New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

financial statement analysis

Financial Statement Analysis 10th International Edition John Wild - Solutions

10–2. Working capital equals current assets less current liabilities. Identify and describe factors impairing the usefulness of working capital as an analysis measure.

10–3. Are fixed assets potentially includable in current assets? Explain. If your answer is yes, describe situations where inclusion is possible.

10–4. Certain installment receivables are not collectible within one year. Why are these receivables sometimes included in current assets?

10–5. Are all inventories included in current assets? Why or why not?

10–6. What is the justification for including prepaid expenses in current assets?

10–9. Your analysis of two companies reveals identical levels of working capital. Are you confident in concluding their liquidity positions are equivalent?

10–10. What is the current ratio? What does the current ratio measure? What are reasons for using the current ratio for analysis?

10–11. Since cash generally does not yield a return, why does a company hold cash?

10–12. Is there a relation between level of inventories and sales? Are inventories a function of sales? If there is a relation between inventories and sales, is it proportional?

10–13. What are management’s objectives in determining a company’s investment in inventories and receivables?

10–14. What are the limitations of the current ratio as a measure of liquidity?

10–15. What is the appropriate use of the current ratio as a measure of liquidity?

10–16. What are cash-based ratios of liquidity? What do they measure?

10–17. How can we measure “quality” of current assets?

10–18. What does accounts receivable turnover measure?

10–19. What is the days’ sales in receivables? What does it measure?

10–20. Assume a company’s days’ sales in receivables is 60 days in comparison to 40 days for the prior period.Identify at least three possible reasons for this change.

10–21. What are the repercussions to a company of (a) overinvestment and (b) underinvestment in inventories?

10–22. What problems are expected in an analysis of a company using the LIFO inventory method when costs are increasing? What effects do price changes have on the (a) inventory turnover ratio and (b) current ratio?

10–23. Why is the composition of current liabilities relevant to our analysis of the quality of the current ratio?

10–24. A seemingly successful company can have a poor current ratio. Identify possible reasons for this result.

10–25. What is window-dressing of current assets and liabilities? How can we recognize whether financial statements are window-dressed?

10–26. What is the rule of thumb governing the expected level of the current ratio? What risks are there in using this rule of thumb for analysis?

10–27. Describe the importance of sales in assessing a company’s current financial condition and the liquidity of its current assets.

10–28. Identify important qualitative considerations in the analysis of a company’s liquidity. What SEC disclosures help our analysis in this area?

10–29. What is the importance of what-if analysis on the effects of changes in conditions or policies for a company’s cash resources?

10–30. Identify several key elements in the evaluation of solvency.

10–31. Why is analysis of a company’s capital structure important?

10–32. What is meant by financial leverage? Identify one or more cases where leverage is advantageous.

10–34. How should we treat deferred income taxes in an analysis of capital structure?

10–35. In analysis of capital structure, how should lease obligations not capitalized be treated? Under what conditions should they be considered equivalent to debt?

10–36. What is off-balance-sheet financing? Provide one or more examples.

10–37. What are liabilities for pensions? What factors should our analysis of a company’s pension obligations take into consideration?

10–38. When is information on unconsolidated subsidiaries important to solvency analysis?

10–39. Would you classify the items below as equity or liabilities? State your reason(s) and any assumptions.a. Minority interest in consolidated financial statements.d. Convertible debt.b. Appropriated retained earnings.e. Preferred stock.c. Guarantee for product performance on sale.

10–40.a. Why might an analysis of financial statements need to adjust the book value of assets?b. Give three examples of the need for possible adjustments to book value.

10–41. In evaluating solvency, why are long-term projections necessary in addition to a short-term analysis?What are some limitations of long-term projections?

10–42. What is the difference between common-size analysis and capital structure ratio analysis? Explain how capital structure ratio analysis is useful to financial statement analysis.

10–43. Equity capital on the balance sheet is reported using historical cost accounting and at times differs considerably from market value. How should our analysis allow for this, if at all, in analyzing capital structure?

10–44. Why is the evaluation of asset composition useful for capital structure analysis?

10–45. What does the earnings to fixed charges ratio measure? What does this ratio add to the other tools of credit analysis?

10–46. In computing the earnings to fixed charges ratio, what broad categories of items are included in fixed charges? What tax adjustments must be considered for these items?

10–47. A company you are analyzing has a purchase commitment of raw materials under a noncancelable contract that is substantial in amount. Under what conditions do you include this purchase commitment in computing fixed charges?

10–48. Is net income a reliable measure of cash available to meet fixed charges?

10–50. Comment on the assertion: “Debt is a supplement to, not a substitute for, equity financing.”

10–53. Why are debt securities regularly rated while equity securities are not?

10–54. What factors do rating agencies emphasize in rating an industrial bond? Describe these factors.

10–55. Can an analysis of financial statements improve on published bond ratings? Explain.

10–56. What is the reason(s) why companies hire bond rating agencies to rate their debt?

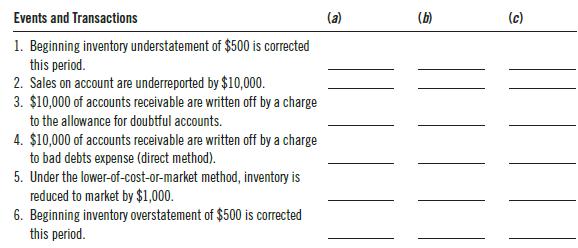

EXERCISE 9–1 Interpret the effect of the following six independent events and transactions for the:a. Accounts receivable turnover (currently equals 3.0).b. Days’ sales in receivables.c. Inventory turnover (currently equals 3.0).The three columns to the right of each event and transaction are

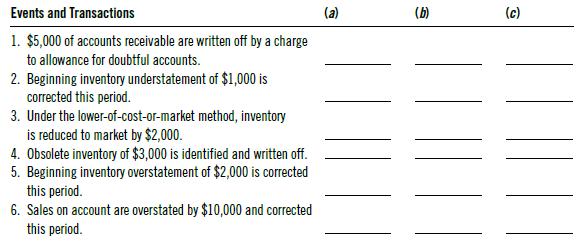

EXERCISE 9–1 Interpret the effect of the following six independent events and transactions for the:a. Accounts receivable turnover (equals 4.0 prior to the event).b. Days’ sales in receivables.c. Inventory turnover (equals 4.0 prior to the event).The three columns to the right of each event and

EXERCISE 9–1 The management of a corporation wishes to improve the appearance of its current financial position as reflected in the current and quick ratios.Required:a. Describe four ways in which management can window-dress the financial statements to accomplish this objective.b. For each

EXERCISE 9–1 Financial data ($ thousands) for Wisconsin Wilderness, Inc., are reproduced below:Short-term liabilities ........ $ 500 Long-term liabilities ......... 800 Equity capital ................... 1,200 Cash from operations ....... 300 Pretax income ................... 200 Interest expense

EXERCISE 9–1 The following information is relevant for Questions 1 and 2:Austin Corporation’s Year 8 financial statement notes include the following information:a. Austin recently entered into operating leases with total future payments of $40 million that equal a discounted present value of

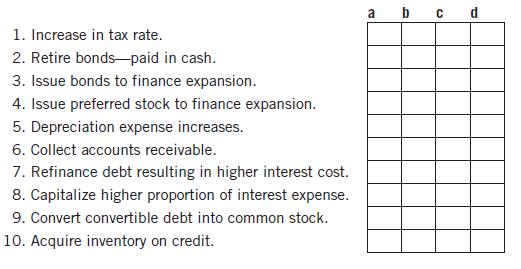

EXERCISE 10–6 1. Among the effects of these adjustments for the times interest earned coverage ratio is (choose one of the following):a. Lease capitalization increases this ratio.b. Lease capitalization decreases this ratio.c. Recognizing the debt guarantee decreases this ratio.d.

EXERCISE 10–6 2. Among the effects of these adjustments for the long-term debt to equity ratio is (choose one of the following):a. Only the held-to-maturity debt securities adjustment decreases this ratio.b. Only lease capitalization decreases this ratio.c. All three adjustments decrease this

EXERCISE 10–6 3. What is the effect of a cash dividend payment on the following ratios (all else equal)?Times Interest Earned Long-Term Debt to Equitya. Increase Increaseb. No effect Increasec. No effect No effectd. Decrease Decrease

EXERCISE 10–6 4. What is the effect of selling inventory for profit on the following ratios (all else equal)?Times Interest Earned Long-Term Debt to Equitya. Increase Increaseb. Increase Decreasec. Decrease Increased. Decrease Decrease

EXERCISE 10–6 5. The existence of uncapitalized operating leases is to (choose one of the following):a. Overstate the earnings to fixed charges coverage ratio.b. Overstate fixed charges.c. Overstate working capital.d. Understate the long-term debt to equity ratio.

EXERCISE 10–6 Selected financial data of Future Technologies, Inc., at December 31, Year 1, are shown below:Cash......................................... $ 42,000 Accounts payable ........$ 78,000 Accounts receivable.................. 90,000 Notes payable.............. 21,000

EXERCISE 10–6 Shown below are selected financial accounts of RAM Corp. as of December 31, Year 1:Cash......................................... $ 80,000 Accounts payable ........ $130,000 Accounts receivable.................. 150,000 Notes payable.............. 35,000

EXERCISE 10–6 Reproduced below are selected financial data at the end of Year 5 and forecasts for the end of Year 6 for Top Corporation:Year 6 Year 6 Account Year 5 (Forecast) Account Year 5 (Forecast)Cash ....................................... $ 35,000 ? Accounts payable ..... $ 65,000 $122,000

PROBLEM 10–6 The income statement of Kimberly Corporation for the year ended December 31, Year 1, is re-produced below:KIMBERLY CORPORATION Consolidated Income Statement ($ thousands)For Year Ended December 31, Year 1

PROBLEM 10–8 The income statement of Lot Corp. for the year ended December 31, Year 1, follows:LOT CORPORATION Income Statement ($ thousands)For Year Ended December 31, Year 1 Sales ........................................................................................ $27,400 Undistributed

PROBLEM 10–6 Your supervisor is considering purchasing the bonds and preferred shares of ARC Corp. She fur- nishes you the following ARC income statement and expresses concern about the coverage of fixed charges.ARC CORPORATION Consolidated Income Statement For Year Ended December 31, Year 5

PROBLEM 10–6 Refer to the following financial data of Fox Industries Ltd.:FOX INDUSTRIES LIMITED Condensed Income Statement ($ thousands)FISCAL YEAR ENDED Year 7 Year 6 Year 5 Year 4 Year 3 Earnings before depreciation, interest on long-term debt, and taxes .............................. $8,750

PROBLEM 10–6 TOPP Company is planning to invest $20,000,000 in an expansion program expected to increase income before interest and taxes by $4,000,000. TOPP currently is earning $5 per share on 2,000,000 shares of common stock outstanding. TOPP’s capital structure prior to the investment

PROBLEM 10–6 You are a senior portfolio manager with Reilly Investment Management reviewing the biweekly printout of equity value screens prepared by a brokerage firm. One of the screens used to identify companies is a “low long-term debt/total long-term capital ratio.” The printout indicates

PROBLEM 10–13 Required:a. Assuming TOPP maintains its current income level and achieves the expected income from expansion, what will be TOPP’s earnings per share:(1) If expansion is financed by debt? (2) If expansion is financed by equity?b. At what level of income before interest and taxes

PROBLEM 10–6 You are analyzing the bonds of ZETA Company (see Case CC–2 in the Comprehensive Case Chapter for data) as a potential long-term investment. As part of your decision-making process, you compute various ratios for Years 5 and 6. Additional data and information to be considered only

PROBLEM 10–6 As a new employee of Clayton Asset Management, you are assigned to evaluate the credit quality of BRT Corp. bonds. Clayton holds the bonds in its high-yield bond portfolio. The following information is provided to assist in the analysis.1. BRT Corporation is a rapidly growing company

PROBLEM 10–16 Assume you are a fixed-income analyst at an investment management firm. You are following the developments at two companies, Sturdy Machines and Patriot Manufacturing, which are both U.S.-based industrial companies that sell their products worldwide. Both companies operate in

PROBLEM 10–6 Fax Corporation’s income statement and balance sheet for the year ended December 31, Year 1, are reproduced below:FAX CORPORATION Income Statement For Year Ended December 31, Year 1 Net sales.......................................................................... $960,000 Cost of

CASE 10–2 Kopp Corporation’s income statement and balance sheet for the year ending December 31, Year 1, are reproduced below:KOPP CORPORATION Income Statement For Year Ended December 31, Year 1 Net sales ....................................................... $ 960,000 Cost of goods sold

CASE 10–2 Ian Manufacturing Company was organized five years ago and manufactures toys. Its most recent three years’ balance sheets and income statements are reproduced below:IAN MANUFACTURING COMPANY Balance Sheets June 30, Year 5, Year 4, and Year 3 Year 5 Year 4 Year 3 Assets Cash

CASE 10–2 Altria Group, formerly known as Philip Morris Companies, is a major manufacturer and distributor of consumer products. It has a history of steady growth in sales, earnings, and cash flows. In recent years Altria has diversified with acquisitions of Miller Brewing and General Foods. In

CASE 10–2 Assume you are an analyst at a brokerage firm. One of the companies you follow is ABEX Chemicals, Inc., which is rapidly growing into a major producer of petrochemicals (principally polyethylene).You are uneasy about competitors in the petrochemical business, their aggressive expansion,

11–1. Why is analysis of research and development expenses important in assessing and forecasting earnings?What are some concerns in analyzing research and development expenses?

11–3. What is the purpose in recasting the income statement for analysis?

11–4. Where do we find the data necessary for analysis of operating results and for their recasting and adjustment?

11–5. Describe the recasting process. What is the aim of the recasting process in analysis?

11–6. Describe the adjustment of the income statement for financial statement analysis.

11–7. Explain earnings management. How is earnings management distinguished from fraudulent reporting?

11–8. Identify and explain at least three types of earnings management.

11–9. What factors and incentives motivate companies (management) to engage in earnings management?What are the implications of these incentives for financial statement analysis?

11–10. Why is management interested in the reporting of extraordinary gains and losses?

11–11. What are the analysis objectives in evaluating extraordinary items?

11–13. Describe the effects of extraordinary items on:a. Company resources.

b. Management evaluation.11–14. Comment on the following statement: “Extraordinary gains or losses do not result from ‘normal’ or‘planned’ business activities and, consequently, they should not be used in evaluating managerial performance.”Do you agree?

11–15. Can accounting manipulations influence earnings-based estimates of company valuation? Explain.

11–16.a. Identify major determinants of PB and PE ratios.b. How can the analyst use jointly the values of PB and PE ratios in assessing the merits of a particular stock investment?

11–17. What is the difference between forecasting and extrapolation of earnings?

11–18. How do MD&A disclosure requirements aid in earnings forecasting?

11–19. What is earning power? Why is earning power important for financial statement analysis?

11–20. How are interim financial statements used in analysis? What accounting problems with interim statements must we be alert to in an analysis?

11–21. Interim financial reports are subject to limitations and distortions. Identify and discuss at least two reasons for this.

11–22. What are major disclosure requirements for interim reports? What are the objectives of these requirements?

11–23. What are the implications of interim reports for financial analysis?

EXERCISE 11–1 Refer to the financial statements of Quaker Oats Company in Problem 9-6 along with the following footnote.SUPPLEMENTARY EXPENSE DATA ($ millions) Year 11 Year 10 Year 9 Advertising, media, and production ............ $ 277.5 $ 282.8 $ 256.5 Merchandising

EXERCISE 11–1 An analyst needs to understand the sources and implications of variability in financial statement data.Required:Identify factors affecting variability in earnings per share, dividends per share, and market price per share that derive froma. The companyb. The economy

Showing 3900 - 4000

of 5656

First

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

Last

Step by Step Answers