiency too concerned about saving money rather than helping to preserve the environment?

What are the three steps that can be taken along a corporate eco-efficiency path?How are the five modules related to development of a measure of eco-efficiency?

Why is the distinction between general and specific indicators of eco-efficiency important for accounting in (a) ecological and (b) financial terms?

Benchmarking of eco-efficiency indicators faces a number of practical problems.What are these? Can they be overcome? Why is internal benchmarking more common than external benchmarking?

The objective . . . is not to develop one single approach to measuring and reporting eco-efficiency. Rather it is to establish a general, voluntary framework that is flexible enough to be widely used, broadly accepted and easily interpreted by the full range of businesses.This is based on a

‘Eco-efficiency provides necessary but not sufficient indicators of environmental performance.’ What is environmental performance? Provide an example of another type of information that is important when assessing a company’s environmental performance.

How are the limits on using eco-efficiency indicators related to accounting?

How do stakeholder groups relevant to environmental management accounting and environmentally induced financial accounting differ?

What reasons can you give in support of, and against, the development of separate financial accounting guidelines and standards that reflect the financial consequences of environmental issues?

Information disclosed in financial reports should have a number of characteristics(e.g. understandability, neutrality). What are these characteristics?Provide two examples of situations where there might be a conflict between these different characteristics.

Explain the difference between an asset and an expense in conventional financial accounting. Are pollution permits an asset? Comment on the view that letting companies hold pollution allowances as assets is contrary to the aim of reducing pollution.

Present a critical appraisal of the argument that only one international standardsetting institution is needed to establish financial reporting standards relating to environmental issues.

Tax-deductibility of clean-up costs—asset or liability?The IRS [US Inland Revenue Service] reversed its position on the accounting treatment of environmental clean-up costs in Revenue Ruling 94-38. Such costs arise when owners of real property are required to remove hazardous wastes from their

Distinguish between a liability and an environmental liability. Is there any difference, in principle, between the recognition criteria for normal and environmental liabilities in conventional financial accounting?

What are the advantages and disadvantages of permitting counter-claims for insurance claims to be offset in financial reports? Consider the views of management, shareholders and a non-governmental organisation such as Greenpeace.

If ‘grandfathering’ is accepted as the basis for allocating initial emission permits what is the likely impact on early action (action before trading schemes commence)being taken to reduce emissions? Consider your answer in the context of the emerging mechanism for greenhouse gas emissions

Conventional financial accounting suggests that environmental permits should be measured by using the historical cost principle. One alternative is that current market prices should be used instead. Should exit prices that represent opportunity costs of capital tied up in permits, or current costs

How important are environmental disclosures in the management discussion and analysis section of an annual report? Explain.

What is shareholder value? Given that there is a range of stakeholders interested in corporate environmental impacts, what arguments can be advanced for emphasising shareholders and ‘value’ attributable to them?

Is there a relationship between the number of accounting standards issued and demand for accounting and auditing services? Explain this relationship. Given this relationship, should environmental accounting standards be added to the set of existing standards?

‘Shareholder value is cash-oriented.’ Do you agree with this statement? Give reasons.

Shareholder value, as a concept, faces a number of problems. List these problems. Can any of the problems be overcome?

Are systematic and unsystematic environmental risks related? Why, or why not?Are banks concerned about systematic environmental risks? Are insurance companies concerned about unsystematic environmental risks? Explain.

What set of eco-efficiency characteristics is the shareholder value approach concerned with identifying?

Can option values be used to promote corporate legitimacy?

What are the main characteristics of the conventional accounting and ecological accounting categories? Why is the distinction necessary?

Explain the two major types of measure used in conventional accounting and ecological accounting. When consideration is given to environmental issues in accounting, what are the two main groups of information that stakeholders may be interested in? Provide examples.

What is the difference between management accounting and the other two types of conventional accounting—financial accounting and other accounting systems?

What is the difference between internal ecological accounting and the other two types of ecological accounting—external ecological accounting and other ecological accounting?

