New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

auditing assurance services

Information Systems Control And Audit 1st Edition Ron Weber - Solutions

You are the partner-in-charge of the external audit of H'ani Diamond Mines Ltd. (HDML), a medium-sized South African diamond mining company with its head office in Johannesburg. Because there has been significant turnover of management during the past year at one of HDML's major mining sites (some

Ferngoods Ltd. is a large Auckland-based white goods manufacturer (e.g., refrigerators, washing machines, stoves) that sells its products throughout the Southeast Asian market. It employs about 1,500 people, and it has large inventories of raw materials, work in process, and finished goods that it

You are an auditor examining the data-entry process for a large Torontobased mail-order retail firm that dispatches goods to customers on behalf of about 30 clients. You are currently focusing on two error types that can occur: (1) the data-entry clerk can enter a wrong amount ordered for an order

Electronic Connections Ltd. (ECL) is a major supplier of computer networkrelated services. It was started by two young programmers in 1963 who purchased a (then) large secondhand mainframe computer to provide timesharing services to customers. ECL expanded it services throughout the 1960s and

Which of the following statements about interviews versus interrogations is true?a. An interrogation requires fewer skills to conduct than an interview because the need to establish rapport with respondents is not as importantb. A respondent in an interview is more likely to be uncooperative than a

In which of the following situations would an interview not be appropriate?a. Determining the impact of an application system on a user's quality of working lifeb. Obtaining advice from operations personnel on which applications are inefficientc. Obtaining the opinions of management on the material

A respondent's motivation to reply to the questions asked during an interview is primarily a function of:a. Whether the respondents perceive the questions asked during the interview to be complex or simpleb. The stress placed on respondents by having to answer the questions asked during the

A tandem interview is an interview conducted:a. With one respondent and two interviewersb. With two or more respondentsc. On two or more separate occasionsd. On a regular rotating basis

In an interview, closed questions should be asked:a. Toward the beginning of an interviewb. Toward the middle of an interviewc. When a complex topic is being examinedd. When a controversial topic must be addressed

Which of the following is most likely to be the best time to conduct an interview?a. Outside normal working hours when respondents will not be distracted by the pressures of workb. Over a meal or break so respondents can relax and attend better to the interviewer's questionsc. Midmorning when

Which of the following is not a rule of protocol to follow when conducting an interview?a. For the most part, be a listener rather than a talkerb. Use technical terms whenever possible to communicate more effectivelyc. Answer all the respondent's questions courteouslyd. Avoid familiarity, and

Tape recorders should be used in an interview only if:a. The prior permission of respondents has been obtainedb. Non sensitive material is to be covered in the interviewc. Respondents do not appear to be nervousd. Respondents' time is at a premium

Which of the following guidelines is most likely to result in the high-quality analysis of an audit interview?a. It should be left until some time after the interview so auditors have a chance to reflect on the information obtainedb. Auditors should show their report to the interviewee to obtain

Which of the following types of questionnaires probably would require the most explanatory information to be included with the questionnaire?a. An internal control questionnaire completed by auditorsb. A questionnaire completed by auditors during an interviewc. A self-administered questionnaire

Which of the following is not a general design guideline for questions to be included in a questionnaire?a. Avoid having more than a few responses to each questionb. Avoid using questions that involve extensive recallc. Avoid using hypothetical questionsd. Avoid using embarrassing questions

Which of the following types of response scales typically is not likely to be used on a questionnaire when opinions are solicited?a. Multi-point scaleb. Semantic differential scalec. Likert scaled. Yes/no scale

In a questionnaire, more difficult questions should:a. Be placed toward the middle and end of the questionnaireb. Require a yes or no response to reduce complexityc. Leave little room for opinion to increase response objectivityd. Be placed toward the beginning of a questionnaire

The representativeness of the sample items on a questionnaire in terms of the domain of interest is a measure of its:a. Construct validityb. Predictive validityc. Face validityd. Content validity

A reliable questionnaire is one that:a. Measures what it is supposed to measure in terms of its underlying constructb. Has only a limited number of questions that the respondent must answerc. Obtains the same responses across repeated administrations of the questionnaired. Predicts the values of

A primary problem with internal control questionnaires used by auditors is:a. They are prone to high response error ratesb. They are completed mechanically after repeated usec. They often have low predictive validityd. They allow no scope for respondents to offer an opinion

Which of the following flowcharting techniques is most likely to form the basis of a control flowchart that shows controls exercised at the logical or functional level in an application system?a. Document flowchartb. Data flow diagramc. System flowchartd. Program flowchart

In the preparation of a control flowchart, the most difficult decisions are usually associated with:a. Choosing the appropriate level of detail at which to workb. Preparing the primary flowchartc. Narrating controls on the primary flowchartd. Choosing the primary flowcharting technique to use

In the preparation of a control flowchart, computer-assisted software engineering tools are most unlikely to assist in:a. Determining the correct position to narrate controls on the control flowchartb. Reducing the amount of time required to prepare the control flowchart in the first placec.

Which of the following aspects of control flowcharts requires the most audit experience for their effective use?a. Choosing the right primary flowcharting technique to describe the features of interest in the application systemb. Correctly modifying the control flowchart in light of changes that

Give five ways in which interviews, questionnaires, and control flowcharts can assist auditors during the conduct of an audit.

Briefly explain the difference between interviewing and interrogation. Why should auditors be careful about becoming involved in an interrogation?

Why do people respond to questions in an interview? Why is it important auditors have an understanding of what motivates a person to respond to questions they might ask during an audit interview?

Why do different types of interviews require varying levels of respondent motivation? Give two examples of audit interviews that auditors might conduct, one that requires a high level of respondent motivation, and one that requires a low level of respondent motivation.

In the structure of an interview, where should general questions be placed? Where should specific questions be placed? Why is placement of questions during an interview important?

Briefly explain the difference between a closed and an open question. What factors affect whether auditors use a closed or an open question during an audit interview?

Briefly outline the factors that auditors should consider when choosing a time and place for an audit interview.

What is meant by establishing rapport with the interviewee during the conduct of an audit interview? Why is establishing rapport important during the conduct of an audit interview? Briefly describe four techniques auditors might use to try to establish or maintain rapport during an interview.

What can auditors do if a confrontation situation arises during an audit interview?

Briefly explain what is meant by a tandem interview. What are the advantages and disadvantages of a tandem interview? Give an example of where auditors might use a tandem interview during the conduct of an audit.

What tasks must auditors perform during the analysis of an audit interview? When should auditors carry out these tasks?

Why must auditors consider who will be the respondent group in the design of an audit questionnaire? What impact does the type of respondent group have on the design of an audit questionnaire?

During the conduct of an audit, how will the characteristics of a selfadministered questionnaire differ from the characteristics of a questionnaire that auditors administer to auditees themselves? When should a selfadministered questionnaire be used? When should a questionnaire that auditors

How do response scales differ for questions asked via an audit questionnaire to obtain factual information versus questions asked to obtain attitudes or opinions?

What is meant by the reliability and validity of a questionnaire? Why must auditors be concerned about reliability and validity issues when they administer questionnaires during an audit?

What advantages do standardized questionnaires offer to auditors in the conduct of their audit work? Does their use have any disadvantages?

One problem with using the same audit questionnaire on a routine basis is the problem of "cheating." Explain briefly.

Give three problems of mail questionnaires. Outline some techniques that auditors can use to overcome these problems when they employ mail questionnaires during the conduct of an audit.

What is a control flowchart? What are the purposes of a control flowchart?

Briefly describe the nature and purposes of four types of control flowchart that auditors might construct during their audit work.

Outline the steps that must be undertaken when constructing a control flowchart. Be sure to indicate the critical decisions that must be made at each step.

For each of the four types of control flowcharts described in the chapter, give a strength and a limitation.

How might the availability of flowcharting software assist auditors to prepare and maintain control flowcharts they construct during the conduct of an audit?

A major advantage of control flowcharts is that they can be prepared and used effectively by auditors who have little knowledge of data processing controls. Discuss briefly.

To what extent is the hypothesized usefulness of flowcharts supported by empirical research results?

You are the manager of internal auditor for Kukup Manufacturing Ltd., which is a large, diversified manufacturing company based in Kuala Lumpur, Malayasia. Kukup has well-established computer systems to support its operations. The internal audit group that you manage, however, was established only

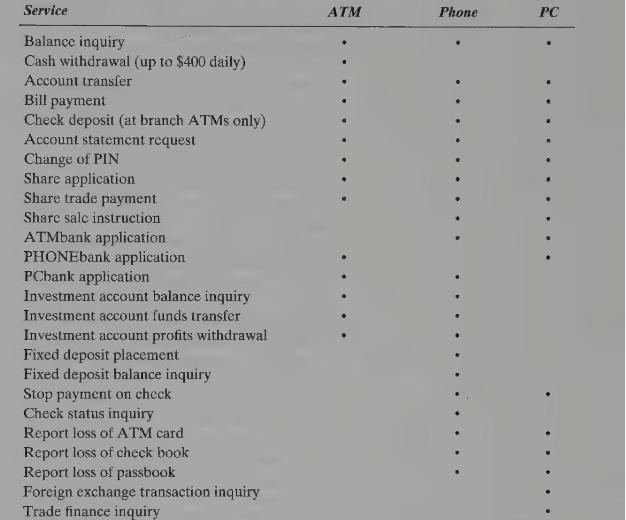

The New Hong Kong Chinese Banking Corporation (NHKCBC) is a large Hong Kong-based bank that offers a wide range of retail and wholesale banking services. Retail customers can access services in four ways: over the counter (COUNTERbank); via automatic teller machines (ATMbank); via telephone

Finer Furnishings Limited is a Vancouver-based company that makes an extensive range of furniture for sale throughout North America. While it produces a wide range of standard lines of furniture, many of its products are also custom designed in light of extensive discussions conducted with its

Swagmans Banking Corporation is a large Australian bank based in Melbourne. It offers a wide range of services to customers in Australia through an extensive network of branches.Swagmans has decided to offer its customers a share trading service. Customers can call a toll-free number 24 hours a

You are the manager of internal audit for a large North America-based financial institution. One day your staff report to you that they have discovered an error in the amount of interest paid to a significant number of depositors. Your institution has overpaid several million dollars of interest as

Briefly explain the nature of concurrent auditing techniques.

Why has the disappearance of paper-based audit trails motivated the implementation and use of concurrent auditing techniques?

Why is there often a need for continuous monitoring of advanced information systems? How do concurrent auditing techniques facilitate continuous monitoring of advanced information systems?

Why has it become more difficult for auditors to perform transaction walkthroughs with application systems? How can concurrent auditing techniques assist auditors to perform transaction walkthroughs?

What is entropy? Information systems staff often have a very high rate of turnover in their jobs. Is this a form of entropy in information systems? If so, how can concurrent auditing techniques be used to help mitigate the effects of this form of entropy?

How can auditors use concurrent auditing techniques to monitor application systems that are developed, implemented, operated, and maintained on behalf of an organization by an outsourcing vendor?

Why are concurrent auditing techniques useful in monitoring the authenticity, accuracy, and completeness of transaction processing in distributed application systems?

Briefly describe the nature of ITF.

Describe two methods of entering test data for an ITF application and discuss the relative advantages and disadvantages of each method.

Describe two methods of removing the effects of ITF transactions and the relative advantages and disadvantages of each method.

Outline the difference between the snapshot and extended record concurrent auditing techniques.

What are three major design decisions auditors must make when implementing the snapshot/extended record concurrent auditing technique?

Briefly describe the nature of the SCARF concurrent auditing technique. Discuss how snapshot and SCARF might be integrated with one another.

A properly written input program for an application system should contain the program code needed to undertake comprehensive validation of input data. Why might auditors still be interested in using SCARF embedded audit modules to check whether input data is valid?

Briefly describe three types of evidence that auditors might collect using the SCARF concurrent auditing technique.

What decisions must auditors make in determining the structure of the reporting system to be used with the SCARF concurrent auditing technique?

Briefly describe the nature of the CIS concurrent auditing technique.

Briefly describe each of the major steps that must be undertaken during the execution of the continuous and intermittent simulation (CIS) technique.

Give one advantage and one disadvantage of continuous and intermittent simulation with respect to (a) SCARF and (b) parallel simulation.

What are two types of cost externalities that auditors impose on other groups when using a concurrent auditing technique?

Why do auditors need to consult with other groups whenever they implement a concurrent auditing technique?

Do auditors need high levels of expertise with information systems audit and control to be able to use concurrent auditing techniques successfully? Why or why not?

Why do auditors need to seek the support of other groups whenever they implement a concurrent auditing system? In particular, why do they need the support of management?

Give one major design decision that auditors must make whenever they implement:a. Integrated test facilityb. Snapshot/extended recordc. System control audit review filed. Continuous and intermittent simulation

In our planning of the design and implementation of a concurrent auditing technique, give two factors we must consider in deciding how we will use a concurrent auditing technique once it is implemented.

Why must auditors take great care in testing a concurrent auditing technique before they release it into production use?

Give two purposes of carrying out a postaudit on the use of a concurrent auditing technique.

Give two advantages of using concurrent auditing techniques in an organization.

Are concurrent auditing techniques used extensively in practice? Based on empirical research that has been conducted, give three factors that seem to affect whether a concurrent auditing technique will be used within an organization.

Give two limitations of using concurrent auditing techniques within an organization.

Which of the following is not a justification for using concurrent auditing techniques?a. Cheaper to implement, operate, and maintain than ex post auditing techniquesb. Increasing difficulties of performing walkthroughsc. More timely identification of errors and irregularities needed in advanced

Entropy, the tendency of a system toward disorder, is present in:a. Only systems with weak controlsb. All systemsc. Only advanced systems that are complexd. Only systems with a high level of coupling

Relative to designing new test data, tagging live transactions in an ITF has the advantage that:a. Special audit routines do not have to be embedded in the host systemb. The limiting conditions in the system are more likely to be testedc. Source documents and data-entry screens do not have to be

Which of the following advantages is common to submitting reversal entries and submitting trivial transactions as two means of removing the effects of ITF transactions?a. The limiting values in the host system can be testedb. ITF activities are transparent to usersc. No costs and risks are involved

The snapshot technique involves:a. Recording the state of an application system's working storage at a point in timeb. Taking pictures of a transaction as it flows through a systemc. Evaluating the afterimages of all data items changed for accuracy and completenessd. Providing a filter in the input

The difference between the snapshot technique and the extended record technique is:a. With the extended record technique, record images that are collected at different points in an application system are stored contiguously, whereas with snapshot they are stored separatelyb. More audit evidence is

Which of the following types of information cannot be collected using SCARF?a. Statistical samplesb. Policy and procedural variancesc. Lack of internal program documentationd. Performance measurement data

The purpose of using CALL statements only in the source code of a program to invoke SCARF routines is to:a. Improve the efficiency with which data can be collected via the SCARF routinesb. Highlight those places in the programming code associated with an application system where SCARF routines

The choice of sort codes in the SCARF reporting system is important because it:a. Determines whether a high-level or a low-level programming language can be used to implement the systemb. Affects the decision on how long the interval must be before SCARF reports can be issued for audit scrutinyc.

Which of the following is the primary difference between SCARF and CIS?a. CIS is unable to collect data to be used for performance monitoring purposes, whereas SCARF can be used to collect evidence to judge the host application system's efficiencyb. CIS is invoked by the database management system

Which of the following functions is not performed by the database management system when the CIS concurrent auditing technique is used?a. It invokes CIS and passes transactions across to CIS for examinationb. It provides CIS with all the data requested by the application system to process the

When compared with parallel simulation, which of the following is most likely to be a disadvantage of the CIS concurrent auditing technique?a. It is more difficult to implement because it is intended for use in an online rather than a batch processing environmentb. It requires more program

Which of the following is not a reason for interacting with information systems staff when auditors design and implement concurrent auditing techniques?a. The cooperation of information systems staff will be needed if the existence of concurrent auditing techniques is not to be disclosed to

Which of the following statements about use of concurrent auditing techniques in practice is true?a. They are used more frequently than generalized audit software and utility softwareb. The most popular form of concurrent auditing technique is continuous and intermittent simulation (CIS)c. Over

Which of the following factors is most likely to lead to more extensive use of concurrent auditing techniques within an organization?a. Application systems have been programmed in high-level languages rather than low-level languagesb. The concurrent auditing techniques have been requested by the

Which of the following is likely to be the most important disadvantage of using concurrent auditing techniques?a. They can provide evidence about only a limited set of features in an application system that interest the auditorb. Only a few types of application systems can accommodate the audit

Showing 400 - 500

of 2689

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers