Consider an investor who must allocate her wealth to (n) assets. The return of each asset, indexed

Question:

Consider an investor who must allocate her wealth to \(n\) assets. The return of each asset, indexed by  , is a random variable \(R_{i}\) with expected value

, is a random variable \(R_{i}\) with expected value  . Asset allocations may be expressed by decision variables \(w_{i}\), representing the fraction of wealth invested in asset \(i\). If we rule out short-selling, these decision variables are naturally bounded by

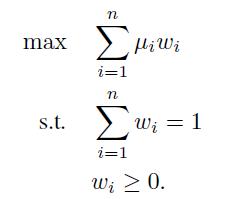

. Asset allocations may be expressed by decision variables \(w_{i}\), representing the fraction of wealth invested in asset \(i\). If we rule out short-selling, these decision variables are naturally bounded by  . If we assume that the investor should just maximize expected return, she should solve the problem

. If we assume that the investor should just maximize expected return, she should solve the problem

Data From Equation (2.1)

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Munir Ahmed Jakhro

I am professional Tutor of of Business Courses, I did my four years Bachelor Degree from one of the Top Business schools of World "Institute of Business Administration" in year 2013. Since then I have been working as Tutor of Accounting, Finance tutor on different online platforms like this website. I am have experience of 6 years teaching business courses to students online and offline my professional job at national savings also helped me in accounting understanding .

8+ Reviews

10+ Question Solved

Related Book For

An Introduction To Financial Markets A Quantitative Approach

ISBN: 9781118014776

1st Edition

Authors: Paolo Brandimarte

Question Posted: