Question: 2. The following table lists the expected returns and standard deviation of returns for 3 assets: Asset 1 0.1 0.1 Asset 2 0.2 0.2

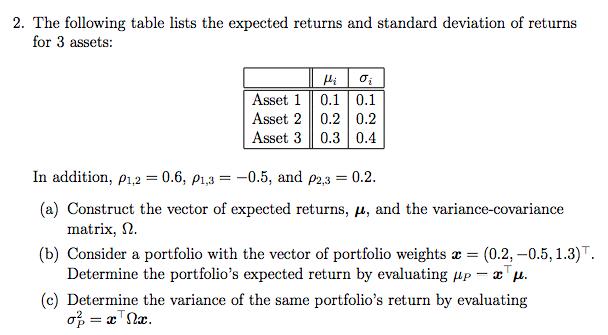

2. The following table lists the expected returns and standard deviation of returns for 3 assets: Asset 1 0.1 0.1 Asset 2 0.2 0.2 Asset 3 0.3 0.4 In addition, p1,2 = 0.6, P1,3 = -0.5, and p2,3 = 0.2. (a) Construct the vector of expected returns, , and the variance-covariance matrix, N. (b) Consider a portfolio with the vector of portfolio weights (0.2, -0.5, 1.3). Determine the portfolio's expected return by evaluating px. (c) Determine the variance of the same portfolio's return by evaluating = xnx.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock