New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

fundamental accounting

Fundamentals Of Oil And Gas Accounting 6th Edition Charlotte Wright - Solutions

In project analysis, which method(s) do not permit the ranking of several competing investment options?a. Payback methodb. Accounting rate of returnc. Net present valued. Internal rate of returne. Profitability index

What does the payback method use to rank projects?a. How long the invested money is at riskb. The relative size of the potential profitc. The number of years the well will be producingd. The size of the investment relative to the number of years of anticipated productione. None of these

What is a serious shortcoming of the payback method?a. It is a complicated metric that is difficult to interpret.b. It is based on the time value of money.c. It ignores any cash flows that might occur after payback.d. Discounted cash flows are treated the same as undiscounted cash flows.e. All of

What is a serious shortcoming of the accounting rate of return method?a. It is a complicated metric that is difficult to interpret.b. It does not incorporate the time value of money.c. It ignores any cash flows that might occur after payback.d. Discounted cash flows are treated the same as

The _________ method indicates whether the future cash flow stream generated by an investment will yield a positive net present value when the cash flows are discounted using the company’s desired rate of return.a. IRRb. Paybackc. Profitability indexd. NPVe. None of these

The internal rate of return is the ___________ that would be required in order to generate an NPV of zero.a. Discount rateb. Amount of moneyc. Discounted cash flowd. Profitability indexe. None of these

The IRR method assumes which of the following?a. All future cash inflows will be reinvested at the same rate of return as the IRR.b. None of the future cash inflows will be reinvested at the same rate of return as the IRR.c. All future cash inflows will be reinvested at the same rate as the

The IRR method allows a ranking of competing projects.a. Trueb. False

The ___________ method measures the proportion of the present value of dollars returned to dollars invested.a. IRRb. NPVc. Profitability indexd. Risk-adjusted paybacke. None of these

Define the following terms:asset retirement obligationretirementaccretionpromissory estoppellegally enforceable obligationobligating event

Are the following statements true or false?a. Full cost companies do not book AROs.b. An oral agreement to dismantle equipment and restore the environment at the end of the productive life of a facility would result in the recording of an ARO.c. A change in the discount rate should result in the

When are companies required to remeasure AROs, and what types of changes result in the re-measurement? How are changes recorded?

The CEO of Force Oil Company, Duncan Fife, gave a speech at the World Environmental Conference. In his speech, Mr. Fife spoke about Force Oil’s goal of doing no damage to the environment as a result of the company’s operations and gave specific details on how the company was achieving this

What is a conditional ARO? How are conditional AROs to be accounted for?

Stephens Company operates a single field in Wyoming in which it has a 48%working interest. The remainder of the working interest is held by another oil company. The field went onto production in early in 2022 and has an estimated life of 15 years.REQUIRED: Should Stephens recognize an ARO? If so,

Tadpole Oil and Gas Company completes construction of an offshore oil platform and places it into service on January 1, 2018. Tadpole is legally required to dismantle and remove the platform at the end of its useful life, which is estimated to be 10 years. On January 1, 2018, Tadpole recognized a

Sauer Oil and Gas Company constructed a natural gas treatment facility in three phases. The first phase was completed and placed into service on December 31, 2018. The second phase was completed and placed into service on December 31, 2019, and the third phase was completed and placed into service

When are companies required to remeasure AROs at fair value?a. Annuallyb. When discount rates changec. When events and circumstances indicate that the underlying asset’s carrying value might not be recoverabled. When the end of the asset’s life is readily determinablee. None of these

If the expected cash flow approach is used to estimate the fair value of an ARO, what discount rate should be used?a. Weighted average cost of capitalb. Credit-adjusted risk-free ratec. Incremental borrowing rated. Pretax rate that reflects current market assessment of the time value of money and

Are full cost companies required to book AROs?a. Yes.b. No.c. It depends.

According to ASC 410-20, is an oral agreement between parties a legally enforceable obligation?a. Yes.b. No.c. It depends.

If a contract contains a provision that requires one party to perform retirement activities when the asset is retired, but it is more likely than not that the requirement will be waived, should an ARO be recorded?a. Yes.b. No.c. It depends.

If an ARO is to be remeasured, what discount rate should be used to measure the increment?a. The discount rate used to book the original AROb. The discount rate prevailing when the increment is remeasuredc. The weighted average cost of capital that applies to that particular incrementd. The

Define the following terms:impairmentasset grouptraditional present value approachexpected present value approach

For purposes of booking impairment, what is an asset group? In oil and gas operations, what asset groups are most common?

Give examples of events or circumstances that may trigger impairment testing.

Cameron Oil Company, a successful efforts company, has capitalized costs on Property R, Property S, and Property T as of 12/31/2018 as follows:Cameron has no other capitalized costs. The properties are located in different regions in the United States.REQUIRED: If necessary, test the assets for

Libby Oil Corporation, a successful efforts company, has capitalized costs on three leases as of 12/31/2019 as follows:Libby has no other capitalized costs. The leases are located in different counties in Texas.REQUIRED: If necessary, test the assets for impairment and make any necessary journal

Terry Company, a successful efforts company, has 100% of the working interest in a field in Texas. The field constitutes a cost center and is also an asset group for purposes of testing for impairment. In 2019, the price of oil dropped significantly;therefore, Terry must test for impairment. The

Green Petroleum, a successful efforts company, began operations in 2018 with the acquisition of one field. Green proved the field during 2018. At the end of 2018, prices were high and costs low. During 2019, Green continued exploration and development activities in the field, but towards the end of

Gamma Petroleum owns 100% of the working interest in the Bearcat Field in Wyoming. The field has been producing for 3 years and is expected to produce for 10 more years. Since the state has very stringent decommissioning and environmental statutes, an ARO has been estimated and booked. The local

Gamble Company, a successful efforts company, owns a working interest in an oil field in Alaska. The field has been producing for a number of years and is expected to be producing for another 10 years. On January 1, 2019, the net book value of the field wells, equipment, and facilities totals

When is a company required to test for impairment (according to ASC 360-10-35)?a. Annuallyb. When events or circumstances indicate that the asset’s carrying value may be recoverablec. When events or circumstances indicate that the asset’s book value is higher than its carrying valued. When

According to ASC 360-10-35, how would impairment be determined if an asset requires substantial future development expenditures in order to generate the estimated future cash inflows?a. The future development costs would be estimated and treated as an addition to the net book value of the asset.b.

Why is the temperature of oil or gas important when measuring the volume of oil or gas sold?

Define the following terms:BS&Wgravitytank batteryLACT unitMcfminimum royaltyMMBtu

Define the following terms:run ticketsettlement statementthiefgaugingstrappingHenry HubWest Texas IntermediateNorth Sea Brent BlendDubai crude

Belmont Pipeline Company purchased 200 barrels of oil from Jadson Oil Company. The gross value of the oil was $20,000. The severance tax rate was 4%. Give the entry to record revenue for Jadson, assuming Belmont disbursed the royalty and remitted all taxes, and assuming a division order as follows:

Mr. Stephens sold the surface rights and retained the mineral rights in some land in Texas. He leases the land to George Oil Company, reserving a 1/5 royalty.During 2019, George Oil Company makes the following assignments:a. To Fisher Petroleum, an ORI of 1/7 of George’s interestb. To Wilson

Mountain Oil Company owns a 100% WI in a lease in Wyoming. The lease is burdened with a 1/5 royalty. During the month of July, a total of 10,000 barrels of oil was produced and sold. Assume the selling price of the oil was $90/bbl and the production tax was 5%.REQUIRED: Give the entry required to

During July, Session Oil Company sold 6,000 Mcf of gas at $10.00/Mcf. The lease provides a 1/6 RI. The working interest owner receives 100% of the revenues (net of 5% severance tax) and then distributes the amount due to the royalty interest owner.REQUIRED: Give the entry by Session to record the

McGavin Oil Company obtained 200 Mcf of gas from Lease A and used the gas for gas injection on Lease B. The gas was valued at $12/Mcf. Assume production taxes are 5% and the royalty on Lease A is a 1/6 RI.REQUIRED:a. Give the entry necessary to record the transfer of the gas.b. Give the entry

Wildcat Oil Company sold or used the gas produced on Lease A during March as follows:a. 600 Mcf used as fuel to operate lease equipmentb. 800 Mcf sold to R Company at $12/Mcf Assume a 1/7 RI and a production tax of 5%, and assume that the lease agreement has a free fuel clause, but production taxes

Libby Oil Company has a working interest in a remote lease located in Wyoming.Libby agreed to pay the royalty owner a minimum royalty of $500/month in addition to the 1/5 royalty. Gas production on the lease began in the third month after the lease contract was signed. Total sales revenue during

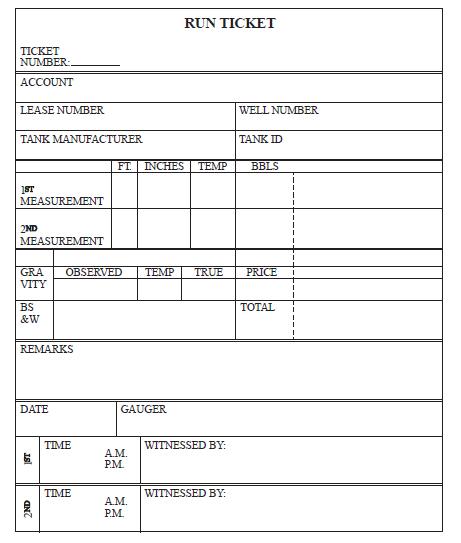

Complete the accompanying run ticket and give the entry to record the sale of the oil at $75/bbl assuming a severance tax rate of 5% and a 1/5 RI. The operator is Montgomery Oil Company and the run ticket is number 55. Use the tables given in the chapter. The tank is manufactured by Tank-Co and its

Information from a run ticket shows that 2,000 net barrels of oil with an API gravity of 36º were sold. The selling price is based on a contract price of $90/bbl, adjusted downward 4¢ for each degree of gravity less than 40º.REQUIRED: Compute the selling price for the 2,000 barrels.

Structure Oil Company made the following transactions in 2021:a. During the months of January through March, minimum royalty payments of$500/month were paid. The minimum royalty payments are recoverable from future royalty payments.b. Production was sold in April 2021, and the royalty payable in

Garcia Company has a 100% WI in a lease in a remote area of Wyoming. The lease provides for a 1/5 royalty. Garcia produces and sells a total of 150,000 Mcf of gas from the property during August. Of the 150,000 Mcf of gas, 50,000 Mcf are sold to a pipeline for $10.00/Mcf. Garcia sells the remaining

Determine the barrels of production allocated to each well given the following data:Round the ratio to three decimal places and round barrels to the nearest whole barrel. Well 24-hr Test, bbl 40 50 35 123 Days Produced 28 30 24 Total Production Sold 3,300 barrels measured at point of delivery

Bryant Oil Company produced a total of 1,000 barrels of oil in June 2022. The expected selling price was $120/bbl. The purchaser pays the severance taxes and the royalty interest owner and remits the remainder to Bryant Oil. The royalty interest is 1/5, and the severance tax rate is 10%.REQUIRED:a.

Launch Oil Company owns a working interest in the Carpenter Lease in Texas.The lease is burdened with a 3/16 royalty interest. During April, a total of 4,000 barrels of oil is sold at $90/bbl to a refinery owned 100% by Launch Oil. Assume the severance tax rate is 5% in Texas.REQUIRED: Prepare

Michael Oil Company operates Leases X and Y. Michael Oil transfers 60 barrels of oil from Lease X to Lease Y to be used as fuel on Lease Y. The current spot oil price is $110/bbl, and the severance tax rate is 5%. Michael owns 100% working interests in Lease X and Lease Y. Lease X has a 1/8 royalty

A lease operated by Rocky Oil Company produces a total of 3,000 barrels of oil in June. The oil is sold in October. The posted field price and the actual selling price is $100/bbl. The severance tax rate is 5%. The purchaser of the oil will pay the severance tax to the state and also will pay the

Pam O’Neal owns some mineral rights in Oklahoma that she leases to Sunshine Oil Company, reserving a 1/8 royalty interest. During 2021, Sunshine Oil made the following assignments:a. To Ted Mair, an ORI of 1/6b. To Frank Clark, a production payment interest of 15,000 barrels of oil to be paid out

Kincaid Oil Company sells 20,000 (gross) Mcf of gas at $9/Mcf. The lease is burdened with a 1/6 RI, and the working interest owner has assigned an ORI of 1/10. The severance tax rate is 7%.REQUIRED: Record the entries for the royalty interest owner, ORI owner, and working interest owner,

Jackson Oil Company’s production for Lease A and Lease B is gathered into a common system and sold. Total sales for the month of July are 6,562 barrels.Assume the following data for Lease A and Lease B:Measured production is 3,300 barrels from Lease A and 3,500 barrels from Lease B.REQUIRED:a.

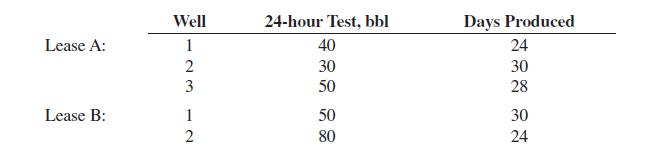

Hill Company’s production from each well on Lease C and Lease D is estimated based on a 24-hour test. Oil produced from each well on each lease is commingled and measured before leaving each lease. The oil produced from each lease is then commingled and delivered to a central tank battery.Assume

Longhorn Company (70% WI) and Aggie Company (30% WI) own a joint working interest in the Dowling Field. There is a 1/8 royalty owner. The 1/8 royalty is shared proportionally by Longhorn and Aggie. Longhorn and Aggie agree that Longhorn’s purchaser will take March’s gas production and Aggie’s

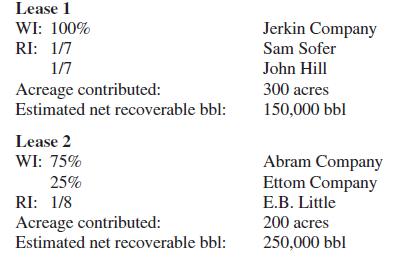

Two leases in far West Texas are being combined to form the West End Unit.REQUIRED:a. Determine the participation factors for each party, assuming the participation factors are based on the acreage contributed.b. Determine the participation factors for each party, assuming the participation factors

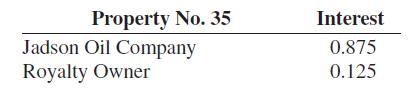

Heagy Oil Company has production on a lease in Louisiana with the following ownership interest:During April, 5,000 (gross) barrels of oil (after correction for temperature, gravity, and BS&W) were produced and sold. Assume the price for oil is $120.00/bbl, and the severance tax rate in

Higgins Company, a full cost company located in Texas, sold 3,000 (gross) Mcf of gas with a heat content of 1.035 MMBtu/Mcf. The selling price of the gas was$9.00/MMBtu.REQUIRED:a. Determine the MMBtus for the gas sold.b. Determine the total sales price.c. Determine the unit sales price per Mcf.

Tharp Field is jointly owned by Gavin Company (70% WI), which acts as field operator, and Garza Company (30% WI). There is a 1/6 royalty. The 1/6 royalty is shared proportionally by Gavin and Garza. The two working interest owners have agreed that Gavin’s purchaser will take gas produced in July,

Hays Oil Company is a new successful efforts company located in New Mexico.During September 2020, Hays Oil Company sold 2,000 Mcf of gas at 14.65 psia with a heat content of 1.030 MMBtu/Mcf at 14.73 psia. The selling price of the gas was $8.80/MMBtu.REQUIRED:a. Convert Mcf to a standard pressure of

Sam Field, located in northern Alaska, is jointly owned by Smith Company (60%WI) and Joyner Company (40% WI). Smith, which is the operator, estimates that gross gas production during July will be 40,000 Mcf. Smith Company makes confirmed nominations of 30,000 Mcf, and Joyner Company makes confirmed

____________ is natural gas that overlies and is in contact with crude oil in a reservoir but is not in solution with the oil.a. Nonassociated gasb. Associated gasc. Nondissolved gasd. Gas well gase. None of these

__________________ involves buying or selling one shipment of oil under a price that is agreed upon at the time of the arrangement.a. Posted priceb. Spot pricec. Future priced. WTI pricee. None of these

No royalty is typically paid on _______________.a. Lease use gasb. Off-lease use gasc. Crude oil exchangesd. Non-processed gase. None of these

Under the _______________ method of accounting for production imbalances, no receivable or payable is recorded for under-derlivered or overdelivered oil or gas.a. Entitlementsb. Salesc. Imbalancesd. Working intereste. None of these

MMBTU is a measure of ____________.a. Volumeb. Energyc. Weightd. Gravitye. None of these

The price at ____________ is typically used as the price benchmark for spot trades of natural gas.a. WTIb. US Gulf Coastc. Rotterdam/Northwest Europed. Henry Hube. None of these

Define the following:a. IDCb. Elected capitalized IDCc. Subleased. Depletable basise. Half-year conventionf. Property

How does the formula for tax depletion differ from the formula for successful efforts or full cost depletion?

How does the tax depletion of leasehold costs differ from successful efforts or full cost depletion? Include in your answer a discussion of the reserves used (proved reserves or proved developed reserves), which costs are amortized, and the cost center used (i.e., are property costs amortized

How does amortization of lease and well equipment such as storage tanks and separators differ under the three methods? Include in your answer a discussion of the method used, including which reserves are used, if any, and the cost center used.

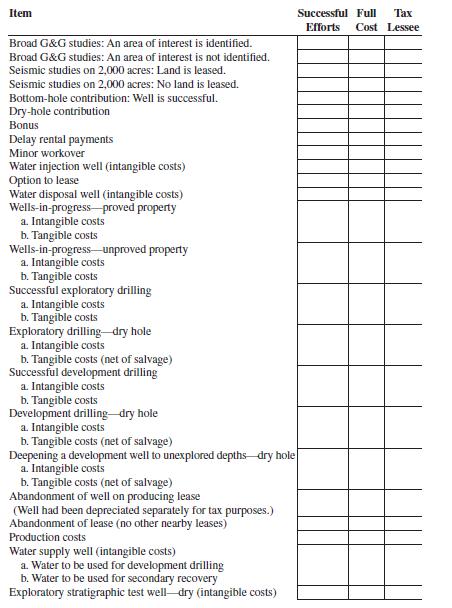

Indicate which items are to be capitalized (C), expensed (E), or part capitalized and part expensed (C/E) for successful efforts, full cost, and tax accounting.Assume the maximum tax deductions are taken. Item Broad G&G studies: An area of interest is identified. Broad G&G studies: An area of

How does amortization of drilling costs differ under the three methods? Include in your answer a discussion of the method used, which reserves are used, if any, and which drilling costs are amortized—dry versus successful, exploratory well versus development well, completed versus uncompleted,

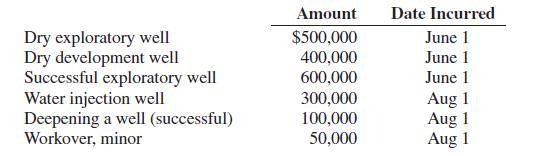

Belmont Oil Company, a full cost company, incurred intangible costs during 20XA related to the following:REQUIRED:a. Assuming Belmont is an independent producer, how much IDC can it deduct for 20XA?b. How much IDC could Belmont deduct as an integrated producer? Dry exploratory well Dry development

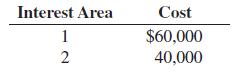

During early 20XA, Terry Petroleum incurred G&G costs of $45,000 for Project Area

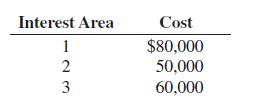

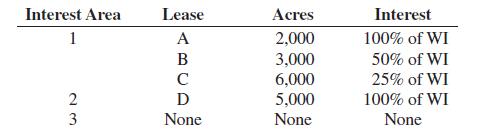

As a result of the G&G, three areas of interest were identified. Detailed G&G was conducted on the areas of interest at the following costs:As a result of the detailed G&G studies, the following leases were acquired:REQUIRED: Determine the tax basis of any assets and the amount of any

On January 1, 20XA, Granger Oil Corporation bought a developed lease for$300,000. During 20XA, Granger Oil Corporation incurred $600,000 of IDC on a successful well. Reserves of 400,000 barrels were discovered, and 20,000 barrels were produced and sold. Gross income from production was

Hoffman Oil Corporation paid the following amounts in 20XD:REQUIRED: Determine the tax basis of any assets and the amount of any tax deductions. Shut-in royalty payments (not recoverable) $5,000 Shut-in royalty payments (failure to make payments terminates lease).. 4,000 Shut-in royalty payments

During 20XA, Black Petroleum incurred G&G costs of $20,000 for Project Area15. Two areas of interest were identified. Detailed seismic studies were conducted on the areas of interests at the following costs:As a result of the detailed seismic studies, the following leases were obtained:During

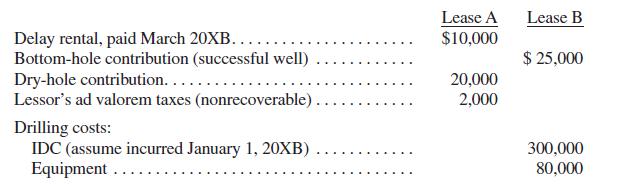

On March 1, 20XA, Bryce Mott purchases mineral rights (MR) for $80,000. On June 1, 20XA, he leases the mineral rights to Hampton Oil Company, retaining a 1/8 royalty interest (RI). Hampton Oil Company pays Mott a lease bonus of$5,000. On June 1, 20XB, a delay rental of $1,000 is received by Mott.

Aztec Oil Company, an integrated producer, has an unproved property with acquisition and capitalized G&G costs of $35,000. Aztec also has a proved property with the following costs:REQUIRED: Determine the amount of the tax loss in each of the following situations:a. Aztec drilled a dry hole on

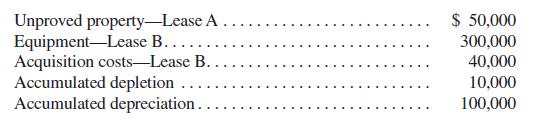

Scott Oil Company, an independent producer, has the following account balances at 1/1/20XA:REQUIRED: Determine the amount of the tax loss on the following dates:a. On March 1, 20XA, the unproved property is abandoned.b. On April 2, 20XA, Lease B is abandoned with salvageable equipment in the amount

Thomas Petroleum has the following information:The lease is subleased to Stevenson Oil Corporation for $300,000, and Thomas retains an 1/16 ORI. At the date of the sublease, the FMV of the equipment is $180,000.REQUIRED: Determine the tax basis of Thomas’ and Stevenson’s assets and the amount

Graham Oil Corporation, an integrated producer, incurs IDC costs in the following years as indicated. The IDC amounts marked with an asterisk (*) relate to dry-hole IDC.REQUIRED: Compute the amount that may be deducted for IDC in the years 20XA, 20XB, 20XC, and 20XD. Date Date Date Date Incurred

During 20XB, Chatham Oil and Gas Company incurs the following costs relating to Lease A, a producing property:REQUIRED: Determine the tax basis of any assets and the amount of any tax deductions. Supplies for Lease A... Labor cost for pumpers and gaugers-Lease A Ad valorem tax on Lease A.....

Colley Energy, an independent producer, has average production from Lease A of 100 bbl/day in 20XA from Lease A. The average selling price of oil in 20XA is$120/bbl. Net income from Lease A in 20XA is $820,000, and taxable income of the company is $2,000,000.REQUIRED: Compute percentage depletion.

Laredo Oil Corporation began operations in June 20XA. Laredo Oil is classified as an independent producer. During the first 2½ years of operation, Laredo Oil acquired only two US properties, which were noncontiguous. Costs incurred on those properties during those 2½ years are given below, net of

Kilpatrick Oil Corporation owns and operates four oil and gas properties that are classified for tax purposes as four separate properties. Data for the four properties are presented below:REQUIRED: Compute the amount of percentage depletion that could be deducted on Kilpatrick’s tax return.

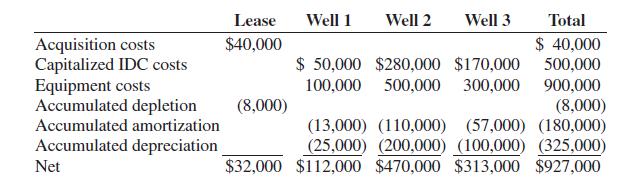

Lexington Energy owns only one lease in the United States, Lease Q. The following information for Lease Q, which is burdened with a 1/6 royalty, is as of 12/31/20XD.All reserve, production, and sales data apply only to Lexington Energy.Additional data: Lexington also placed in service on 8/1/20XB a

If interest areas warranting further evaluation are identified, the initial reconnaissance costs of the project area are ______________.a. Capitalized to the areas of interestb. Allocated to the areas of interest on an acre-by-acre basisc. Allocated equally to the areas of interest regardless of

After an area of interest is identified, any costs incurred to further evaluate it are__________.a. Capitalized to the area of interestb. Allocated to the areas of interest on an acre-by-acre basisc. Allocated equally to the areas of interest regardless of their relative sizesd. Held in suspense

All of the following costs would be classified as IDC EXCEPT __________.a. Labor to install valves and pipe in the tank batteryb. Labor to install the wellheadc. Labor to cement surface casingd. Labor to build the locatione. None of these

All of the following cost would be classified as lease and well equipment EXCEPT _________.a. Dirt-moving necessary for location of a tank batteryb. Reentering a producing well for the purpose of perforating in a new zone or horizonc. Labor to install a Christmas treed. Labor to install flow

According to the IRS, what reserves are to be used in computing cost depletion?a. Proved onlyb. Probable onlyc. Possible or perspective onlyd. All of thesee. None of these

What is the term describing two tracts of land that share only a corner?a. Adjacentb. Contiguousc. Annexedd. Indexede. None of these

Which of the following statements is NOT true regarding the election to expense IDC?a. Integrated oil companies are required to capitalize70% of IDC even after making the election.b. The amount capitalized by an integrated oil company is deducted ratably over 60 months.c. The election is binding on

For a lessee, losses from unproductive properties may NOT be taken in which of the following situations?a. Losses are not taken for drilling development dry holes.b. Losses are not taken for abandonment of unproved property.c. Losses are not taken for abandonment of leasehold and wells and

Showing 1700 - 1800

of 2510

First

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

Last

Step by Step Answers