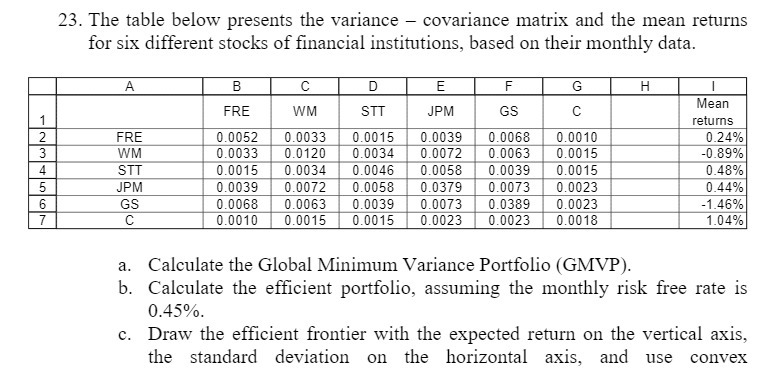

Question: 23. The table below presents the variance - covariance matrix and the mean returns for six different stocks of financial institutions, based on their monthly

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock