New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

real estate principles

Real Estate Finance and Investments 14th edition William Brueggeman, Jeffrey Fisher - Solutions

List and characterize equity REITs based on their investment objectives.

What are the three principal types of REITs?

What are the general requirements regarding income, investments, and dividends with which a REIT must comply to maintain its tax-exempt status?

What is the main difference between organizing a real estate venture a corporation versus a general partnership? How does a limited partnership have some of the characteristics of both?

How are general partners usually compensated in a syndication? What major concerns should investors consider when making an investment with a syndication

Differentiate between public and private syndications? What is an accredited investor? Why is the distinction used?

What concerns should an investor in a real estate syndication have regarding general partners?

Why do you think the Tax Reform Act of 1986 affected the desirability of investing in real estate syndications?

What are the different ways that the general partner is compensated?

How does the risk associated with investment in a partnership differ for the general partner versus a limited partner?

What is the significance of capital accounts? What causes the balance in a capital account to change each year?

What causes the after-tax IRR (ATIRRe) for the general partner to differ from that of the limited partner?

What are special allocations?

What is the main difference between the way a partnership is taxed versus the way a corporation is taxed?

Suppose the split between the limited and general partner is 99 percent for the limited partner and 1 percent for the general partner for equity contributions, income, and allocation of gain. How does this change the expected return to each partner?

Why is the Internal Revenue Service concerned with how partnership agreements in real estate are structured?

How can the general partner-syndicator structure the partnership to offer incentives to limited partners?

What is the advantage of the limited partnership ownership form for real estate syndications?

What is the difference between an IRR preference and an IRR lookback?

What are the unique risks of land development projects from the developer’s and lender’s point of view?

Refer to problem 3, Change the assumptions in the file to solve problem 3. Then answer the following questions.a. Determine the release price based on a repayment schedule calling for the loan to be repaid at the following rates: 0 percent, 10 percent, and 30 percent faster than the receipt of

In land development projects, why do lenders insist on loan repayment rates in excess of sales revenue? What is a release price?

What are some of the physical considerations that a developer should be concerned with when purchasing land? How should such considerations be taken into account when determining the price that should be paid?

What is an option contract? How is it used in land acquisition? What should developers be concerned with when using such options? What contingencies may be included in a land option?

How might land development activities be specialized? Why is this activity different from project development discussed in the preceding chapter?

Why is the practice of “holdbacks” used? Who is involved in this practice? How does it affect construction lending?

It is sometimes said that land represents “residual” value. This statement reflects the fact that improvement costs do not vary materially from one location to another whereas rents vary considerably. Hence, land values reflect changes in rents (both up and down) from location to location. Do

What do we mean by overage in a retail lease agreement? How might it be calculated?

What is the major concern construction lenders express about the income approach to estimating value? Why do they prefer to use the cost approach when possible? In the latter case, if the developer has owned the land for five years prior to development would the cost approach be more effective? Why

What is the difference between the assignment of a take-out commitment to the construction lender and a triparty agreement? If neither device is used in project financing, what is the relationship between lenders in such a case?

Why don’t permanent lenders usually provide construction loans to developers? Do construction lenders ever provide permanent loans to developers?

A presale agreement is said to be equivalent to a take-out commitment. What will the construction lender be concerned about if the developer plans to use such an agreement in lieu of a take-out?

Third-party lenders sometimes provide gap financing for project developments. Why is this lending used? How does it work?

What is a mini-perm or bullet loan? When and why is this loan used?

What is a standby commitment? When and why is it used?

What contingencies are commonly found in permanent or take-out loan commitments? Why are they used? What happens if they are not met by the developer?

Describe the process of financing the construction and operation of a typical real estate development. Indicate the order in which lenders who fund project development financing are sought and why this pattern is followed.

a. What is the yield to the lender and the investor’s after-tax IRR if 90 percent of the loan must be drawn during the first four months and 10 percent during the last eight months?b. Repeat (a) assuming 60 percent of the loan is drawn the first four months and 40 percent the last eight months.

What are some development strategies that many developers follow? Why do they follow such strategies?

What are the sources of risk associated with project development?

What factors would tend to affect the value of a lease?

Why should corporations have their real estate appraised on a regular basis?

What factors might cause the highest and best use of real estate to change during the course of typical lease term?

Why might refinancing be considered an alternative to a sale-leaseback?

Why has real estate often been a key factor in corporate restructuring?

Why might it be argued that corporations do not have a comparative advantage when investing in real estate as a means of diversification from the core business?

Why is the cost of financing with a sale-leaseback essentially the same as the return from continuing to own?

Why is the value of corporate real estate often considered “hidden” from shareholders?

Why might the decision to own rather than lease real estate have an unfavorable effect on the corporation’s financial statements?

What would cause the rate of return for an investor that purchases real estate and leases it to the corporation to differ from the rate of return earned by the corporation on the incremental investment in owning versus leasing the same property

How does each of the following affect the IRR on the ATCF difference from owning versus leasing?a. The property can be leased for $175,000 instead of $200,000.b. A loan can be obtained at an 8 percent interest rate instead of 10 percent.

Why might the riskiness of cash flow from the residual value of the real estate differ from the riskiness of cash flow from the corporation’s core business? What would cause these cash flows to be correlated?

Why might the cost of a mortgage loan be greater than the cost of using unsecured corporate debt to finance corporate real estate?

What factors would tend to make leasing more desirable than owning?

What are the main reasons that corporations may choose to own real estate?

Why would an investor consider doing an exchange or an installment sale?

In general, what kinds of tax incentives are available for rehabilitation of real estate income property?

What is meant by the “incremental cost of refinancing?”

What are the benefits and costs of renovation?

Are tax considerations important in renovation decisions?

How important are taxes in the decision to sell a property?

How can tax law changes create incentives for investors to sell their properties to other investors?

Why would refinancing be an alternative to sale of the property?

An investor is considering selling a property that has an adjusted basis of $1.5 million for $2 million. The property has a loan balance of $1.75 million. She is exploring different disposition strategies. All capital gains would be taxed at 20 percent (whether from depreciation recapture or price

Why is refinancing often done in conjunction with renovation?

Suppose both the NOI and property value growth rate are 5 percent instead of 3 percent. How would this change the marginal rate of return for years 1 to 10? Does the MRR increase or decrease for the first year? Does it decrease at a faster or slower rate over time?a

What factors should be considered when deciding whether to renovate a property?

Why might the after-tax internal rate of return on equity (ATIRRe) differ for a new investor versus an existing investor who keeps the property?

What causes the marginal rate of return to change over time? How can the marginal rate of return be used to decide when to sell a property?

Richard Rambo presently owns the Marine Tower office building, which is 20 years old, and is considering renovating it. He purchased the property two years ago for $800,000 and financed it with a 20-year, 75 percent loan at 10 percent interest (monthly payments). Of the $800,000, the appraiser

Lonnie Carson purchased Royal Oaks Apartments two years ago. An opportunity has arisen for Carson to purchase a larger apartment project called Royal Palms, but Carson believes that he would have to sell Royal Oaks to have sufficient equity capital to purchase Royal Palms. Carson paid $2 million

What is the marginal rate of return? How is it calculated?

Refer to problem 1. The owner determines that if the property were renovated instead of sold, after-tax cash flow over the next year would increase to $60,000 and the property could be sold after one year for $2.4 million. Renovation would cost $250,000. The investor would not borrow any additional

Why might the actual holding period for a property be different from the holding period that was anticipated when the property was purchased?

A property could be sold today for $2 million. It has a loan balance of $1 million and, if sold, the investor would incur a capital gains tax of $250,000. The investor has determined that if it were sold today, she would earn an IRR of 15 percent on equity for the past five years. If not sold, the

What factors should an investor consider when trying to decide whether to dispose of a property that he has owned for several years?

How does the use of scenarios differ from sensitivity analysis ?

What is meant by the term ‘overage’ for retail space ?

Refer to the Westgate Shopping Center example. Use ARGUS to replicate the assumptions for the “pessimistic scenario” discussed in the chapter. What inputs did you have to change in order to get the same answer (rounded) as the book?

What is meant by a ‘ real option’ ?

Why is the variance (or standard deviation) used as a measure of risk? What are the advantages and disadvantages of this risk measure?

A developer plans to start construction of a building in one year if at that point rent levels make construction feasible. At that time the building will cost $1,000,000 to construct. During the first year after construction would take place, there is a 60 percent chance that NOI will be $150,000

Use the same information as in problem 3. Now assume a loan for $1.5 million is obtained at a 10 percent interest rate and a 15-year term.a. Calculate the expected IRR on equity and the standard deviation of the return on equity.b. Contrast the results from (a) with those from problem 3. Has the

An investor has projected three possible scenarios for a project as follows:Pessimistic—NOI will be $200,000 the first year, and then decrease 2 percent per year over a five-year holding period. The property will sell for $1.8 million after five years.Most likely—NOI will be level at $200,000

What are some of the types of risk that should be considered when analyzing real estate and other categories of investment?

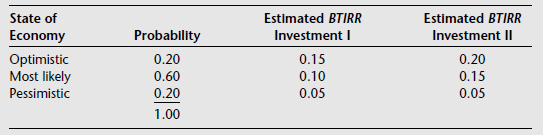

Mike Riskless is considering two projects. He has estimated the IRR for each under three possible scenarios and assigned probabilities of occurrence to each scenario.Riskless is aware that the pattern of returns for Investment II looks very attractive relative to Investment I; however, he believes

What is a risk premium? Why does such a premium exist between interest rates on mortgages and rates of return earned on equity invested in real estate?

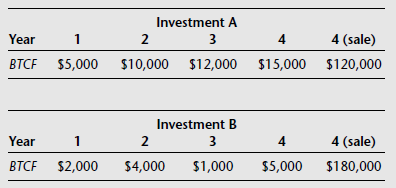

Two investments have the following pattern of expected returns:Investment A requires an outlay of $110,000 and Investment B requires an outlay of $120,000.a. What is the BTIRR on each investment?b. If the BTIRR were partitioned based on BTCFo and BTCFs what proportions of the BTIRR would be

What is meant by partitioning the internal rate of return? Why is this procedure meaningful?

How can the effect of below-market rate loans on value be determined using investor criteria?

What is the traditional cash equivalency approach to determine how below-market rate loans affect value?

What criteria should be used to choose between two financing alternatives?

Refer to the Monument Office Building example. What is the leveraged IRR if the loan-to-value ratio is increased to 80 percent?

What is the motivation for a sale-leaseback of the land?

How do you think participations affect the riskiness of a loan?

A borrower and lender negotiate a $20,000,000 interest-only loan at a 9 percent interest rate for a term of 15 years. There is a lockout period of 10 years. Should the borrower choose to prepay this loan at any time after the end of the 10th year, a yield maintenance fee (YMF) will be charged. The

Why might a lender prefer a loan with a lower interest rate and a participation?

Refer to problem 6. Assume that another alternative is a convertible mortgage (instead of a participation loan) that gives the lender the option to convert the mortgage balance into a 60 percent equity position at the end of year 10. That is, instead of receiving the payoff on the mortgage, the

Why might an investor prefer a loan with a lower interest rate and a participation?

A property is expected to have NOI of $100,000 the first year. The NOI is expected to increase by 3 percent per year thereafter. The appraised value of the property is currently $1 million and the lender is willing to make a $900,000 participation loan with a contract interest rate of 8 percent.

Showing 1000 - 1100

of 1528

First

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

Step by Step Answers