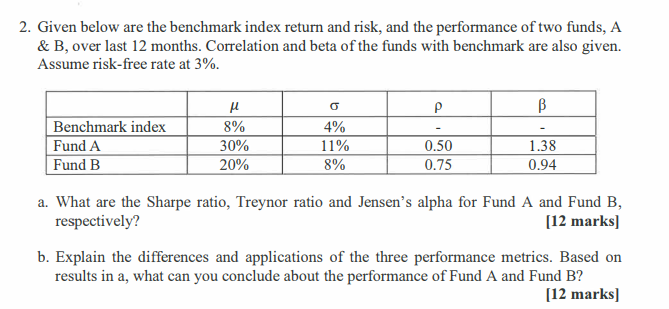

Question: 2. Given below are the benchmark index return and risk, and the performance of two funds, A & B, over last 12 months. Correlation and

2. Given below are the benchmark index return and risk, and the performance of two funds, A & B, over last 12 months. Correlation and beta of the funds with benchmark are also given. Assume risk-free rate at 3%. 0 B Benchmark index Fund A Fund B 8% 30% 20% 4% 11% 8% 0.50 0.75 1.38 0.94 a. What are the Sharpe ratio, Treynor ratio and Jensen's alpha for Fund A and Fund B, respectively? [12 marks] b. Explain the differences and applications of the three performance metrics. Based on results in a, what can you conclude about the performance of Fund A and Fund B? [12 marks]

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock