New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

intermediate accounting

Intermediate Accounting 10th edition J. David Spiceland, James Sepe, Mark Nelson, Wayne Thomas - Solutions

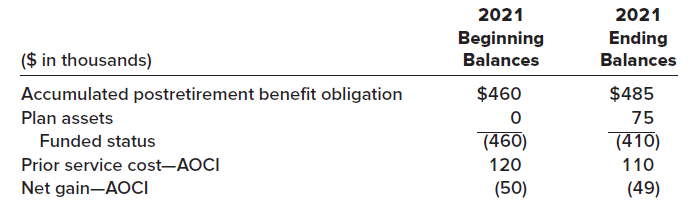

The information below pertains to the retiree health care plan of Thompson Technologies:Thompson began funding the plan in 2021 with a contribution of $127,000 to the benefit fund at the end of the year. Retirees were paid $52,000. The actuary?s discount rate is 5%. There were no changes in

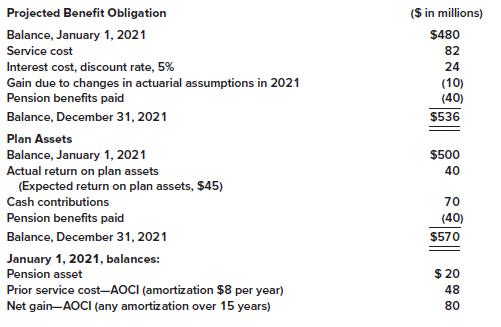

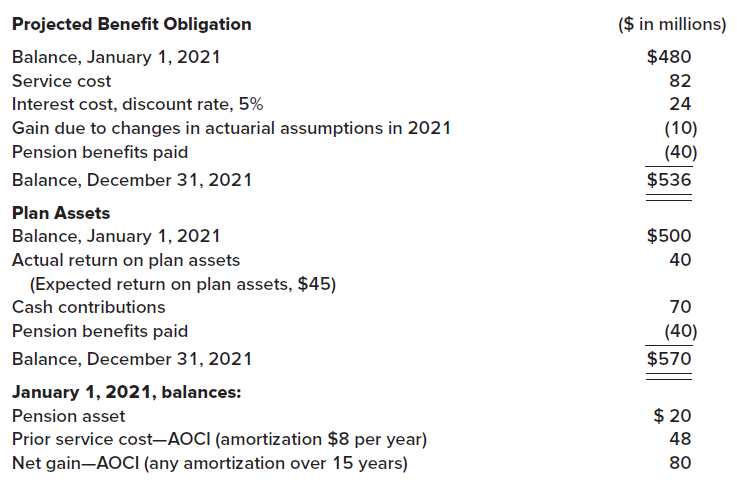

Refer to the data provided in E 17–19.Required:Prepare a pension spreadsheet to show the relationship among the PBO, plan assets, prior service cost, the net gain, pension expense, and the net pension asset.E 17–19 Projected Benefit Obligation ($ in millions) Balance, January 1, 2021 $480

Stockton Labeling Company has a retiree health care plan. Employees become fully eligible for benefits after working for the company eight years. Stockton hired Misty Newburn on January 1, 2021. As of the end of 2021, the actuary estimates the total net cost of providing health care benefits to

Beale Management has a noncontributory, defined benefit pension plan. On December 31, 2021 (the end of Beale?s fiscal year), the following pension-related data were available: Required:1. Prepare the 2021 journal entry to record pension expense.2. Prepare the journal entry(s) to record any 2021

Patel Industries has a noncontributory, defined benefit pension plan. Since the inception of the plan, the actuary has used as the discount rate the rate on high-quality corporate bonds, which recently has been 7%. During 2021, changing economic conditions caused the rate to change to 6%, and the

Actuary and trustee reports indicate the following changes in the PBO and plan assets of Douglas-Roberts Industries during 2021: Prior service cost at Jan. 1, 2021, from plan amendment at the beginning of 2018 (amortization: $4 million per year) $28 million Net loss?AOCI at Jan. 1, 2021 (previous

On January 1, 2021, Medical Transport Company’s accumulated postretirement benefit obligation was $25 million. At the end of 2021, retiree benefits paid were $3 million. Service cost for 2021 is $7 million. Assumptions regarding the trend of future health care costs were revised at the end of

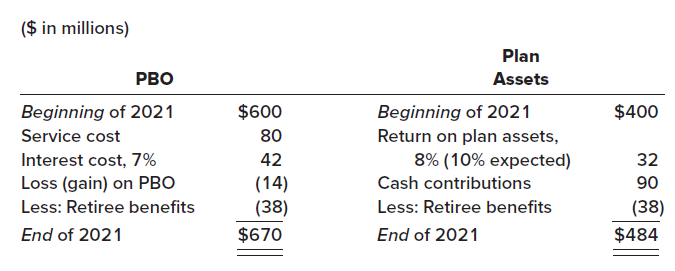

The following pension-related data pertain to Metro Recreation?s noncontributory, defined benefit pension plan for 2021 ($ in thousands): Required:Prepare a pension spreadsheet that shows the relationships among the various pension balances, shows the changes in those balances, and computes

Prince Distribution Inc., has an unfunded postretirement benefit plan. Medical care and life insurance benefits are provided to employees who render 10 years service and attain age 55 while in service. At the end of 2021, Jim Lukawitz is 31. He was hired by Prince at age 25 (6 years ago) and is

Lewis Industries adopted a defined benefit pension plan on January 1, 2021. By making the provisions of the plan retroactive to prior years, Lewis incurred a prior service cost of $2 million. The prior service cost was funded immediately by a $2 million cash payment to the fund trustee on January

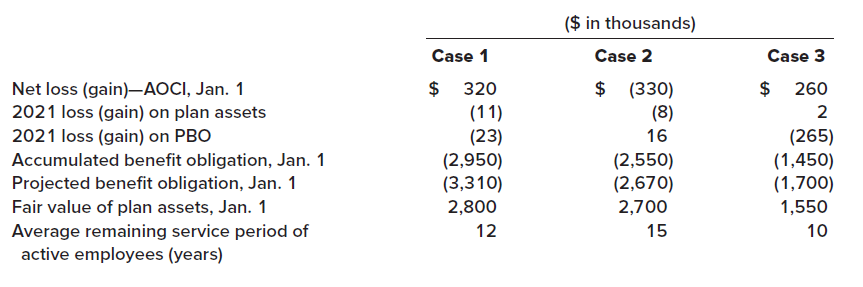

Hicks Cable Company has a defined benefit pension plan. Three alternative possibilities for pension-related data at January 1, 2021, are shown below: Required:1. For each independent case, calculate any amortization of the net loss or gain that should be included as a component of pension expense

Refer to the situation described in P 17–10. Assume Electronic Distribution prepares its financial statements according to International Financial Reporting Standards (IFRS). Also assume that 10% is the current interest rate on high-quality corporate bonds.Required:1. Calculate the net pension

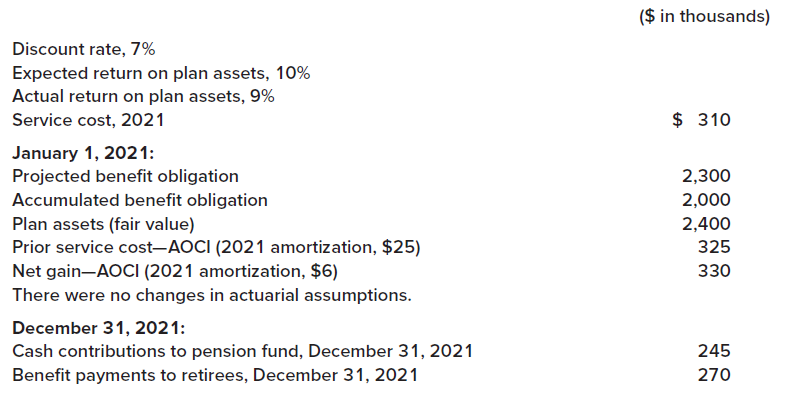

Pension data for Barry Financial Services Inc., include the following: Required:1. Determine pension expense for 2021.2. Prepare the journal entries to record? (a) Pension expense (b) Gains and losses (if any) (c) Funding, (d) Retiree benefits for 2021. ($ in thousands) Discount rate, 7% Expected

Electronic Distribution has a defined benefit pension plan. Characteristics of the plan during 2021 are as follows:.............................................................($ in millions)PBO balance, January 1 ...............................$480Plan assets balance, January

U.S. Metallurgical Inc., reported the following balances in its financial statements and disclosure notes at December 31, 2020.Plan assets ......................................$400,000Projected benefit obligation ...........320,000U.S.M.’s actuary determined that 2021 service cost is $60,000.

Refer to the situation described in E 17–8.Required:How might your answer differ if we assume Sterling Properties prepares its financial statements according to International Financial Reporting Standards (IFRS)? The interest rate on high-grade corporate bonds is 6%.E

JDS Shipyard’s projected benefit obligation, accumulated benefit obligation, and plan assets were $40 million, $30 million, and $25 million, respectively, at the end of the year. What, if any, pension liability must be reported in the balance sheet? What would JDS report if the plan assets were

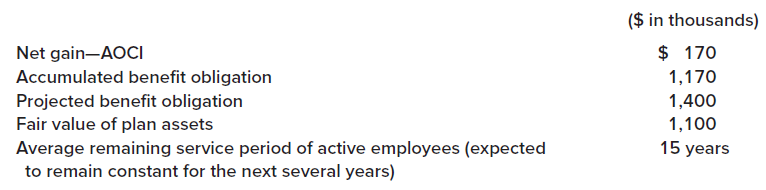

Pension data for Sterling Properties include the following:...................................................................($ in thousands)Service cost, 2021 ......................................................$112Projected benefit obligation, January 1, 2021 ..........850Plan assets (fair

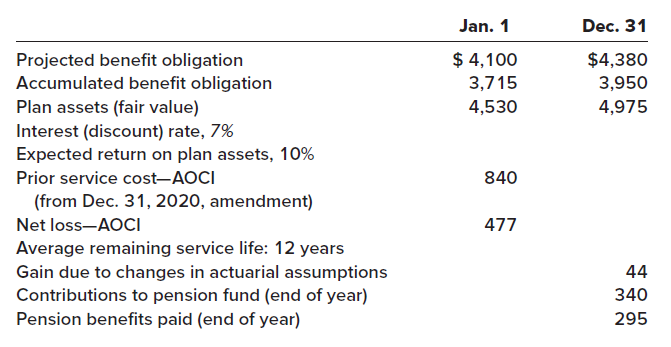

Herring Wholesale Company has a defined benefit pension plan. On January 1, 2021, the following pensionrelated data were available: The rate of return on plan assets during 2021 was 9%, although it was expected to be 10%. The actuary revised assumptions regarding the PBO at the end of the year,

Stanley-Morgan Industries adopted a defined benefit pension plan on April 12, 2021. The provisions of the plan were not made retroactive to prior years. A local bank, engaged as trustee for the plan assets, expects plan assets to earn a 10% rate of return. A consulting firm, engaged as actuary,

Sachs Brands’s defined benefit pension plan specifies annual retirement benefits equal to 1.6% × service years × final year’s salary, payable at the end of each year. Angela Davenport was hired by Sachs at the beginning of 2007 and is expected to retire at the end of 2041 after 35 years’

Sachs Brands’s defined benefit pension plan specifies annual retirement benefits equal to 1.6% × service years × final year’s salary, payable at the end of each year. Angela Davenport was hired by Sachs at the beginning of 2007 and is expected to retire at the end of 2041 after 35 years’

Sachs Brands’s defined benefit pension plan specifies annual retirement benefits equal to 1.6% × service years × final year’s salary, payable at the end of each year. Angela Davenport was hired by Sachs at the beginning of 2007 and is expected to retire at the end of 2041 after 35 years’

Sachs Brands’s defined benefit pension plan specifies annual retirement benefits equal to 1.6% × service years × final year’s salary, payable at the end of each year. Angela Davenport was hired by Sachs at the beginning of 2007 and is expected to retire at the end of 2041 after 35 years’

On January 1, 2021, Ravetch Corporation’s projected benefit obligation was $30 million. During 2021, pension benefits paid by the trustee were $4 million. Service cost for 2021 is $12 million. Pension plan assets (at fair value) increased during 2021 by $6 million as expected. At the end of 2021,

Sachs Brands’s defined benefit pension plan specifies annual retirement benefits equal to 1.6% × service years × final year’s salary, payable at the end of each year. Angela Davenport was hired by Sachs at the beginning of 2007 and is expected to retire at the end of 2041 after 35 years’

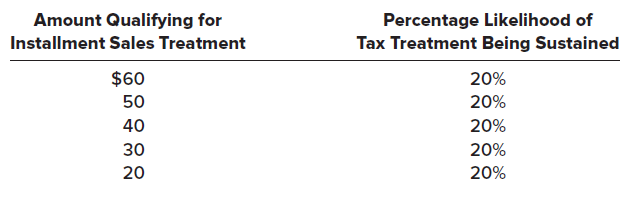

First Bank has some questions as to the tax-free nature of $5 million of governmental bonds held in its investment portfolio. This amount is excluded from First Bank’s taxable income of $55 million. Management has determined that there is a 65% chance that the tax-free status of this entire

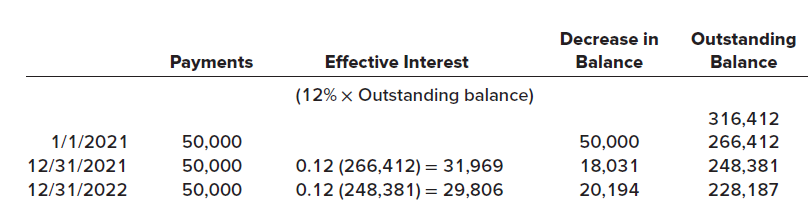

On January 1, 2021, NRC Credit Corporation leased equipment to Brand Services under a finance/sales-type lease designed to earn NRC a 12% rate of return for providing long-term financing. The lease agreement specified the following:a. Ten annual payments of $55,000 beginning January 1, 2021, the

Federated Fabrications leased a tooling machine on January 1, 2021, for a three-year period ending December 31, 2023. The lease agreement specified annual payments of $36,000 beginning with the first payment at the beginning of the lease, and each December 31 through 2022. The company had the

Rhone-Metro Industries manufactures equipment that is sold or leased. On December 31, 2021, Rhone-Metro leased equipment to Western Soya Co. for a noncancelable stated lease term of four years ending December 31, 2025, at which time possession of the leased asset will revert back to Rhone-Metro.

(This problem is a variation of P 15?19, modified to cause the lease to be a sales-type lease with a selling profit.)Bidwell Leasing purchased a single-engine plane for $400,000 and leased it to Red Baron Flying Club for its fair value of $645,526 on January 1, 2021.Terms of the lease agreement and

On January 1, 2021, Wetick Optometrists leased diagnostic equipment from Southern Corp., which had purchased the equipment at a cost of $1,437,237. The lease agreement specifies six annual payments of $300,000 beginning January 1, 2021, the beginning of the lease, and at each December 31 thereafter

Bidwell Leasing purchased a single-engine plane for its fair value of $645,526 and leased it to Red Baron Flying Club on January 1, 2021.Terms of the lease agreement and related facts werea. Eight annual payments of $110,000 beginning January 1, 2021, the beginning of the lease, and at each

Branif Leasing leases mechanical equipment to industrial consumers under sales-type leases that earn Branif a 10% rate of return for providing long-term financing. A lease agreement with Branson Construction specified 20 annual payments beginning December 31, 2021, the beginning of the lease. The

On January 1, 2021, Lesco Leasing leased equipment to Quality Services under a finance/sales-type lease designed to earn NRC a 12% rate of return for providing long-term financing. The lease agreement specified a. Ten annual payments of $56,000 beginning January 1, 2021, the beginning of the lease

Newton Labs leased chronometers from Brookline Instruments on January 1, 2021. Brookline Instruments manufactured the chronometers at a cost of $200,000. The chronometers have a fair value of $260,000.Appropriate adjusting entries are made quarterly. Required:1. Prepare appropriate entries for

High Time Tours leased rock-climbing equipment from Adventures Leasing on January 1, 2021. High Time has the option to renew the lease at the end of two years for an additional three years for $8,000 per quarter.? Adventures purchased the equipment at a cost of $198,375. Required:1. Prepare

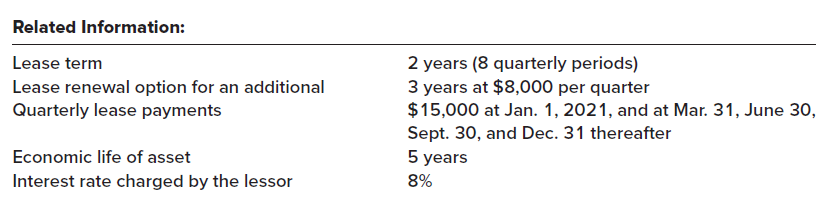

Manufacturers Southern leased high-tech electronic equipment from Edison Leasing on January 1, 2021. Edison purchased the equipment from International Machines at a cost of $112,080.Related Information:Lease term .........................................2 years (8 quarterly periods)Quarterly rental

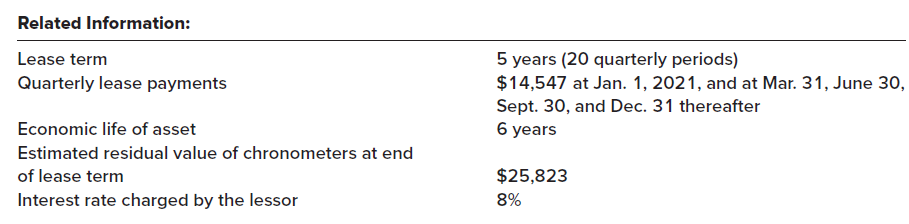

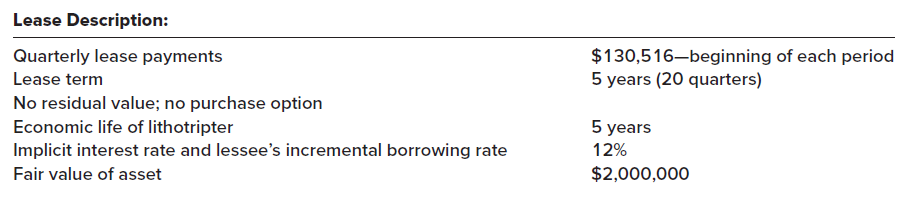

Rand Medical manufactures lithotripters. Lithotripsy uses shock waves instead of surgery to eliminate kidney stones. Physicians? Leasing purchased a lithotripter from Rand for $2,000,000 and leased it to Mid-South Urologists Group, Inc., on January 1, 2021. 1. How should this lease be classified

On June 30, 2021, Georgia-Atlantic, Inc. leased warehouse equipment from Builders, Inc. The lease agreement calls for Georgia-Atlantic to make semiannual lease payments of $562,907 over a three-year lease term (also the asset’s useful life), payable each June 30 and December 31, with the first

On June 30, 2021, Georgia-Atlantic, Inc. leased warehouse equipment from IC Leasing Corporation. The lease agreement calls for Georgia-Atlantic to make semiannual lease payments of $562,907 over a three-year lease term (also the asset’s useful life), payable each June 30 and December 31, with the

On June 30, 2021, Georgia-Atlantic, Inc. leased warehouse equipment from IC Leasing Corporation. The lease agreement calls for Georgia-Atlantic to make semiannual lease payments of $562,907 over a three-year lease term, payable each June 30 and December 31, with the first payment at June 30, 2021.

