Question: Convert the following stochastic problem into an equivalent deterministic model. subject to Assume that a 1 and a 3 are independent and normally distributed random

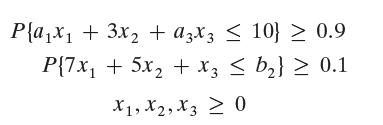

Convert the following stochastic problem into an equivalent deterministic model.

subject to

Assume that a1 and a3 are independent and normally distributed random variables with means E{a1} = 2 and E{a3} = 5 and variances var{a1} = 9 and var{a3} = 16 and that b2 is normally distributed with mean 15 and variance 4.

Maximize z = x + 2x + 5x3

Step by Step Solution

★★★★★

3.52 Rating (162 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Constraint 1 Constraint 2 ... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock