Groupe Casino is a French multinational company that operates more than 9,000 multiformat retail storeshypermarkets, supermarkets, discount

Question:

Groupe Casino is a French multinational company that operates more than 9,000 multiformat retail stores—hypermarkets, supermarkets, discount stores, convenience stores, and restaurants— throughout the world. It has two series of perpetual bonds described below in excerpts from its 2018 financial statements.

12.5 Deeply-subordinated perpetual bonds (TSSDI)

At the beginning of 2005, the Group issued 600,000 deeply-subordinated perpetual bonds (TSSDI) for a total amount of €600 million. The notes are redeemable solely at the Group’s discretion and interest payments are due only if the Group pays a dividend on its ordinary shares in the preceding 12 months. The bonds pay interest at the 10-year constant maturity swap rate plus 100 bps, capped at 9%. In 2018, the average coupon was 1.93% (2017: 1.71%). On 18 October 2013, the Group issued €750 million worth of perpetual hybrid bonds (7,500 bonds) on the market. The bonds are redeemable at the Company’s discretion with the first call date set for 31 January 2019 (not exercised) and the second on 31 January 2024. The bonds paid interest at 4.87% until 31 January 2019. Since then, as specified in the prospectus, the interest rate has been reset at 3.992%. This rate will be reset every five years. Given their specific characteristics in terms of maturity and remuneration, the bonds are carried in equity for the amount of €1,350 million. Issuance costs net of tax have been recorded as a deduction from equity.

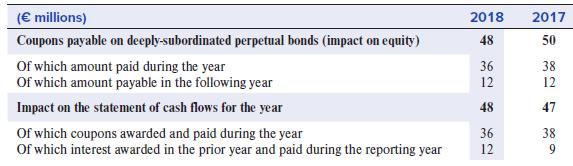

The coupon payable on deeply-subordinated perpetual bonds is as follows:

Required:

1. Casino management treated the notes as equity instruments for financial reporting purposes in accordance with International Financial Reporting Standards (IFRS).

What specific IFRS guidance helps accountants and auditors distinguish between liabilities and equities?

2. Do you concur with management’s decision to treat the notes as equity instruments? Why?

3. Prepare the journal entries Casino would use to record (a) issuance of the bonds on October 18, 2013, and (b) 2018 interest expense and interest paid for both series of perpetual bonds. Income tax considerations may be ignored.

4. How would the Casino notes be treated under U.S. GAAP?

Step by Step Answer:

Requirement 1 IFRS Guidance International Accounting Standards IAS No 32 states that the issuer of a financial instrument shall classify the instrument or its component parts on initial recognition as ...View the full answer

Financial Reporting And Analysis

ISBN: 9781260247848

8th Edition

Authors: Lawrence Revsine, Daniel Collins, Bruce Johnson, Fred Mittelstaedt, Leonard Soffer