New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

principles corporate finance

Global Corporate Finance Text And Cases 6th Edition Suk H. Kim, Seung H. Kim - Solutions

Boeing sells an airplane to Korean Airlines for 840 million won with terms of 1 year. Boeing will receive its payment in Korean won. The spot rate for the Korean currency is 700 won per dollar and Boeing expects to exchange 840 million won for $1.2 million (840 millionΠ 700) when payment is

For the coming year, a Singapore subsidiary of an American company is expected to earn an after-tax profit of S\($25\) million and its depreciation charge is estimated at S\($5\) million.The exchange rate is expected to rise from S\($2.00\) per dollar to S\($1.5\) per dollar for the next year.(a)

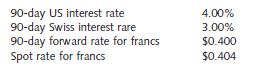

A US company purchased several boxes of watches from a Swiss company for SFr300,000.This payment must be made in Swiss francs 90 days from today. The following quotations and expectations exist:Would the company be better off using the forward market hedge or the money market hedge? 90-day US

For the coming year, a British subsidiary of an American company is expected to incur an after-tax loss of £50 million and its depreciation charge is estimated at £10 million. The exchange rate is expected to rise from \($1.5\) per pound to \($1.7\) per pound for the next year. What is the

A US company has bought a number of TV sets from a Japanese company for ¥100,000.This payment must be made in Japanese yen 180 days from today. The following quotations and expectations exist:The US company does not have any idle dollar balances at present, but it expects to have adequate cash in

An American firm has just sold merchandise to a British customer for £100,000, with payment in British pounds 3 months from now. The US company has purchased from its bank a 3-month put option on £100,000 at a strike price of \($1.6660\) per pound and a premium cost of \($0.01\) per pound. On the

Assume that a subsidiary in New Zealand needs NZ\($500,000\) and that a credit swap has been proven the least costly hedged alternative. Further assume that the best unhedged alternative is the direct loan from the parent and that the cost of the direct loan is 20 percent. The current exchange rate

Western Mining Company (WMC) is an Australia-based minerals producer with business interests in 19 countries. It is the world’s third largest nickel producer, owns 40 percent of the world’s largest alumina producer (Alcoa World Alumina and Chemicals), and is a major producer of copper, uranium,

Explain the conditions under which items and/or transactions are exposed to foreign exchange risks.

Three basic types of exchange exposure are translation exposure, transaction exposure, and economic exposure. Briefly explain each of these three types of exposure.

What is the basic purpose of exposure netting?

How does FASB 8 differ from FASB 52?

How will the weakened US dollar affect the reported earnings of a US company with subsidiaries all over the world? How will the strengthened US dollar affect the reported earnings of a US company with subsidiaries all over the world?

How could an MNC use leading and lagging to hedge its soft-currency receivables and its soft-currency payables?

Which method do most MNCs use to hedge their translation exposure: financial instruments or operational techniques?

A US company has a single, wholly owned affiliate in Japan. This affiliate has exposed assets of ¥500 million and exposed liabilities of ¥800 million. The exchange rate appreciates from ¥150 per dollar to ¥100 per dollar.(a) What is the amount of net exposure?(b) What is the amount of the

The British subsidiary of a US company had current assets of £1 million, fixed assets of £2 million, and current liabilities of £1 million at both the beginning and the end of the year.There are no long-term liabilities. The pound depreciated during the year from \($1.50\) per pound to \($1.30\)

Assume that a Malaysian subsidiary of a US company has the following: (1) cash =M\($1,000;\) (2) accounts receivable = M\($1,500;\) (3) inventory = M\($2,000;\) (4) fixed assets= M\($2,500;\) (5) current liabilities = M\($1,000;\) (6) long-term debt = M\($3,000;\) (7) net worth= M\($3,000;\) and

In 1982, Ford incurred an after-tax loss of \($658\) million, adopted FASB 52, and had a translation loss of \($220\) million. In the same year, General Motors earned an after-tax profit of\($963\) million, used FASB 8, and had a translation gain of \($348\) million.(a) Why do you think that in

Assume that a subsidiary in New Zealand needs NZ\($500,000\) and that a credit swap has been proven to be the least costly hedged alternative. Further assume that the best unhedged alternative is the direct loan from the parent and that the cost of the direct loan is 20 percent. The current

The current exchange rate of Saudi Arabian riyal is SR4 per \($1.\) The Exton Company, the Saudi Arabian subsidiary of a US multinational company, has the following balance sheet:If the Saudi Arabian riyal devalues from SR4 per \($1\) to SR5 per \($1,\) what would be the translation loss (gain)

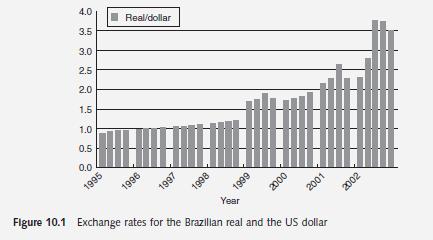

At the end of 2002, Todd Pickett, CFO of Dell Mercosur, was faced with conflicting predictions of the value of the Brazilian currency, the real, and what to do to hedge Dell’s operation in Brazil. Although Pickett was concerned about Dell’s exposure in the other Mercosur countries, especially

Explain the globalization of financial markets.

How has technology affected the globalization of financial markets?

Why has the Eurocurrency market grown so rapidly?

If Germany imposes interest rate ceilings on German bank deposits, what is the likely effect of this regulation on the euro interest rate?

Why have bank regulators and market analysts expressed some concern about the stability of the interbank market?

What is the difference between currency option bonds and currency cocktail bonds?

Describe two new instruments: Euronotes and global bonds.

Explain the Basel Accord of 1988.

What is the major difference in the role of commercial banks in corporate governance between the USA and Japan?

How can a government privatize state-owned companies?

In April 2003, the Basel Committee on Banking Supervision released for public comment the new Basel Capital Accord, which will replace the 1988 Capital Accord. What are the three pillars of this new proposal?

What are some reasons for a company to crosslist its shares?

The World Bank highlighted three aspects of the recent developing-country shift from debt to equity in its 2003 Global Development Finance. Briefly describe these three aspects of the shift.

Fill in the following blank spaces with a reserve ratio of 20 percent: Acquired reserves Required reserves Excess reserves Amount bank can lend Bank 1 $100.00 $20.00 $80.00 $80.00 Bank 2 Bank 3 Bank 4 Bank 5 Bank 6 Bank 7 Bank 8 Bank 9 Bank 10 Bank 11 Bank 12 Bank 13 Total amount loaned

Assume that an international bank has the following simplified balance sheet. The reserve ratio is 20 percent:(a) Determine the maximum amount that this bank can safely lend. Show in column 1 how the bank’s balance sheet will appear after the bank has loaned this amount.(b) By how much has the

A multinational company holds a $1,000 zero-coupon bond with a maturity of 15 years and a yield rate of 16 percent. What is the market value of the zero-coupon bond?

A multinational company has issued a 10-year, $1,000 zero-coupon bond to yield 10 percent.(a) What is the initial price of the bond?(b) If interest rates dropped to 8 percent immediately upon issue, what would be the price of the bond?(c) If interest rate rose to 12 percent immediately upon issue,

A multinational company has common stock outstanding. Each share of the common stock pays $3.60 dividends per year, and the stockholder requires a 12-percent rate of return.What is the price of the common stock?

The effect of foreign-currency fluctuations on a company depends on a company’s business structure, its industry profile, and its competitive environment. This case recounts how Merck assessed its foreign-exchange exposure and decided to hedge those exposures.The Company In 2001, Merck celebrated

Why have currency swaps replaced parallel loans?

Explain both interest rate swaps and currency swaps. Which instrument has a greater credit risk: an interest rate swap or a currency swap?

How can a typical mortgage company use an interest rate swap to escape the interest rate risk?

How can multinational companies utilize a currency swap to reduce borrowing costs?

If you expect short-term interest rates to rise more than the yield curve should suggest, would you rather pay a fixed long-term rate and receive a floating short-term rate, or receive a fixed long-term rate and pay a floating short-term rate?

What is the role of the notional principal in understanding swap transactions? Why is this principal amount regarded as only notional?

Comment on the following statement: “If one party benefits from a swap, the other party must lose.”

What are call swaptions and put swaptions? Compare a call swaption with an interest rate cap.

Describe an interest rate collar. How will it be used?

What are advantages of financial swaps over currency futures and options?

What are major limitations of financial swaps?

A swap agreement covers a 5-year period and involves annual interest payments on a $1 million principal amount. Party A agrees to pay a fixed rate of 12 percent to party B. In return, party B agrees to pay a floating rate of LIBOR + 3 percent to party A. The LIBOR is 10 percent at the time of the

Assume that the current spot rate for the Polish zloty is 2.5 zlotys per dollar (\($0.40\) per zloty), the US interest rate is 10 percent, and the Polish interest rate is 8 percent. Party C wishes to exchange 25 million zlotys for dollars. In return for these zlotys, party D would pay \($10\)

A mortgage company (party E) has just lent \($1\) million for 5 years at 12 percent with annual payments, and it pays a deposit rate that equals LIBOR + 1 percent. With these rates, the company would lose money if the LIBOR exceeds 11 percent. This vulnerability prompts the mortgage company to

The current spot rate for the Polish zloty is 2.5 zlotys per dollar or \($0.40\) per zloty. Party G has access to zlotys at a rate of 7 percent, while party H must pay 8 percent to borrow zlotys. On the other hand, party H can borrow dollars at 9 percent, while party G must pay 10 percent for its

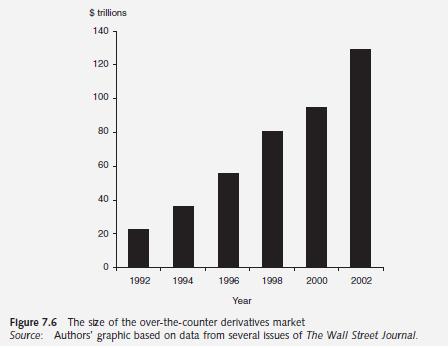

Financial derivatives – forwards, futures, options, and swaps – are contracts whose values are linked to or derived from values of underlying assets, such as securities, commodities, and currencies.There are two types of markets for financial derivatives: organized exchanges and

Describe corporate motives for currency forecasting.

If foreign-exchange markets are perfectly efficient, why should no one pay for the services of currency forecasting firms?

Most empirical studies have found that foreign-exchange markets are at least weakform efficient. Does this mean that investors can earn extra profits by using technical analysis?

Explain fundamental analysis as a technique for forecasting exchange rates.

Explain technical analysis as a technique for forecasting exchange rates.

Explain the market-based forecast as a technique for forecasting exchange rates.

How can we assess performance in forecasting exchange rates?

In the early 1990s, some former Eastern-bloc countries allowed the exchange rates of their currencies to fluctuate against the dollar. Would the use of fundamental analysis be useful for forecasting the future exchange rates of these currencies?

Explain the events that would force the par value to change.

A general rule suggests that in a fixed-rate system, the forecaster ought to focus on the government decision-making structure. Explain.

Why do the central banks of countries with flexible exchange rate systems intervene in the foreign-exchange market?

The beginning spot rate is $0.1854 per South African rand and the ending spot rate is$0.20394 per rand.(a) Calculate the percentage change in the exchange rate for the rand against the dollar.(b) Calculate the percentage change in the exchange rate for the dollar against the rand.

The beginning spot rate is \($0.1040\) per Chinese yuan and the ending spot rate is \($0.0936\) per yuan.(a) What is the percentage change in the exchange rate for the yuan?(b) What is the percentage change in the exchange rate for the dollar?

The spot rate is $0.60 per Swiss franc. The 4-year annualized inflation rate is 9 percent in the USA and 6 percent in Switzerland.(a) What is the expected percentage appreciation or depreciation of the franc over the 4-year period?(b) What is the forecast for the franc’s spot rate in 4 years?

A US company’s forecast for the percentage change in the British pound (BP) depends on only three variables: inflation rate differentials, US inflation minus British inflation (I); differentials in the rate of growth in money supply, the growth rate in US money supply minus the growth rate in

The spot rate is $0.5800 per Singapore dollar. The 90-day forward premium for Singapore dollars is 13.79 percent. What is the expected spot rate in 90 days?

The spot rate is $0.08 per Spanish peseta. The annual interest rates are 4 percent for the USA and 9 percent for Spain. What is the market’s forecast of the spot rate in 2 years?

The forecasted value for the Mexican peso is \($0.1200\) and its realized value is $0.1000.What is the forecast error (root square error) for the peso?

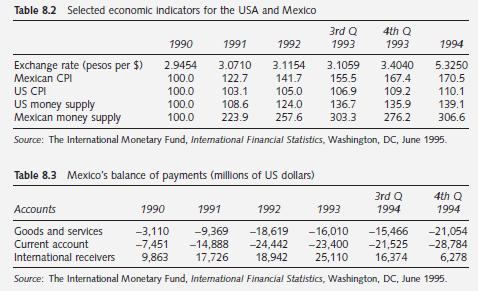

Although Mexico had allowed its peso to fluctuate within a narrow band, the government had virtually pegged the peso to the US dollar since 1990. However, on December 20, 1994, Mexico unexpectedly announced its decision to float the peso and a 40 percent devaluation followed in the next 2 days. The

How should appreciation of a company’s home currency affect its cash inflows? How should depreciation of a company’s home currency affect its cash inflows?

What should management do to protect assets adequately against risks from exchange rate fluctuations?

What are the two major types of hedging tools?

Which exposure is more difficult to manage: transaction exposure or economic exposure?

How could a US company hedge net payables in Japanese yen in terms of forward and options contracts?

How could a US company hedge net receivables in Japanese yen in terms of forward and options contracts?

Are there any special situations in which options contracts are better than forward contracts or vice versa?

What are the major problems of economic exposure management?

What is the basic purpose of economic exposure management?

How do most companies deal with their economic exposure?

If the Swiss franc is selling for \($0.5618\) and the Japanese yen is selling for \($0.0077,\) what is the cross rate between these two currencies?

(a) If the spot rate changes from \($0.11\) per peso to \($0.10\) per peso over a 1-year period, what is the percentage change in the value of the Mexican peso?(b) If the spot rate changes from Mex\($10.00\) per dollar to Mex\($9.00,\) what is the percentage change in the value of the Mexican peso?

If a bank’s bid price is \($1.60\) for the British pound and its ask price is \($1.65,\) what is the bid–ask spread for the pound?

Assume: (1) the spot rate for Canadian dollars is \($0.8089;\) (2) the 180-day forward rate for Canadian dollars is \($0.8048;\) (3) the spot rate for Swiss francs is \($0.4285;\) and (4) the 180-day forward rate for Swiss francs is \($0.4407.\) Determine the 180-day forward discount or premium on

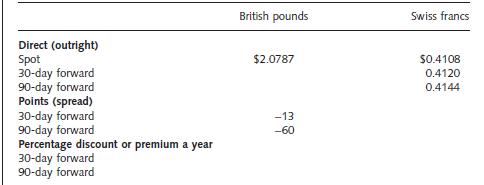

Fill in the following blank spaces: Direct (outright) Spot 30-day forward 90-day forward Points (spread) 30-day forward 90-day forward Percentage discount or premium a year 30-day forward 90-day forward British pounds $2.0787 -13 -60 Swiss francs $0.4108 0.4120 0.4144

Assume that the current exchange rate is $2.00 per pound, the US inflation rate is 10 percent for the coming year, and the British inflation rate is 5 percent over the same period. What is the best estimate of the pound future spot rate 1 year from now?

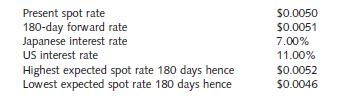

The following quotations and expectations exist for the Swiss franc:(a) What is the premium or discount on the forward Swiss franc?(b) If your expectation proves correct, what would be your dollar profit or loss from investing $4,000 in the spot market? How much capital would you need now to carry

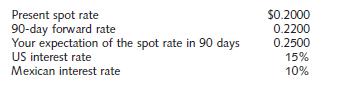

An American firm purchases \($4,000\) worth of perfume (Mex\($20,000)\) from a Mexican firm. The American distributor must make the payment in 90 days, in Mexican pesos.The following quotations and expectations exist for the Mexican peso:(a) What is the premium or discount on the forward Mexican

You must make a $100,000 domestic payment in Los Angeles in 90 days. You have$100,000 now and decide to invest it for 90 days either in the USA or in the UK. Assume that the following quotations and expectations exist:a) Where should you invest your $100,000 to maximize your yield with no risk?(b)

The theory of purchasing power parity (PPP) is one of the oldest theories in international economics.The theory states that, in the long run, the exchange rates between two currencies should move toward the rate that would equalize the prices of an identical basket of goods and services in the two

What is the most important difference between futures and options contracts?

What are the major types of margin with respect to a futures contract? What is the role of a margin requirement?

How can speculators use currency futures?

How can US companies use currency futures?

Showing 4700 - 4800

of 5445

First

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

Step by Step Answers