New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

financial institutions management

Financial Institutions Management A Risk Management Approach 11th International Edition Anthony Saunders, Marcia Millon Cornett, Otgo Erhemjamts - Solutions

Referring to Figure 10–4, explain why credit card loan rates are much higher than car loan rates. 0.0% 02/1972 03/1973. 04/1974 5.0% 10.0% 05/1975 06/1976- 07/1977 08/1978 09/1979. 10/1980- 11/1981 12/1982- 01/1984- 02/1985- 15.0% 20.0% 03/1986 04/1987- 05/1988 06/1989- 07/1990 08/1991. 09/1992

Calculate the promised return (k) on a loan if the base rate is 13 percent, the risk premium is 2 percent, the compensating balance requirement is 5 percent, fees are½ percent, and reserve requirements are 10 percent. (16.23%)

What is the expected return on this loan if the probability of default is 5 percent? (10.42%)

Can an FI’s expected return on its loan portfolio increase if it cuts its loan rates?

What might happen to the expected return on a wholesale loan if an FI eliminates its fees and compensating balances in a low-interest rate environment?

Is it more costly for an FI manager to assess the default risk exposure of a publicly traded company or a small, single-proprietor firm? Explain your answer.

How do loan covenants help protect an FI against default risk?

Make a list of key borrower characteristics you would assess before making a mortgage loan.

How should the risk premium on a loan be affected if there is a reduction in a borrower’s leverage?

Suppose an estimated linear probability model looked as follows: Z = 0.03X1 +0.01X2 + error, where X 1 = Debt-to-equity ratio X 2 = Total assets-to-working capital ratio Suppose, for a prospective borrower, X1 = 1.5 and X2 = 3.0. What is the projected probability of default for the borrower? (7.5%)

Suppose X3 = 0.5 in Example 10–3. Show how this would change the default risk classification of the borrower. (Z = 3.95)

What are two problems in using discriminant analysis to evaluate credit risk?

What is the difference between the marginal default probability and the cumulative default probability?

How should the posting of collateral by a borrower affect the risk premium on a loan?

In Table 10–7, the cumulative default probability over three years for CCC-rated corporate bonds is 33.75 percent.Check this calculation using the individual year MMRs. TABLE 10-7 Mortality Rates by Original Rating-All Rated* Corporate Bonds Source: E. L. Altman, "Credit Cycle Outlook and the

Why would any FI manager buy loans that have a cumulative default probability of 33.75 percent? Explain your answer.

Describe the basic concept behind RAROC models.

Which is the only credit risk model discussed in this section that is really forward looking?

What is the link between the implied volatility of a firm’s assets and its expected default frequency?

Differentiate between a secured loan and an unsecured loan. Who bears most of the risk in a fixed-rate loan? Why would FI managers prefer to charge floating rates, especially for longer-maturity loans?

Why is commercial lending declining in importance in the United States? What effect does this decline have on overall commercial lending activities?

Why are rates on credit cards generally higher than rates on car loans?

What are compensating balances? What is the relationship between the amount of compensating balance requirement and the return on the loan to the FI?

Suppose that a bank does the following:a. Sets a loan rate on a prospective loan at 8 percent (where BR = 5% and ϕ = 3%).b. Charges a 1 ⁄ 10 percent (or 0.10 percent) loan origination fee to the borrower.c. Imposes a 5 percent compensating balance requirement to be held as non-interestbearing

Why could a lender’s expected return be lower when the risk premium is increased on a loan? In addition to the risk premium, how can a lender increase the expected return on a wholesale loan?

What are covenants in a loan agreement? What are the objectives of covenants?

Suppose the estimated linear probability model used by an FI to predict business loan applicant default probabilities is PD = 0.03X1 + 0.02X2 – 0.05X3 + error, where X1 is the borrower’s debt/equity ratio, X2 is the volatility of borrower earnings, and X3 is the borrower’s profit margin. For

Suppose that the financial ratios of a potential borrowing firm take the following values:Working capital/Total assets ratio (X1) = 0.75 Retained earnings/Total assets ratio (X2) = 0.10 Earnings before interest and taxes/Total assets ratio (X3) = 0.05 Market value of equity/Book value of total

MNO Inc., a publicly traded manufacturing firm in the United States, has provided the following financial information in its application for a loan. All numbers are in thousands of dollars.Also assume sales = $500,000; cost of goods sold = $360,000; and the market value of equity is equal to the

Carman County Bank (CCB) has a $5 million face value outstanding adjustable-rate loan to a company that has a leverage ratio of 80 percent. The current riskfree rate is 6 percent and the time to maturity on the loan is exactly ½ year. The asset risk of the borrower, as measured by the standard

Go to the Federal Reserve Board’s website at www.federalreserve.gov and update the data in Table 10–1 using the following steps. Click on “Data.” Click on “Assets and Liabilities of Commercial Banks in the U.S.” This downloads a file onto your computer that contains the relevant data.

Go to the Federal Reserve Board’s website at www.federalreserve.gov and update the data in Table 10-2 using the following steps. Click on “Data.” Click on “Assets and Liabilities of Commercial Banks in the U.S.” This will bring up on your computer the files that contain individual loan

Go to the FRED database website from the Federal Reserve Bank of St. Louis at http://fred.stlouisfed.org and update the data for Figure 10-4 using the following steps. Type “48-month auto loan” in the search window and click Enter.Clicking on the “Finance Rate on Consumer Installment Loans at

In Example 11–1, what would the concentration limit be if the loss rate on bad loans is 25 cents on the dollar? (60 percent) EXAMPLE 11-1 Calculating Concentration Limits for a Loan Portfolio Suppose management is unwilling to permit losses exceeding 15 percent of an Fl's capital to a particular

In Example 11–1, what would the concentration limit be if the maximum loss (as a percent of capital) is 10 percent instead of 15 percent? (25 percent) EXAMPLE 11-1 Calculating Concentration Limits for a Loan Portfolio Suppose management is unwilling to permit losses exceeding 15 percent of an

What is the main point in using MPT for loan portfolio risk?

Why would an FI not always choose to operate with a minimum risk portfolio?

How does Moody’s Analytics measure the return on a loan?

If EDF = 0.1 percent and LGD = 50 percent, what is the unexpected loss (σi) on the loan? (1.58 percent)

How does Moody’s Analytics calculate loan default correlations?

Suppose the returns on different loans are independent. Would there be any gains from loan portfolio diversification?

How would you find the minimum risk loan portfolio in a modern portfolio theory framework?

Should FI managers select the minimum risk loan portfolio? Why or why not?

Explain the reasoning behind the Federal Reserve’s 1994 decision to rely more on a subjective rather than a quantitative approach to measuring credit concentration risk. Is that view valid today?

How do loan portfolio risks differ from individual loan risks?

An FI has set a maximum loss of 2 percent of total capital as a basis for setting concentration limits on loans to individual firms. If it has set a concentration limit of 25 percent of capital to a firm, what is the expected loss rate for that firm?

Suppose that an FI holds two loans with the following characteristics: Loani X R +2 1 0.55 0.45 10 07 8% 8.55% 73.1025% P12=0.24 9.15 83.7225 012= 18.7758

The Bank of Tinytown has two $20,000 loans with the following characteristics:Loan A has an expected return of 10 percent and a standard deviation of returns of 10 percent. The expected return and standard deviation of returns for loan B are 12 percent and 20 percent, respectively.a. If the

Suppose that an FI holds two loans with the following characteristics.Calculate the return and risk on the two-asset portfolio using Moody’s Analytics RiskFrontier. Annual Spread between Loan Rate and FI's Loan X Cost of Funds 1 0.45 5.5% 2 0.55 3.5 Loss to FI Expected Given Annual Fees Default

CountrySide Bank uses Moody’s Analytics RiskFrontier to evaluate the riskreturn characteristics of the loans in its portfolio. A specific $10 million loan earns 2 percent per year in fees and the loan is priced at a 4-percent spread over the cost of funds for the bank. Because of collateral

Suppose that an FI holds two loans with the following characteristics.The return on loan 1 is R1 = 6.25%, the risk on loan 2 is σ2 = 1.8233%, and the return of the portfolio is Rp = 4.555%. Calculate of the loss given default on loans 1 and 2, the proportions of loans 1 and 2 in the portfolio, and

What databases are available that contain loan information at the national and regional levels? How can they be used to analyze credit concentration risk?

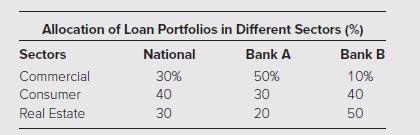

Information concerning the allocation of loan portfolios to different market sectors is given below.Bank A and Bank B would like to estimate how much their portfolios deviate from the national average.a. Which bank is further away from the national average?b. Is a large standard deviation

From Table 11A–1, what is the probability of a loan upgrade? A loan downgrade?a. What is the impact of a rating upgrade or downgrade?b. How is the discount rate determined after a credit event has occurred?c. Why does the probability distribution of possible loan values have a negative skew?d.

What are the sources of liquidity risk?

Why is cash more liquid than loans for an FI?

List two benefits and two costs of using (a) purchased liquidity management and(b) stored liquidity management to meet a deposit drain.

What are the three major sources of DI liquidity? What are the two major uses?

What are the measures of liquidity risk used by FIs?

What is likely to be a life insurance company’s first source of liquidity when premium income is insufficient?

Can a life insurance company be subjected to a run? If so, why?

What is the greatest cause of liquidity exposure faced by property–casualty insurers?

Is the liquidity risk of property–casualty insurers in general more or less than that of life insurers?

What would be the impact on their liquidity needs if DIs offered deposit contracts of an open-end mutual fund type rather than the traditional all-or-nothing demand deposit contract?

How do the incentives of mutual fund investors to engage in runs compare with the incentives of DI depositors?

What are the two reasons that liquidity risk arises? How does liquidity risk arising from the liability side of the balance sheet differ from liquidity risk arising from the asset side of the balance sheet? What is meant by fire-sale prices?

The probability distribution of the net deposit drains of a DI has been estimated to have a mean of 2 percent and a standard deviation of 1 percent. Is this DI increasing or decreasing in size? Explain.

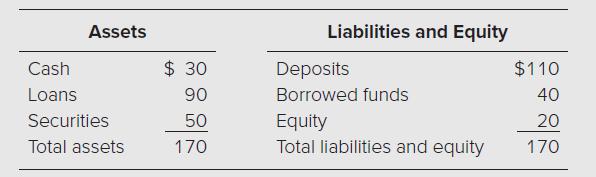

AllStarBank has the following balance sheet (in millions):AllStarBank’s largest customer decides to exercise a $15 million loan commitment.How will the new balance sheet appear if AllStar uses the following liquidity risk strategies?a. Stored liquidity management.b. Purchased liquidity

Define each of the following four measures of liquidity risk. Explain how each measure would be implemented and utilized by a DI.a. Financing gap and financing requirement.b. Sources and uses of liquidity.c. Peer group ratio comparisons.d. Liquidity index.

Plainbank has $10 million in cash and equivalents, $30 million in loans, and $15 million in core deposits.a. Calculate the financing gap.b. What is the financing requirement?c. How can the financing gap be used in the day-to-day liquidity management of the bank?

A DI has the following assets in its portfolio: $10 million in cash reserves with the Fed, $25 million in T-bills, and $65 million in mortgage loans. If the DI has to liquidate the assets today, it will receive only $98 per $100 of face value of the T-bills and $90 per $100 of face value of the

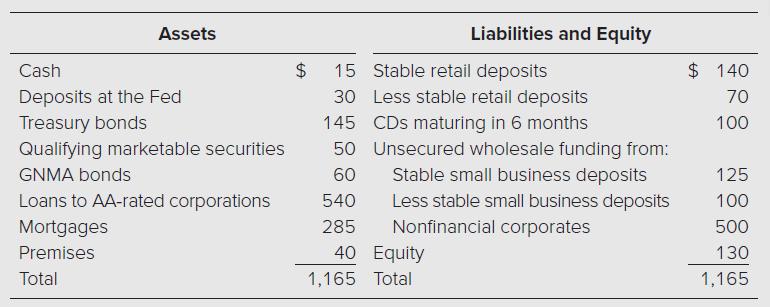

Central Bank has the following balance sheet (in millions of dollars).Cash inflows over the next 30 days from the bank’s performing assets are $7.5 million. Calculate the LCR for Central Bank. Assets Liabilities and Equity Cash $ 15 Stable retail deposits $ 140 Deposits at the Fed 30 Less stable

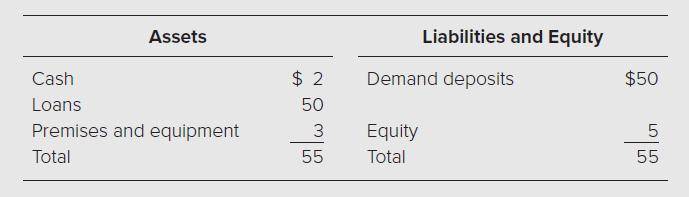

WallsFarther Bank has the following balance sheet (in millions of dollars).Cash inflows over the next 30 days from the bank’s performing assets are $5.5 million. Calculate the LCR for WallsFarther Bank. Assets Liabilities and Equity Cash $ 12 Stable retail deposits $ 55 Deposits at the Fed 19

The following is the balance sheet of a DI (in millions):The asset–liability management committee has estimated that the loans, whose average interest rate is 6 percent and whose average life is three years, will have to be discounted at 10 percent if they are to be sold in less than two days. If

How is the liquidity problem faced by investment funds different from that faced by DIs and insurance companies? How does the liquidity risk of an openend mutual fund compare with that of a closed-end fund?

Go to JPMorgan Chase’s website (www.jpmorganchase.com), download its latest 10Q report and find its sources of liquidity. How have the sources of liquidity changed since June 2021?

What is the difference between a spot and a forward foreign exchange market transaction?

How is the net foreign currency exposure of an FI measured?

If a bank is long in British pounds (£), does it gain or lose if the dollar appreciates in value against the pound?

A bank has £10 million in assets and £7 million in liabilities. It has also bought£52 million in foreign currency trading. What is its net exposure in pounds? (£55 million)

What are the four major FX trading activities?

In which trades do FIs normally act as agents and in which trades as principals?

What is the source of most profits or losses on foreign exchange trading? What foreign currency activities provide a secondary source of revenue?

The cost of one-year U.S. dollar CDs is 8 percent, one-year U.S. dollar loans yield 10 percent, and U.K. pound loans yield 15 percent. The dollar/pound spot exchange rate is $1.50/£1 and the one-year forward exchange rate is $1.48/£1. Are one-year U.S. dollar loans more or less attractive than

What are two ways an FI manager can control FX exposure?

You deposit $10,000 annually into a life insurance fund for the next 10 years, after which time you plan to retire.a. If the deposits are made at the beginning of the year and earn an interest rate of 8 percent, what will be the amount of retirement funds at the end of year 10?b. Instead of a lump

How do life insurance companies earn a profit?

What are the two major activity lines of property–casualty insurance firms?

Insurance companies will charge a higher premium for which of the insurance lines listed below? Why?a. Low-severity, high-frequency lines versus high-severity, low-frequency lines.b. Long-tail lines versus short-tail lines.

An insurance company collected \($3.6\) million in premiums and disbursed\($1.96\) million in losses. Expenses amounted to 6.6 percent and dividends paid to policyholders totaled 1.2 percent. The total income generated from the company’s investments was \($170,000\) after all expenses were paid.

A property–casualty insurer brings in \($6.25\) million in premiums on its homeowners’multiple peril line of insurance. The line’s losses amount to \($4,343,750\), expenses are \($1,593,750\), and dividends are \($156,250\). The insurer earns \($218,750\) on the investment of its premiums.

What have been the major changes in the accounts receivable balances of finance companies over the 44-year period 1977–2021?

Compare Tables 3–2 and 2–5. Which firms have higher ratios of capital to total assets: finance companies or commercial banks? What does this comparison indicate about the relative strengths of these two types of firms?

What are the risk implications to an investment bank from underwriting on a best-efforts basis versus a firm commitment basis? If you operated a company issuing stock for the first time, which type of underwriting would you prefer?Why? What factors might cause you to choose the alternative?

An investment bank agrees to underwrite an issue of 15 million shares of stock for Looney Landscaping Corp.a. If the investment bank underwrites the stock on a firm commitment basis, it agrees to pay $12.50 per share to Looney Landscaping Corp. for the 15 million shares of stock. It can then sell

An investment bank agrees to underwrite a $500 million, 10-year, 8 percent semiannual bond issue for KDO Corporation on a firm commitment basis.The investment bank pays KDO on a Thursday and plans to begin a public sale the next day. What type of interest rate movement does the investment bank fear

One of the major activity areas of securities firms is trading.a. What is the difference between pure arbitrage and risk arbitrage?b. What is the difference between position trading and program trading?

What three factors are given credit for the steady decline in brokerage commissions as a percentage of total revenues over the period beginning in 1977 and ending in 1991?

How did the National Securities Markets Improvement Act (NSMIA) of 1996 change the regulatory structure of the securities industry?

Identify the major regulatory organizations that are involved in the daily operations of the investment securities industry, and explain their role in providing smoothly operating markets.

Showing 4200 - 4300

of 4618

First

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

Step by Step Answers