Question:

In January 2018, the management of Branxton Ltd decided on a program of expansion for the business. On 1 July 2018, the company had $900 000 in retained earnings, and another reserve totalling $600 000 had been set aside out of retained earnings for the acquisition of equipment.

Share capital consisted of 2 800 000 shares issued for $1 each. The following events occurred in relation to the equity accounts of Branxton Ltd over the next few years.

Required

(a) Prepare journal entries to record all transactions and events across the 3‐year period.

(b) Show the equity section of the balance sheet of Branxton Ltd as at 31 December 2021.

Transcribed Image Text:

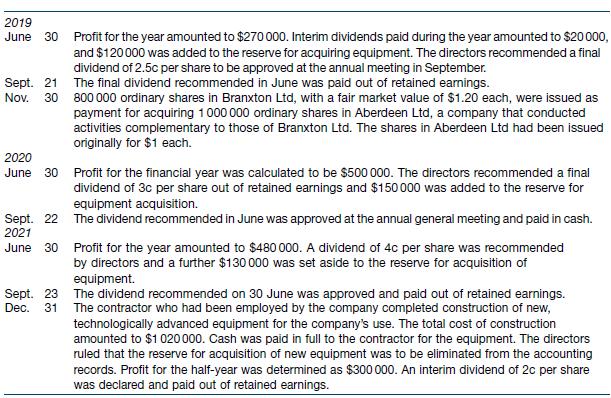

2019 June 30 Profit for the year amounted to $270 000. Interim dividends paid during the year amounted to $20000, Sept. 21 Nov. 30 2020 June and $120,000 was added to the reserve for acquiring equipment. The directors recommended a final dividend of 2.5c per share to be approved at the annual meeting in September. The final dividend recommended in June was paid out of retained earnings. 800 000 ordinary shares in Branxton Ltd, with a fair market value of $1.20 each, were issued as payment for acquiring 1000 000 ordinary shares in Aberdeen Ltd, a company that conducted activities complementary to those of Branxton Ltd. The shares in Aberdeen Ltd had been issued originally for $1 each. 30 Profit for the financial year was calculated to be $500 000. The directors recommended a final dividend of 3c per share out of retained earnings and $150 000 was added to the reserve for equipment acquisition. Sept. 22 The dividend recommended in June was approved at the annual general meeting and paid in cash. 2021 June 30 Profit for the year amounted to $480 000. A dividend of 4c per share was recommended by directors and a further $130 000 was set aside to the reserve for acquisition of equipment. Sept. 23 Dec. 31 The dividend recommended on 30 June was approved and paid out of retained earnings. The contractor who had been employed by the company completed construction of new, technologically advanced equipment for the company's use. The total cost of construction amounted to $1 020 000. Cash was paid in full to the contractor for the equipment. The directors ruled that the reserve for acquisition of new equipment was to be eliminated from the accounting records. Profit for the half-year was determined as $300 000. An interim dividend of 2c per share was declared and paid out of retained earnings.