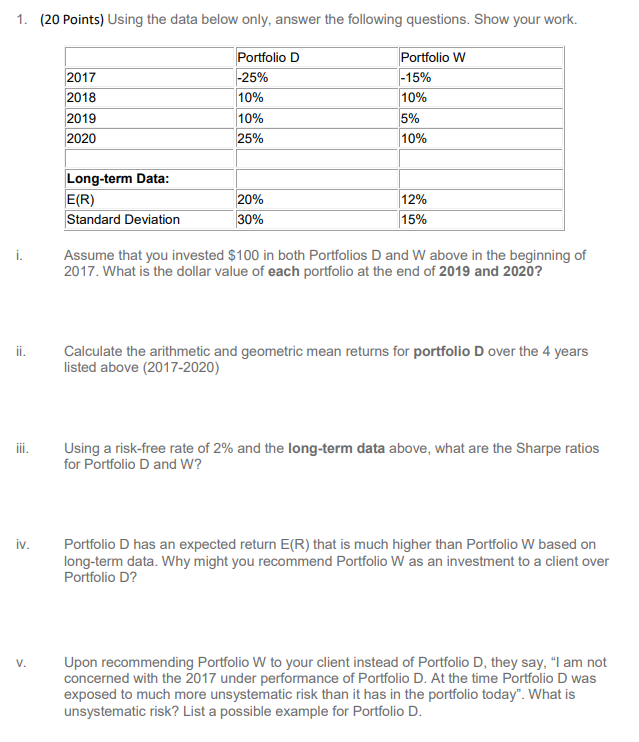

Question: 1. (20 Points) Using the data below only, answer the following questions. Show your work. Portfolio D Portfolio W 2017 -25% -15% 2018 10% 10%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock