Question: We have a historical data set containing the values of a times series r(1), . . . , r(T). Our goal is to predict if

We have a historical data set containing the values of a times series r(1), . . . , r(T). Our goal is to predict if the time-series is going up or down. The basic idea is to use a prediction based on the sign of the output of an auto-regressive model that uses n past data values (here, n is fixed). That is, the prediction at time t of the sign of the value r(t +1) – r(t) is of the form

In the above, ω ∈ Rn is our classifier coefficient, b is a bias term, and n

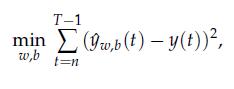

1. As a first attempt, we would like to solve the problem

where y(t) = sgn(r(t + 1) – r(t)). In other words, we are trying to match, in a least-squares sense, the prediction made by the classifier on the training set, with the observed truth. Can we solve the above with convex optimization? If not, why?

2. Explain how you would set up the problem and train a classifier using convex optimization. Make sure to define precisely the learning procedure, the variables in the resulting optimization problem, and how you would find the optimal variables to make a prediction.

w,b (t) = sgn (wr(t) +...+wnr(t n + 1) + b),

Step by Step Solution

3.49 Rating (166 Votes )

There are 3 Steps involved in it

1 The problem is not convex in b 2 We can use a support vector machine for example For t 1 ... View full answer

Get step-by-step solutions from verified subject matter experts