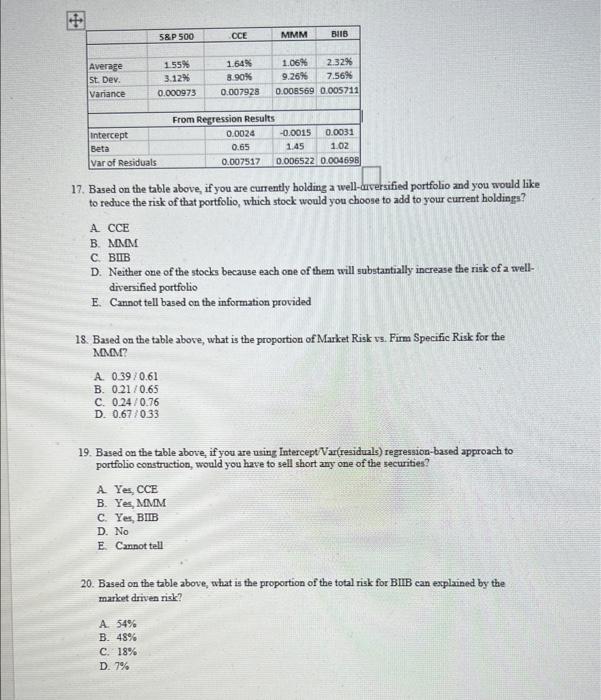

Question: 5&P 500 OCE MMM BIB Average St. Dev. Variance 1 55% 3.12% 0.000973 1.64 8.90% 1.06% 2.32% 9.26% 7.56% 0.008569 0.005711 0.007928 intercept Beta Var

5&P 500 OCE MMM BIB Average St. Dev. Variance 1 55% 3.12% 0.000973 1.64 8.90% 1.06% 2.32% 9.26% 7.56% 0.008569 0.005711 0.007928 intercept Beta Var of Residuals From Regression Results 0.0024 -0.0015 0.0031 0.65 1.45 1.02 0.007517 0.006522 0.004698 17. Based on the table above, if you are currently holding a well-arversified portfolio and you would like to reduce the risk of that portfolio, which stock would you choose to add to your current holdings? ACCE B. MMM D. Neither one of the stocks because each one of the will substantially increase the risk of a well- diversified portfolio E. Cannot tell based on the information provided 18. Based on the table above, what is the proportion of Market Risk vs. Firm Specific Risk for the MMM? A. 0.39/0.61 B. 0.21/0.65 C. 0.24 0.76 D. 0.670.33 19. Based on the table above, if you are using InterceptVar(residuals) regression-based approach to portfolio construction, would you have to sell short any one of the securities? A Yes. CCE B. Yes, MMM C. Yes, BIIB D. No E Cannot tell 20. Based on the table above, what is the proportion of the total risk for BIIB can explained by the market driven risk? A 54% B. 48% C.18% D. 7% 5&P 500 OCE MMM BIB Average St. Dev. Variance 1 55% 3.12% 0.000973 1.64 8.90% 1.06% 2.32% 9.26% 7.56% 0.008569 0.005711 0.007928 intercept Beta Var of Residuals From Regression Results 0.0024 -0.0015 0.0031 0.65 1.45 1.02 0.007517 0.006522 0.004698 17. Based on the table above, if you are currently holding a well-arversified portfolio and you would like to reduce the risk of that portfolio, which stock would you choose to add to your current holdings? ACCE B. MMM D. Neither one of the stocks because each one of the will substantially increase the risk of a well- diversified portfolio E. Cannot tell based on the information provided 18. Based on the table above, what is the proportion of Market Risk vs. Firm Specific Risk for the MMM? A. 0.39/0.61 B. 0.21/0.65 C. 0.24 0.76 D. 0.670.33 19. Based on the table above, if you are using InterceptVar(residuals) regression-based approach to portfolio construction, would you have to sell short any one of the securities? A Yes. CCE B. Yes, MMM C. Yes, BIIB D. No E Cannot tell 20. Based on the table above, what is the proportion of the total risk for BIIB can explained by the market driven risk? A 54% B. 48% C.18% D. 7%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts