In the long run in a perfectly competitive industry, price equals marginal cost and firms earn no

Question:

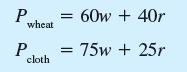

In the long run in a perfectly competitive industry, price equals marginal cost and firms earn no economic profits. The following two equations describe this longrun situation for prices and costs, where the numbers indicate the amounts of each input (labor and land) needed to produce a unit of each product (wheat and cloth):

a. If the price of wheat is initially 100 and the price of cloth is initially 100, what are the values for the wage rate, w , and the rental rate, r ? What is the labor cost per unit of wheat output? Per unit of cloth? What is the rental cost per unit of wheat?

Per unit of cloth?

b. The price of cloth now increases to 120.

What are the new values for w and r (after adjustment to the new long-run situation)?

c. What is the change in the real wage (purchasing power of labor income) with respect to each good? Is the real wage higher or lower “on average”? What is the change in the real rental rate (purchasing power of land income) with respect to each good? Is the real rental rate higher or lower “on average”?

d. Relate your conclusions in part c to the Stolper–Samuelson theorem.

Step by Step Answer:

a With prices of 100 the two equations are Solving these simultaneously the equilibrium wage rate is ...View the full answer