On April 1, 2021, Western Communications, Inc., issued 12% bonds, dated March 1, 2021, with face amount of $30 million. The bonds sold for $29.3 million and mature on February 28, 2024. Interest is paid semiannually on August 31 and February 28. Stillworth Corporation acquired $30,000 of the bonds

Interstate Automobiles Corporation leased 40 vans to VIP Transport under a four-year noncancelable lease on January 1, 2021. Information concerning the lease and the vans follows:a. Equal annual lease payments of $300,000 are due on January 1, 2021, and thereafter on December 31 each year. The

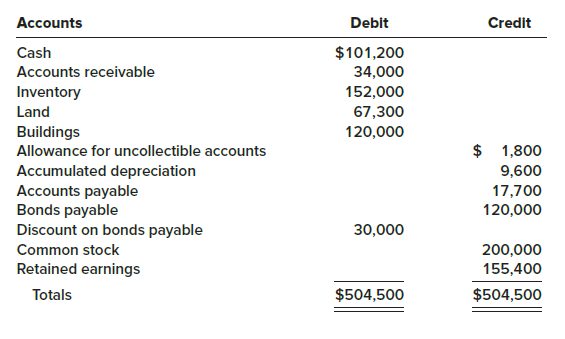

On January 1, 2021, the general ledger of Freedom Fireworks includes the following account balances: During January 2021, the following transactions occurred:January 1 Borrowed $100,000 from Captive Credit Corporation. The installment note bears interest at 7% annually and matures in 5 years.

On March 1, 2021, Brown-Ferring Corporation issued $100 million of 12% bonds, dated January 1, 2021, for $99 million (plus accrued interest). The bonds mature on December 31, 2040, and pay interest semiannually on June 30 and December 31. Brown-Ferring’s fiscal period is the calendar

(Note: This is a variation of E 14–13 modified to consider the fair value option for reporting liabilities.) Federal Semiconductors issued 11% bonds, dated January 1, with a face amount of $800 million on January 1, 2021. The bonds sold for $739,814,813 and mature on December 31, 2040 (20 years).

On January 1, 2021, Madison Products issued $40 million of 6%, 10-year convertible bonds at a net price of $40.8 million. Madison recently issued similar, but nonconvertible, bonds at 99 (that is, 99% of face amount). The bonds pay interest on June 30 and December 31. Each $1,000 bond is

At the end of 2020, Majors Furniture Company failed to accrue $61,000 of interest expense that accrued during the last five months of 2020 on bonds payable. The bonds mature in 2034. The discount on the bonds is amortized by the straight-line method. The following entry was recorded on February 1,

On February 1, 2021, Strauss-Lombardi issued 9% bonds, dated February 1, with a face amount of $800,000. The bonds sold for $731,364 and mature on January 31, 2041 (20 years). The market yield for bonds of similar risk and maturity was 10%. Interest is paid semiannually on July 31 and January 31.

The fiscal year ends December 31 for Lake Hamilton Development. To provide funding for its Moonlight Bay project, LHD issued 5% bonds with a face amount of $500,000 on November 1, 2021. The bonds sold for $442,215, a price to yield the market rate of 6%. The bonds mature October 31, 2041 (20

EDGAR, the Electronic Data Gathering. Analysis, and Retrieval system, performs automated collection, validation, indexing, acceptance and forwarding of submissions by companies and others who are required by law to file forms with the U.S. Securities and Exchange Commission (SEC). All publicly

On February 1, 2021, Cromley Motor Products issued 9% bonds, dated February 1, with a face amount of $80 million. The bonds mature on January 31, 2025 (4 years). The market yield for bonds of similar risk and maturity was 10%. Interest is paid semiannually on July 31 and January 31. Barnwell

On January 1, 2021, Instaform, Inc., issued 10% bonds with a face amount of $50 million, dated January 1. The bonds mature in 2040 (20 years). The market yield for bonds of similar risk and maturity is 12%. Interest is paid semiannually.Required:1. Determine the price of the bonds at January 1,

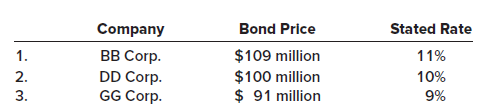

Your investment department has researched possible investments in corporate debt securities. Among the available investments are the following $100 million bond issues, each dated January 1, 2021. Prices were determined by underwriters at different times during the last few weeks. Each of the bond

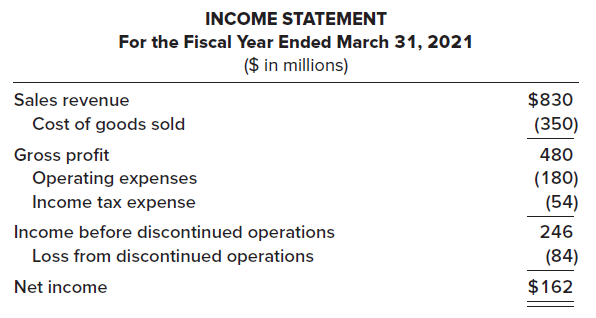

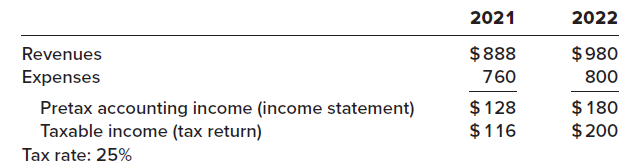

The following income statement does not reflect intraperiod tax allocation. Required:Recast the income statement to reflect intraperiod tax allocation. The company?s tax rate is 25%. INCOME STATEMENT For the Fiscal Year Ended March 31, 2021 ($ in millions) $830 Sales revenue (350) Cost of goods

As of December 31, 2021, Lange Company has the following deferred tax assets and liabilities:Deferred tax assetsPension plans ..............................$ 300,000Inventory ..........................................200,000Total deferred tax assets ...............500,000Deferred tax

(This exercise is a variation of E 16?28, modified to include a second temporary difference.)Case Development began operations in December 2021. When property is sold on an installment basis, Case recognizes installment income for financial reporting purposes in the year of the sale. For tax

Case Development began operations in December 2021. When property is sold on an installment basis, Caserecognizes installment income for financial reporting purposes in the year of the sale. For tax purposes, installmentincome is reported by the installment method. 2021 installment income was

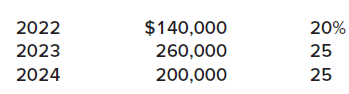

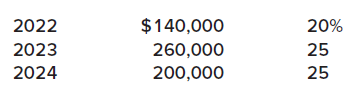

(This exercise is based on the situation described in E 16?24, modified to include a carryforward in addition to a carryback.)Wynn Farms reported a net operating loss of $160,000 for financial reporting and tax purposes in 2021. The enacted tax rate is 25%. Taxable income, tax rates, and income

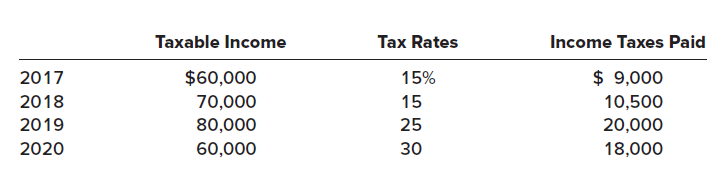

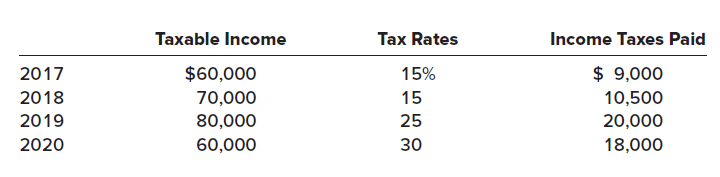

Wynn Farms reported a net operating loss of $100,000 for financial reporting and tax purposes in 2021. The enacted tax rate is 25%. Taxable income, tax rates, and income taxes paid in Wynn?s first four years of operation were as follows: Required:1. Prepare the journal entry to recognize the

During 2021, its first year of operations, Baginski Steel Corporation reported a net operating loss of $360,000 for financial reporting and tax purposes. The enacted tax rate is 25%.Required:1. Prepare the journal entry to recognize the income tax benefit of the net operating loss. Assume the

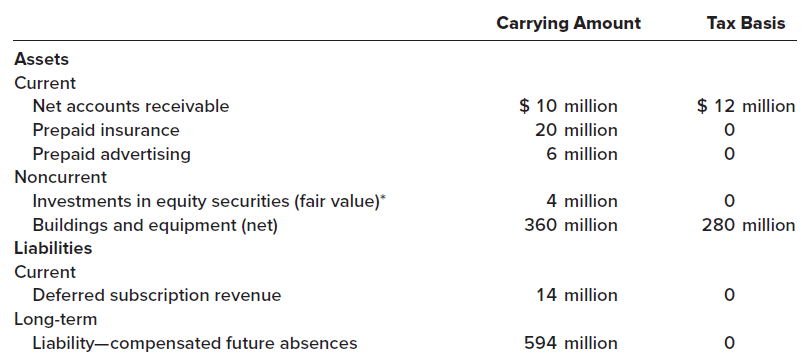

The information that follows pertains to Richards Refrigeration, Inc.:a. At December 31, 2021, temporary differences existed between the financial statement book values and the tax bases of the following ($ in millions): b. No temporary differences existed at the beginning of 2021.c. Pretax

The information that follows pertains to Esther Food Products:a. At December 31, 2021, temporary differences were associated with the following future taxable (deductible) amounts:Depreciation .......................$ 60,000Prepaid expenses .................17,000Warranty expenses

Shwonson Industries reported a deferred tax asset of $5 million for the year ended December 31, 2020, related to a temporary difference of $20 million. The tax rate was 25%. The temporary difference is expected to reverse in 2022, at which time the deferred tax asset will reduce taxable income.

Bronson Industries reported a deferred tax liability of $5 million for the year ended December 31, 2020, related to a temporary difference of $20 million. The tax rate was 25%. The temporary difference is expected to reverse in 2022, at which time the deferred tax liability will become payable.

Arnold Industries has pretax accounting income of $32 million for the year ended December 31, 2021. The tax rate is 25%. The only difference between accounting income and taxable income relates to an operating lease in which Arnold is the lessee. The inception of the lease was December 28, 2021. An

Allmond Corporation, organized on January 3, 2021, had pretax accounting income of $14 million and taxable income of $20 million for the year ended December 31, 2021. The 2021 tax rate is 25%. The only difference between accounting income and taxable income is estimated product warranty costs.

For the year ended December 31, 2021, Fidelity Engineering reported pretax accounting income of $978,000. Selected information for 2021 from Fidelity’s records follows:Interest income on municipal governmental bonds

Southeast Airlines had pretax earnings of $65 million. Included in this amount is income from discontinued operations of $10 million. The company’s tax rate is 25%. What is the amount of income tax expense that Southeast would report in its income statement for continuing operations? How should

Southern Atlantic Distributors began operations in January 2021 and purchased a delivery truck for $40,000. Southern Atlantic plans to use straight-line depreciation over a four-year expected useful life for financial reporting purposes. For tax purposes, the deduction is 50% of cost in 2021, 30%

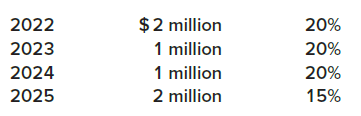

Insure Corporation reported a net operating loss of $25 million for financial reporting and tax purposes. Taxable income last year and the previous year, respectively, was $20 million and $15 million. The enacted tax rate each year is 25%. Assume that Insure qualifies as a type of company that is

(This is a variation of E 16–12, modified to assume a previous balance in the valuation allowance.) At the end of 2020, Payne Industries had a deferred tax asset account with a balance of $25 million attributable to a temporary book-tax difference of $100 million in a liability for estimated

During its first year of operations, Nive.com reported a net operating loss of $15 million for financial reporting and tax purposes. The enacted tax rate is 25%. Prepare the journal entry to recognize the income tax benefit of the net operating loss.

Tru Developers, Inc., sells plots of land for industrial development. Tru recognizes income for financial reporting purposes in the year it sells the plots. For some of the plots sold this year, Tru took the position that it could recognize the income for tax purposes when the installments are

At the end of 2020, Payne Industries had a deferred tax asset account with a balance of $25 million attributable to a temporary book-tax difference of $100 million in a liability for estimated expenses. At the end of 2021, the temporary difference is $64 million. Payne has no other temporary

Superior Developers sells lots for residential development. When lots are sold, Superior recognizes income for financial reporting purposes in the year of the sale. For some lots, Superior recognizes income for tax purposes when the cash is collected. In 2020, Superior sold lots for $20 for which

The long-term liabilities section of CPS Transportation?s December 31, 2020, balance sheet included the following:a. A lease liability with 15 remaining lease payments of $10,000 each, due annually on January 1: Lease liability ..........................$ 76,061Less: Current portion

J-Matt, Inc., had pretax accounting income of $291,000 and taxable income of $300,000 in 2021. The only difference between accounting and taxable income is estimated product warranty costs of $9,000 for sales in 2021. Warranty payments are expected to be in equal amounts over the next three years

(Note: this problem is a variation of P 16–10, modified to allow a net operating loss carryback.) Fore Farms reported a pretax operating loss of $137 million for financial reporting purposes in 2021. Contributing to the loss were (a) a penalty of $5 million assessed by the Environmental

Fore Farms reported a pretax operating loss of $137 million for financial reporting purposes in 2021. Contributing to the loss were (a) a penalty of $5 million assessed by the Environmental Protection Agency for violation of a federal law and paid in 2021 and (b) an estimated loss of $12 million

Differences between pretax accounting income and taxable income were as follows during 2021:

Corning-Howell reported taxable income in 2021 of $120 million. At December 31, 2021, the reported amount of some assets and liabilities in the financial statements differed from their tax bases as indicated below: The total deferred tax asset and deferred tax liability amounts at January 1,

In late 2017 the federal tax rate for subsequent years was decreased from 35% to 21%. How would this affect an existing deferred tax liability? How would the change be reflected in net income?

Arndt, Inc. reported the following for 2021 and 2022 ($ in millions): a. Expenses each year include $30 million from a two-year casualty insurance policy purchased in 2021 for $60 million. The cost is tax deductible in 2021.b. Expenses include $2 million insurance premiums each year for life

Lance Lawn Services reports warranty expense by estimating the amount that eventually will be paid to satisfy warranties on its product sales. For tax purposes, the expense is deducted when the warranty work is completed. At December 31, 2021, Lance has a warranty liability of $2 million and

At the end of the year, the deferred tax asset account had a balance of $4 million attributable to a temporary difference of $16 million in a liability for estimated expenses. Taxable income is $60 million. No temporary differences existed at the beginning of the year, and the tax rate is 25%.

Sherrod, Inc., reported pretax accounting income of $76 million for 2021. The following information relates to differences between pretax accounting income and taxable income:a. Income from installment sales of properties included in pretax accounting income in 2021 exceeded that reported for tax

In 2021, DFS Medical Supply collected rent revenue for 2022 tenant occupancy. For income tax reporting, the rent is taxed when collected. For financial statement reporting, the rent is recorded as deferred revenue and then recognized as revenue in the period tenants occupy the rental property. The

Refer to the situation described in BE 16–5. Suppose the deferred portion of the rent collected was $40 million at the end of 2022. Taxable income is $200 million. Prepare the appropriate journal entry to record income taxes in 2022.BE 16–5In 2021, Ryan Management collected rent revenue for

You are the new accounting manager at the Barry Transport Company. Your CFO has asked you to provide input on the company’s income tax position based on the following:1. Pretax accounting income was $45 million and taxable income was $8 million for the year ended December 31, 2021.2. The

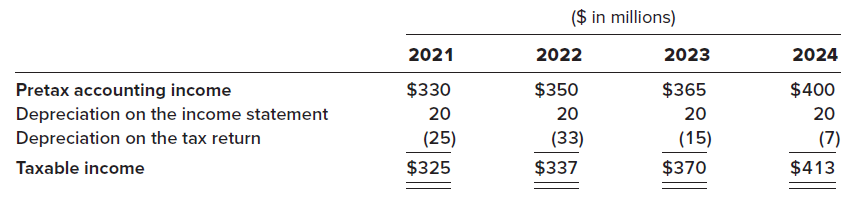

(This exercise is a variation of E 16?4, modified to have the asset fully depreciated in the year of purchase.) Ayres Services acquired an asset for $80 million in 2021. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). Ayers

In 2021, Ryan Management collected rent revenue for 2022 tenant occupancy. For financial reporting, the rent is recorded as deferred revenue and then recognized as revenue in the period tenants occupy rental property. For tax reporting, the rent is taxed when collected in 2021. The deferred portion

The DeVille Company reported pretax accounting income on its income statement as follows:2021 ..........$ 350,0002022 .............270,0002023 .............340,0002024 .............380,000Included in the income of 2021 was an installment sale of property in the amount of $50,000. However, for tax

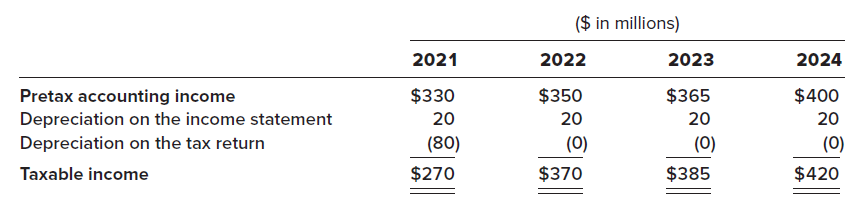

Ayres Services acquired an asset for $80 million in 2021. The asset is depreciated for financial reporting purposes over four years on a straight-line basis (no residual value). For tax purposes the asset?s cost is depreciated by MACRS. The enacted tax rate is 25%. Amounts for pretax accounting

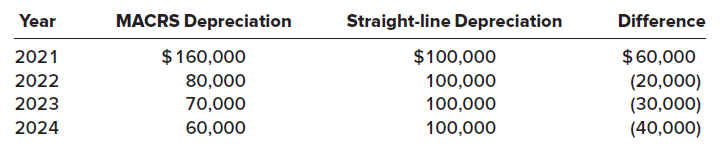

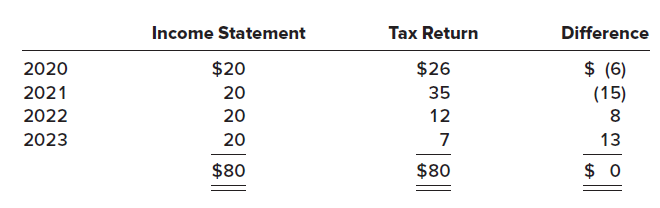

Zekany Corporation would have had identical income before taxes on both its income tax returns and income statements for the years 2021 through 2024 except for differences in depreciation on an operational asset. The asset cost $120,000 and is depreciated for income tax purposes in the following

(This exercise is a variation of E 16–2, modified to have the asset fully depreciated in the year of purchase.) On January 1, 2018, Ameen Company purchased major pieces of manufacturing equipment for a total of $36 million. Ameen uses straight-line depreciation for financial statement reporting

Milo Manufacturing uses straight-line depreciation for financial statement reporting and is able to deduct 100% of the cost of equipment in the year the equipment is purchased for tax purposes. Four years after its purchase, one of Milo’s manufacturing machines has a book value of $600,000. There

Dixon Development began operations in December 2021. When lots for industrial development are sold, Dixon recognizes income for financial reporting purposes in the year of the sale. For some lots, Dixon recognizes income for tax purposes when collected. Income recognized for financial reporting

On January 1, 2018, Ameen Company purchased major pieces of manufacturing equipment for a total of $36 million. Ameen uses straight-line depreciation for financial statement reporting and MACRS for income tax reporting. At December 31, 2020, the book value of the equipment was $30 million and its

Showing 4300 - 4400

of 6751

First

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

Last

Step by Step Answers