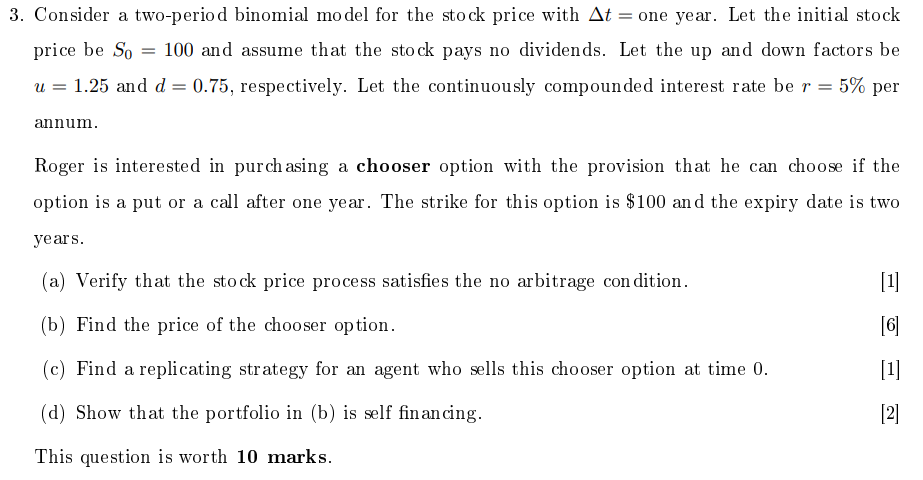

Question: = 3. Consider a two-period binomial model for the stock price with At = one year. Let the initial stock price be so = 100

= 3. Consider a two-period binomial model for the stock price with At = one year. Let the initial stock price be so = 100 and assume that the stock pays no dividends. Let the up and down factors be u = 1.25 and d= 0.75, respectively. Let the continuously compounded interest rate be r = 5% per = annum. Roger is interested in purch asing a chooser option with the provision that he can choose if the option is a put or a call after one year. The strike for this option is $100 and the expiry date is two years. (a) Verify that the stock price process satisfies the no arbitrage condition. [1] (b) Find the price of the chooser option. [6 (c) Find a replicating strategy for an agent who sells this chooser option at time 0. [1] (d) Show that the portfolio in (b) is self financing. [2] This question is worth 10 marks

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts