Proudie, Slope and Thorne were in partnership sharing profits and losses in the ratio 3 : 1

Question:

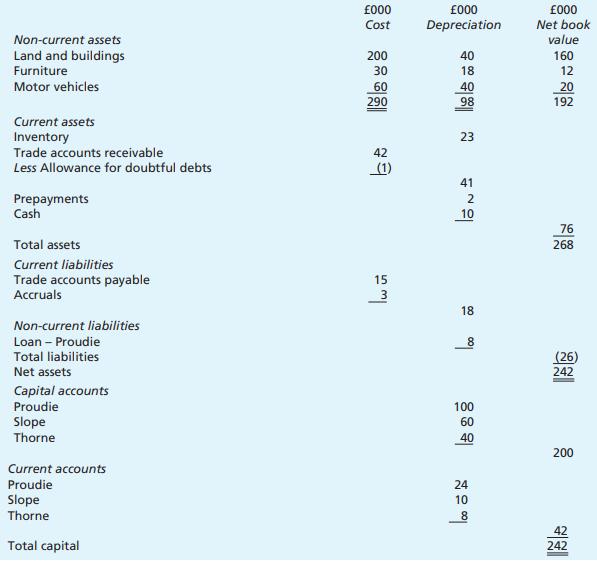

Proudie, Slope and Thorne were in partnership sharing profits and losses in the ratio 3 : 1 : 1. The draft statement of financial position of the partnership as at 31 May 2012 is shown below:

Additional information: 1 Proudie decided to retire on 31 May 2012. However, Slope and Thorne agreed to form a new partnership out of the old one, as from 1 June 2012. They agreed to share profits and losses in the same ratio as in the old partnership. 2 Upon the dissolution of the old partnership, it was agreed that the following adjustments were to be made to the partnership statement of financial position as at 31 May 2012.

(a) Land and buildings were to be revalued at £200,000.

(b) Furniture was to be revalued at £5,000.

(c) Proudie agreed to take over one of the motor vehicles at a value of £4,000, the remaining motor vehicles being revalued at £10,000.

(d) Inventory was to be written down by £5,000.

(e) A bad debt of £2,000 was to be written off, and the allowance for doubtful debts was then to be adjusted so that it represented 5 per cent of the then outstanding trade accounts receivable as at 31 May 2012.

(f) A further accrual of £3,000 for office expenses was to be made. (g) Professional charges relating to the dissolution were estimated to be £1,000.

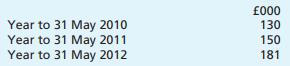

3 It has not been the practice of the partners to carry goodwill in the books of the partnership, but on the retirement of a partner it had been agreed that goodwill should be taken into account. Goodwill was to be valued at an amount equal to the average annual profits of the three years expiring on the retirement. For the purpose of including goodwill in the dissolution arrangement when Proudie retired, the net profits for the last three years were as follows:

The net profit for the year to 31 May 2012 had been calculated before any of the items listed in 2 above were taken into account. The net profit was only to be adjusted for items listed in 2(d), 2

(e) and 2

(f) above. 4 Goodwill is not to be carried in the books of the new partnership. 5 It was agreed that Proudie’s old loan of £8,000 should be repaid to him on 31 May 2012, but any further amount owing to him as a result of the dissolution of the partnership should be left as a long-term loan in the books of the new partnership. 6 The partners’ current accounts were to be closed and any balances on them as at 31 May 2012 were to be transferred to their respective capital accounts. Required:

(a) Prepare the revaluation account as at 31 May 2012.

(b) Prepare the partners’ capital accounts as at the date of dissolution of the partnership, and bring down any balances on them in the books of the new partnership.

(c) Prepare Slope and Thorne’s statement of financial position as at 1 June 2012.

Step by Step Answer:

Frank Woods Business Accounting

ISBN: 9780273759287

12th Edition

Authors: Frank Wood. Sangster, Alan