Provide one example of a question addressed by each of the three ‘environmentally differentiated conventional accounting’ systems. What distinguishes each of these examples from the questions addressed in ‘conventional accounting’systems?

Link the following environmental transactions and events with the relevant environmental accounting system:1 A tax on emissions of carbon dioxide 2 Capital expenditure on a water-recycling plant 3 A ‘per container’ charge on the profits of managers who do not return empty chemical containers to

What is a stakeholder? Why are some stakeholders interested in comparing measures of corporate economic and ecological performance? Provide an example in which shareholders are the stakeholder group.

Do stakeholders influence environmental accounting systems? Do environmental accounting systems influence stakeholders? Provide an example to illustrate your argument.

Chambers (1999) argues that money and monetary calculation are among the greatest simplifiers of complex affairs.What advantages does the use of a money measure of activity have for decision-makers?

According to Rubenstein (1994: 3):For the first time in accounting’s sleepy history, there is a growing recognition among accountants and nonaccountants alike that accounting, the value-free, balanced system of double entries, may be sending dangerously incomplete signals to business, to

Discuss the following issues relating to criticism of conventional accounting.1 Conventional accounting uses the accrual convention.What is the accrual convention? What is the main benefit of accrual accounting? How might accrual accounting help with the management of environmental issues?2 Explain

What is the concept of ‘bounded rationality’? How might the concept be used to help distinguish between the provision of serviceable and unserviceable accounting information in environmental accounting?

Reactions of stakeholders who do not feel that accounting provides serviceable information include: resignation and loyalty; voice; and exit.1 Why are exit and voice of particular importance as strategies to support the development of environmental accounting?2 From a business perspective, is

Conventional accounting systems are said to have some ‘uncontested advantages’over the absence of accounting systems. What are these ‘uncontested advantages’?

Conventional accounting provides information about a ‘cluster of financial circumstances’that are of concern to all stakeholders.What are these circumstances?

Is there a ‘cluster of physical ecological circumstances’ that can be identified as relevant to all stakeholders? List and relate them to the respective stakeholders.

‘Conventional management accounting systems provide the foundation for all other accounting systems.’What are the main differences and links between conventional management accounting and environmental management accounting?

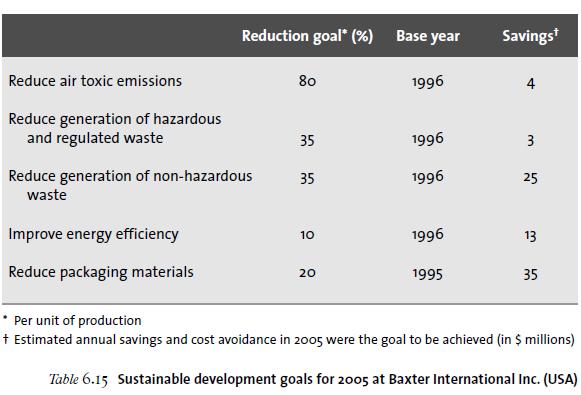

Baxter International Inc. (USA) established the following environmental goals in 1997 for 2005: global targets to cut packaging, energy consumption, toxic emissions to the air and the generation of hazardous and non-hazardous wastes.Relevant estimates are provided in Table 6.15.a What are the total

Use of the term ‘economic cost’ may be contrasted with use of the term‘accounting cost’.The term ‘cost’ is used in different contexts (and by different individuals) with different meanings. It is therefore useful to distinguish the accountant’s use of the term from the economist’s

How do full-cost accounting and full-cost pricing differ? Are they related?

External and internal costs:a How do external and internal environmental costs differ? Provide three examples of an external, and four examples of an internal, environmental cost. In your examples of internal environmental costs include examples of one direct, one indirect, one contingent and one

What are opportunity costs? Why are they important to managers? What is the opportunity cost of not investing in environmental protection? Provide an example to support your answer.

Compare and contrast the following two statements. Are they concerned with achieving eco-efficiency, eco-effectiveness or both?1 Businesses should sack the unproductive kilowatt-hours, tonnes and litres rather than their workforce. This would happen much faster if we taxed labour less and resource

Explain how the notions of effectiveness, efficiency and equity are related to decision-making, sustainable development and accountability.

What is the difference between an accountor and an accountee? Is it important for the needs of both to be taken into account when designing an accounting system? Provide reasons for your view.

Environmental accounting systems have been proposed for sovereign nations as well as for companies. Consider how a macro (national) and a micro (company)view of environmental accounting might differ.

Why is a distinction made between conventional accounting and ecological accounting?

Why has the importance of environmental accounting to business grown in the past ten years?

What is an external stakeholder? Provide an example of a situation where pressure from external stakeholders has pushed managers to engage with environmental issues.

What mechanisms are available to help provide stakeholders with an assurance that a company complies with environmental regulations?

If fines for non-compliance are much higher than ever before, how might increased transparency, brought about by environmental accounting disclosures, still act as a competitive advantage to a company?

What are the reasons for most companies having a poorly co-ordinated collection of environmental data? How are these reasons related to the distinction made between fixed and variable costs of information management systems?

Stakeholders’ views. Broken Hill Proprietary Co. Ltd (BHP). BHP is an Australian-based global mineral resources company. A tailings dam constructed at the Ok Tedi copper and gold mine in Papua New Guinea collapsed leading to over 700 million tonnes of tailings and waste rock being delivered

Costs of information: increasing environmental expenditures. Most major corporations are spending in the tens of millions of dollars annually on environmental costs, with the larger ones spending in the hundreds of millions and some spending more than US$1 billion per year (Epstein 1996: xxv).a

Shell’s statement of business principles (Shell 1998: 24): Principle 6, on health, safety and the environment (HSE).Consistent with their commitment to contribute to sustainable development, Shell companies have a systematic approach to health, safety and environmental management in order to

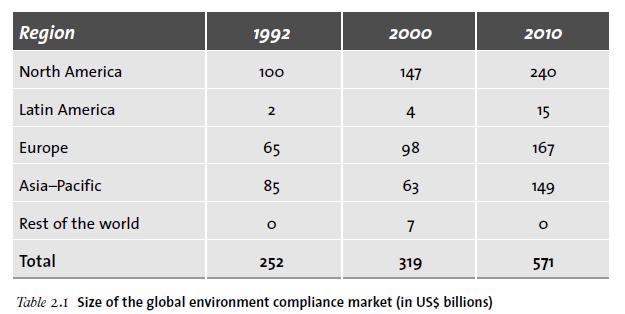

Environmental compliance: a market opportunity. Table 2.1 shows estimates of the size of the market for environmental technologies and services needed to comply with environmental standards. In 1996 the OECD, using a fairly narrow definition of the industry, estimated that the global compliance

Why is involvement of top management important to the success of a corporate environmental management and accounting system?

Distinguish between syntactics, semantics and pragmatics. Are these perspectives independent of each other or are they interwoven?

What is the critical test for any accounting system? Does this test rely on syntactic, semantic or pragmatic perspectives?

Define the two main environmental objectives proposed for management of companies: sustainable development and eco-efficiency. Are these objectives related?

Is sustainable development a useful, practical perspective for business to adopt?If yes, how is it useful? Explain your view, giving reasons.

The efficiency ratio measures the relation between outputs from and inputs to a process. According to the WBCSD, a company wanting to become eco-efficient should strive to:1.Reduce the material intensity of its goods and services 2.Reduce the energy intensity of its goods and services 3.Reduce the

How do ecological product efficiency and ecological function efficiency differ?How are they measured? Are measures of these two types of ecological efficiency linked?

Is a ‘win–win’ situation the only practical way to move business towards sustainability?

Showing 500 - 600

of 692

1

2

3

4

5

6

7

Step by Step Answers