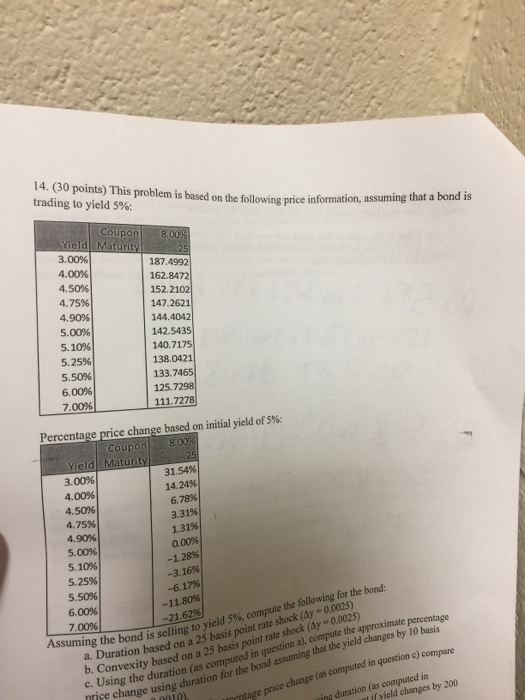

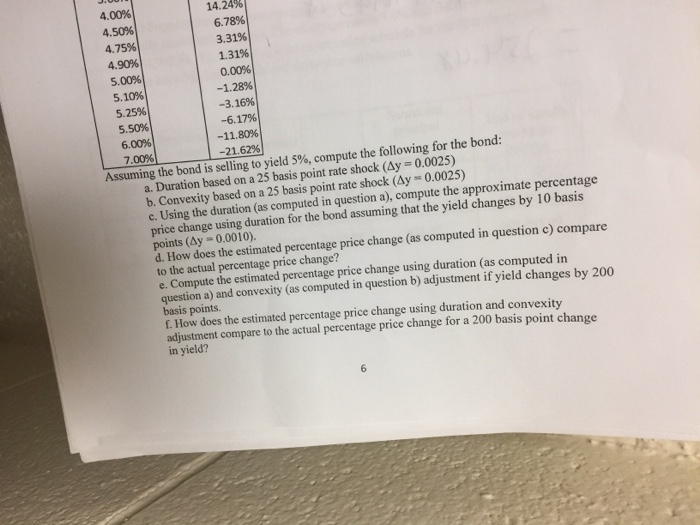

Question: 14. (30 points) This problem is based on the following price information, assuming that a trading to yield 5%; pon 3.00% 4.00% 4.50% 4.75% 4.90%

14. (30 points) This problem is based on the following price information, assuming that a trading to yield 5%; pon 3.00% 4.00% 4.50% 4.75% 4.90% 5.00% 5.10% 5.25% 5.50% 6.00% 187.4997 162.8472 152.2102 147.2621 144.4042 142.5435 140.7175 138.0421 133.7465 125.7298 111.7278 7.00% Percentage price change based on initial yield of 5% 3.00% 4.00% 4.50% 4.75% 4.90% 5.00% 5.10% 5.25% 5.50% 31.54% 14.24% 6.78% 3.31%) 1.31%! 0.00% -1.28% -3.16% ; ' -617% -1 1.80% 6.00% 7.00% a. Duration based on a 25 basis point rate shock (Ay 0.0025) b. Convexity based on a 25 basis point rate c. Using the duration (as computed compute the following for the bond: suming the bond issellingto yield 5%, shock (Ay 0.0025) approximate ge using duration for the bond assuming that the yield changes by 10 ing duration (as computed in basis in question a), compute the nrie change rrntage price change (as computed in question c t if yield changes by 200

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts