Question: 1. Using the information in the table, compute the structure of the optimal portfolio W when there are two risky assets, bond fund and stock

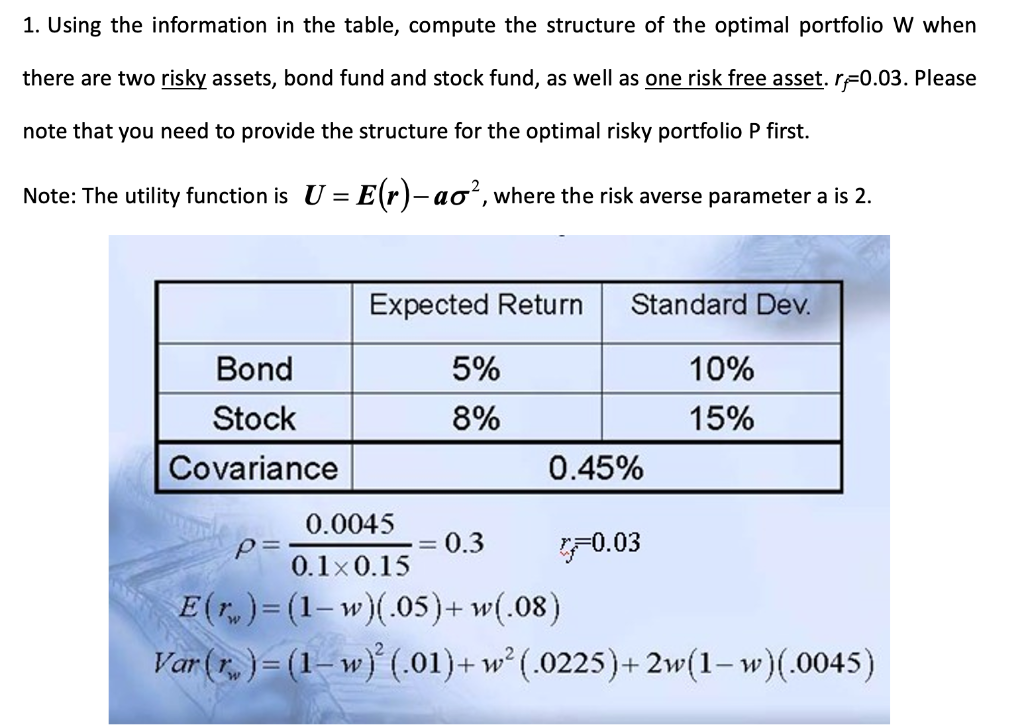

1. Using the information in the table, compute the structure of the optimal portfolio W when there are two risky assets, bond fund and stock fund, as well as one risk free asset. r=0.03. Please note that you need to provide the structure for the optimal risky portfolio P first. Note: The utility function is U = E(r)-ao?, where the risk averse parameter a is 2. Expected Return Standard Dev. Bond 5% 10% Stock 8% 15% Covariance 0.45% 0.0045 P 0.3 520.03 0.1x 0.15 E()=(1-w)(.05)+ w(.08) Var((.)= (1-w) (.01)+ w (0225)+2w(1-w)(0.0045)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock