New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

financial institutions management

Financial Institutions Management A Risk Management Approach 11th International Edition Anthony Saunders, Marcia Millon Cornett, Otgo Erhemjamts - Solutions

Use the following information on a one-year loan commitment to calculate the return on the loan commitment.BR = FI’s base interest rate on the loans = 8%φ = Risk premium on loan commitment = 2.5%f1 = Upfront fee on the whole commitment = 25 basis points f2 = Back-end fee on the average unused

Suburb Bank has issued a one-year loan commitment of $10 million for an upfront fee of 50 basis points. The back-end fee on the unused portion of the commitment is 20 basis points. The bank’s base rate on loans is 7 percent and loans to this customer carry a risk premium of 2 percent. The bank

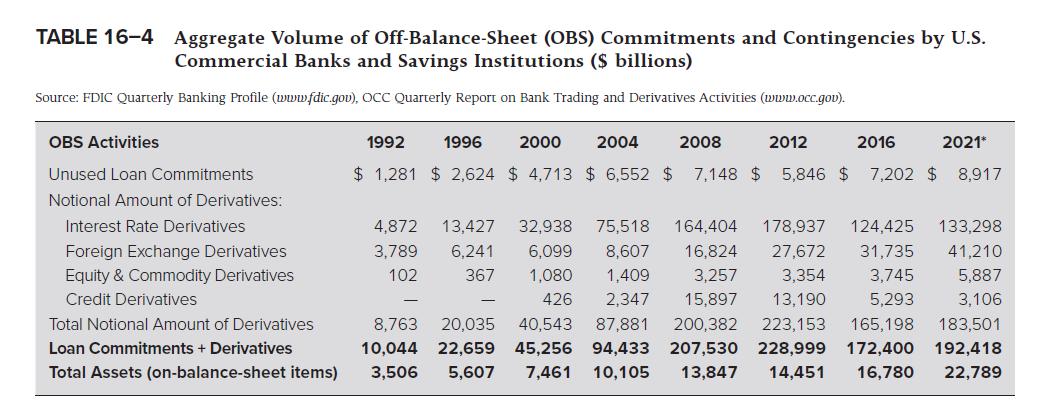

Go to the FDIC website at www.fdic.gov and find the total amount of unused commitments of FDIC-insured commercial banks for the most recent quarter available using the following steps. Click on “Analysis.” From there click on the latest “Quarterly Banking Profile.” Next click on “Balance

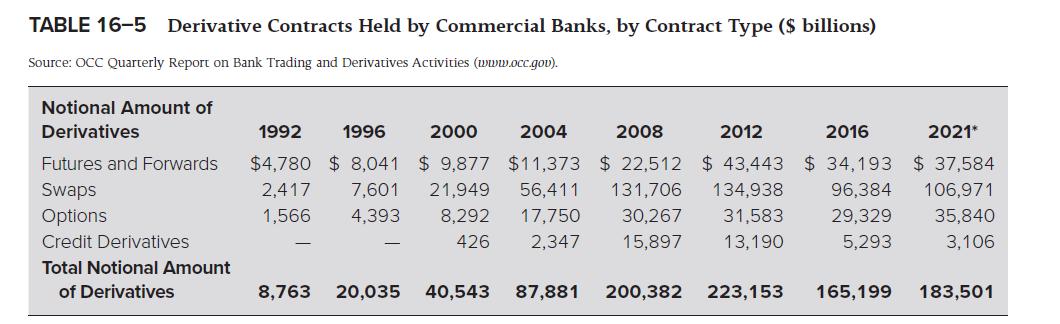

Go to the website of the Office of the Comptroller of the Currency at www.occ. treas.gov and update Table 16–5 using the following steps. Click on “Publications& Resources,” and then “Publications.” Click on “Quarterly Report on Bank Trading and Derivatives Activities.” Click on

Just as banks paid out billions in settlements over LIBOR manipulation, they also paid billions in fines to the Department of Justice for creating and selling toxic mortgage-backed securities. Describe the sources of operational risks that can lead to mortgage fraud, negligent underwriting

Related to a third-party risk is so called fourth-party risk. Fourth parties are those entities to which FI’s third parties may outsource or use for certain tasks. How do you address this issue and keep it from becoming a rabbit hole?

What are two risk factors involved in an FI’s investment of resources in innovative technological products?

What is the link between interstate banking restrictions and the retail demand for electronic payment services?

Does the existence of economies of scale for FIs mean that in the long run, small FIs cannot survive?

If there are diseconomies of scope, do specialized FIs have a relative cost advantage or disadvantage over product-diversified FIs?

Make a list of the potential economies of scope or cost synergies if a commercial bank merged with an investment bank.

Describe the six risks faced by FIs with the growth of wire transfer payment systems.

Why do daylight overdrafts create more of a risk problem for banks on CHIPS than on Fedwire?

What steps have the members of CHIPS taken to lower settlement, or daylight overdraft, risk?

What are the three approaches proposed by the Basel Committee on Banking Supervision for measuring capital requirements associated with operational risk?

What steps have been or are being taken to ensure privacy and protection against fraud in the use of personal and financial consumer information placed on the Internet?

Describe the sources of operational risk. Use some specific examples.

What is cybersecurity risk? What are the primary methods of breaching data systems?Use some specific examples.

What is technology vendor and third-party risk? What actions have regulators taken with respect to third-party risk management?

What information on the operating costs of FIs is provided by the measurement of economies of scope?

Go to the BIS website at www.bis.org/statistics/payment_stats.htm and find the most recent data on the volume and value of payment system transactions in the United States (Table 17–1) using the following steps. Click on “BIS Statistics Explorer.” Click on “United States.” This will bring

Go to the BIS website at www.bis.org/statistics/payment_stats.htm and find the most recent data on the participation in major payment systems (Table 17–3).Click on “BIS Statistics Explorer.” Click on “United States.” This will bring Table 7 which contains data on participation in major

What is risk of digital disruption from fintech and big tech firms?

What are the supply factors that contributed to the recent emergence of fintechs?

What are the demand factors that contributed to the recent emergence of fintechs?

What is stablecoin? What is the primary use of stablecoin?

What is CBDC? Why are they being explored by central banks?

What is DeFi? What are the risks and rewards of DeFi?

Describe applications of artificial intelligence and machine learning in financial services industry.

Explain one of the reasons why high-frequency trading (HFT) has hita speed bump. Do you think fintechs will experience the same difficulties that HFT firms have experienced?

Why do regulators set minimum liquid asset requirements for FIs?

Can we view reserve requirements as a tax when the consumer price index (CPI) is falling?

In general, would it be better to hold three-month T-bills or 10-year T-notes as buffer assets? Explain.

In addition to the target reserve ratio, what other pieces of information does a DI reserve manager require to manage the DI’s reserve requirement position?

For a DI that undershoots its reserve target, what ways are available to a reserve manager to build up reserves to meet the target?

Since 1998, U.S. DIs have operated under a lagged reserve accounting system in which the reserve computation period ends 17 days before the reserve maintenance period begins. Does the reserve manager face any uncertainty at all in managing a DI’s reserve position? Explain your answer.

What explains the decline in the level of required reserves held by DIs between 1990 and August 2008 and the rise in August of 2009 (see Table 19A–3)?

How are liquidity and liability management related?

Describe the trade-off faced by an FI manager in structuring the liability side of the balance sheet.

Describe the withdrawal risk and funding cost characteristics of some of the major liabilities available to a modern DI manager.

Since transaction accounts are subject to both reserve requirements and deposit insurance premiums, whereas fed funds are not, why should a DI not fund all its assets through fed funds? Explain your answer.

What are the major differences between fed funds and repurchase agreements?

Look at Table 19–2. How has the ratio of traditional liquid to illiquid assets changed over the 1960–2021 period? TABLE 19-2 Liquid Assets versus Nonliquid Assets for Insured Commercial Banks, 1960 and 2021 (in percentages) Source: Federal Deposit Insurance Corporation website. www.fdic.gov

Look at Table 19–3. How has the liability composition of banks changed over the 1960–2021 period? TABLE 19-3 Liability Structure All Banks Liabilities and Capital 12/31/60 09/30/21 09/30/21 All Banks Large Banks* Small Banks* 09/30/21 of Insured Transaction accounts 61.00% 25.23% 24.73% 35.40%

Discuss two strategies insurance companies can use to reduce liquidity risk.

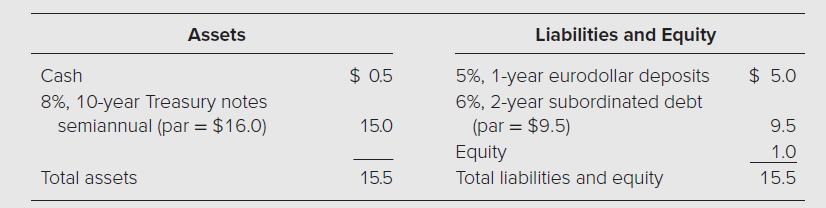

Consider the assets (in millions) of two banks, A and B. Both banks are funded by\($120\) million in deposits and \($20\) million in equity. Which bank has the stronger liquidity position? Which bank probably has a higher profit? Bank A Assets Bank B Assets Cash $ 10 Cash $ 20 Treasury securities

Rank the following liabilities with respect, first, to funding risk and, second, to funding cost.a. Money market deposit account.b. Demand deposits.c. Certificates of deposit.d. Federal funds.e. Bankers’ acceptances.f. NOW accounts.g. Wholesale CDs.h. Passbook savings.i. Repos.j. Commercial paper.

Go to the Federal Deposit Insurance Corporation’s website at https://www7.fdic.gov/sdi/index.asp and update Tables 19–2 and 19–3 using the following steps. Click on “Create or Modify Reports.” In the second column, select “Standard Peer Group,” “Assets more than $1B.” In the third

What events led to Congress’s passing of the FDIC Improvement Act (FDICIA)?

What events brought about the demise of the FSLIC?

What two basic views are offered to explain why depository institution insurance funds become insolvent?

Why was interest rate risk less of a problem for banks than for thrifts in the early 1980s?

Historically, what effect has deposit insurance had on DI panics and runs?

Bank A has a ratio of deposits to assets of 90 percent and a variance of asset returns of 10 percent. Bank B has a ratio of deposits to assets of 85 percent and a variance of asset returns of 5 percent. Which bank should pay the higher insurance premium?

If deposit insurance is similar to a put option, who exercises that option?

If you are managing a DI that is technically insolvent but has not yet been closed by the regulators, would you invest in Treasury bonds or real estate development loans? Explain your answer.

Do we need both risk-based capital requirements and risk-based insurance premiums to discipline shareholders?

Under current deposit insurance rules, how can DI depositors achieve many times the $250,000 coverage cap on deposits?

Why do uninsured depositors benefit from a too-big-to-fail policy followed by regulators?

Make up a simple balance sheet example to show a case where the FDIC can lose even when it uses an IDT to resolve a failed DI.

What measures were mandated by the FDICIA to bolster regulator discipline?

Is a DI’s access to the discount window as effective as deposit insurance in deterring bank runs and panics? Why or why not?

How do state-sponsored guaranty funds for insurance companies differ from deposit insurance?

What specific protection against insolvencies does the Securities Investor Protection Corporation provide to securities firm customers?

What is capital forbearance? How does a policy of forbearance potentially increase the costs of financial distress to the deposit insurance fund as well as the stockholders?

What four factors were provided by the FDICIA as guidelines to assist the FDIC in the establishment of risk-based deposit insurance premiums? What happened to the level of deposit insurance premiums in the late 1990s and 2000s? Why?

Under what conditions may the implementation of minimum capital guidelines, either risk based or non-risk based, fail to impose stockholder discipline as desired by regulators?

What is the primary goal of the FDIC in employing the LCR strategy?a. How is the insured depositor transfer method implemented in the process of failure resolution?b. Why does this method of failure resolution encourage uninsured depositors to more closely monitor the strategies of DI managers?

In what ways did the FDICIA enhance the regulatory discipline to help reduce moral hazard behavior? What has the operational impact of these directives been?

Why is access to the discount window of the Fed less of a deterrent to DI runs than deposit insurance?

What was the purpose of the establishment of the Pension Benefit Guaranty Corporation (PBGC)?a. How does the PBGC differ from the FDIC in its ability to control risk?b. How were the 1994 Retirement Protection Act and the Deficit Reduction Act of 2005 expected to reduce the deficits experienced by

Webb Bank has a composite Capital Adequacy, Asset Quality, Management, Earnings, Liquidity, and Sensitivity (CAMELS) rating of 2, a total risk-based capital ratio of 10.2 percent, a Tier 1 risk-based capital ratio of 6.2 percent, a CET1 leverage ratio of 5.0 percent, and a Tier I leverage ratio of

Million Bank has a composite CAMELS rating of 2, a total risk-based capital ratio of 9.8 percent, a Tier I risk-based capital ratio of 6.8 percent, a CET1 leverage ratio of 6.0 percent, and a Tier I leverage ratio of 4.9 percent. The average total assets of the bank equal $500 million, and average

Go to the FDIC website at www.fdic.gov. Click on “Analysis” and then click on“Latest Profile” under “Quarterly Banking Profile.” After selecting a quarter, click on “Access QBP” and then “Complete QBP-PDF.” Search for “Table II-C. Problem Institutions and Failed/Assisted

Why is an FI economically insolvent when its net worth is negative?

Why does market value accounting produce a more accurate picture of a DI’s net worth than book value accounting?

What are the arguments against the use of market value accounting for DIs?

What are the major strengths of the risk-based capital ratios?

You are a DI manager with a total risk-based capital ratio of 6 percent. Discuss four strategies to meet the required 8 percent ratio in a short period of time without raising new capital.

Why is a capital requirement not levied on exchange-traded derivative contracts?

What is the difference between Tier I capital and Tier II capital?

Identify one asset in each of the credit risk weight categories.

What are the risk-weighted assets in the denominator of the common equity Tier I (CET1) risk-based capital ratio, the Tier I risk-based capital ratio, and the total risk-based capital ratio?

How is the leverage ratio for a DI defined?

Explain the process of calculating risk-weighted on-balance-sheet assets.

Under Basel III, how are residential 1–4 family mortgages assigned to a risk class?

National Bank has the following balance sheet (in millions) and has no offbalance-sheet activities.a. What is the CET1 risk-based ratio?b. What is the Tier I risk-based capital ratio?c. What is the total risk-based capital ratio?d. What is the leverage ratio?e. In what capital category would the

What is the capital conservation buffer? How would this buffer affect your answers to question 18?

Onshore Bank has $20 million in assets with risk-weighted assets of $10 million.CET1 capital is $500,000, additional Tier I capital is $50,000, and Tier II capital is $400,000. How will each of the following transactions affect the value of the CET1, Tier I, and total capital ratios? What will the

Explain the process of calculating risk-weighted off-balance-sheet contingent guaranty contracts.a. What is the basis for the use of the credit equivalent amounts of contingent guaranty contracts rather than the face value of these contracts?b. On what basis are the risk weights for the credit

Explain how off-balance-sheet market contracts, or derivative instruments, differ from contingent guaranty contracts.a. What is counterparty credit risk?b. Why do exchange-traded derivative security contracts have no capital requirements?c. What is the difference between the potential future

What is the contribution to the risk-weighted asset base of the following items under the Basel III requirements?a. $10 million cash.b. $50 million 91-day U.S. Treasury bills.c. $25 million cash items in the process of collection.d. $5 million U.K. government bonds, with external rating of AAA.e.

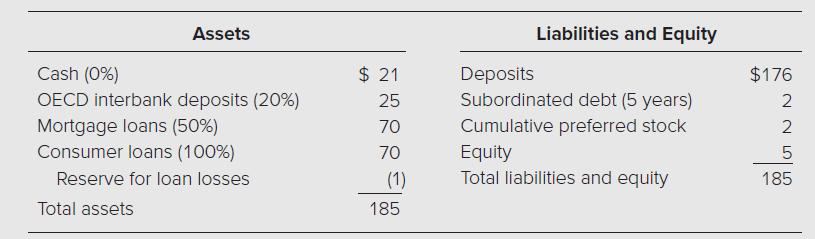

Third Bank has the following balance sheet (in millions) with the risk weights in parentheses.The cumulative preferred stock is qualifying and perpetual. In addition, the bank has $30 million in performance-related standby letters of credit (SLCs) to a public corporation, $40 million in two-year

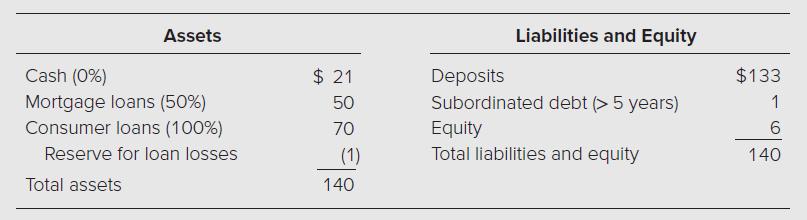

Third Fifth Bank has the following balance sheet (in millions) with the risk weights in parentheses.In addition, the bank has $20 million in commercial direct credit substitute standby letters of credit to a public corporation and $40 million in 10-year FX forward contracts that are in the money by

An investment bank specializing in fixed-income assets has the following balance sheet (in millions). Amounts are in market values and all interest rates are annual unless indicated otherwise.a. Does the investment bank have sufficient liquid assets per the net capital rule? Is the investment bank

A life insurance company has estimated capital requirements for each of the following risk classes: asset risk-affiliate (C0) = $2 million, asset-risk common stock(C1cs) = $5 million, asset-risk other investments (C1o) = $1.5 million, insurance risk (C2) = $4 million, interest rate risk (C3a) =

Offer support for the claim that product expansion restrictions have affected commercial banks more than any other type of financial services firm.

What sources of competition have had an impact on the asset side of banks’ balance sheets?

What was the rationale for the passage of the Glass-Steagall Act in 1933? What permissible underwriting activities did it identify for commercial banks?

Does a bank that currently specializes in making consumer loans but makes no commercial loans qualify as a nonbank bank?

Showing 3900 - 4000

of 4618

First

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

Step by Step Answers