Question: 1) Using the Black-Scholes pricing function in Excel, compute an option value for each strike price and maturity date in case Exhibit 2. For simplicity,

1) Using the Black-Scholes pricing function in Excel, compute an option value for each strike price and maturity date in case Exhibit 2. For simplicity, assume zero dividend yield. Also, use Louise Itos volatility estimates, provided in case Exhibit 1.  2) Does the model yield logical estimates with respect to intrinsic value and time-to-maturity? What happens to the option premiums as you change the volatility? Can you explain why volatility affects prices in such a manner?

2) Does the model yield logical estimates with respect to intrinsic value and time-to-maturity? What happens to the option premiums as you change the volatility? Can you explain why volatility affects prices in such a manner?

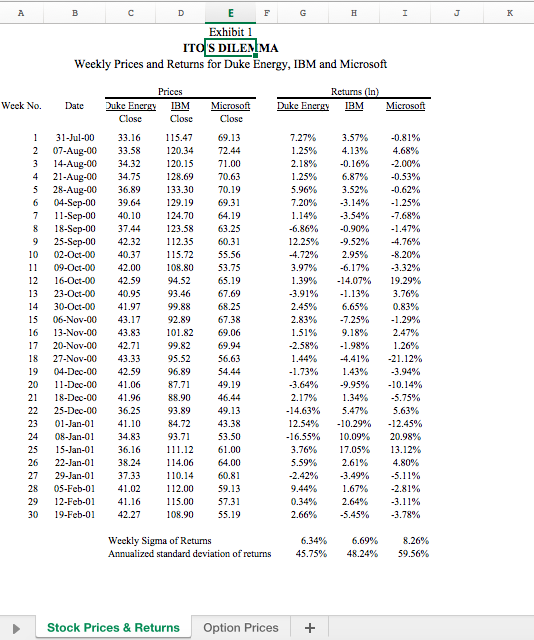

Exhibit 1 ITO S DILEM MA Weekly Prices and Returns for Duke Energy, IBM and Microsoft Exhibit 1 ITO S DILEM MA Weekly Prices and Returns for Duke Energy, IBM and Microsoft

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock