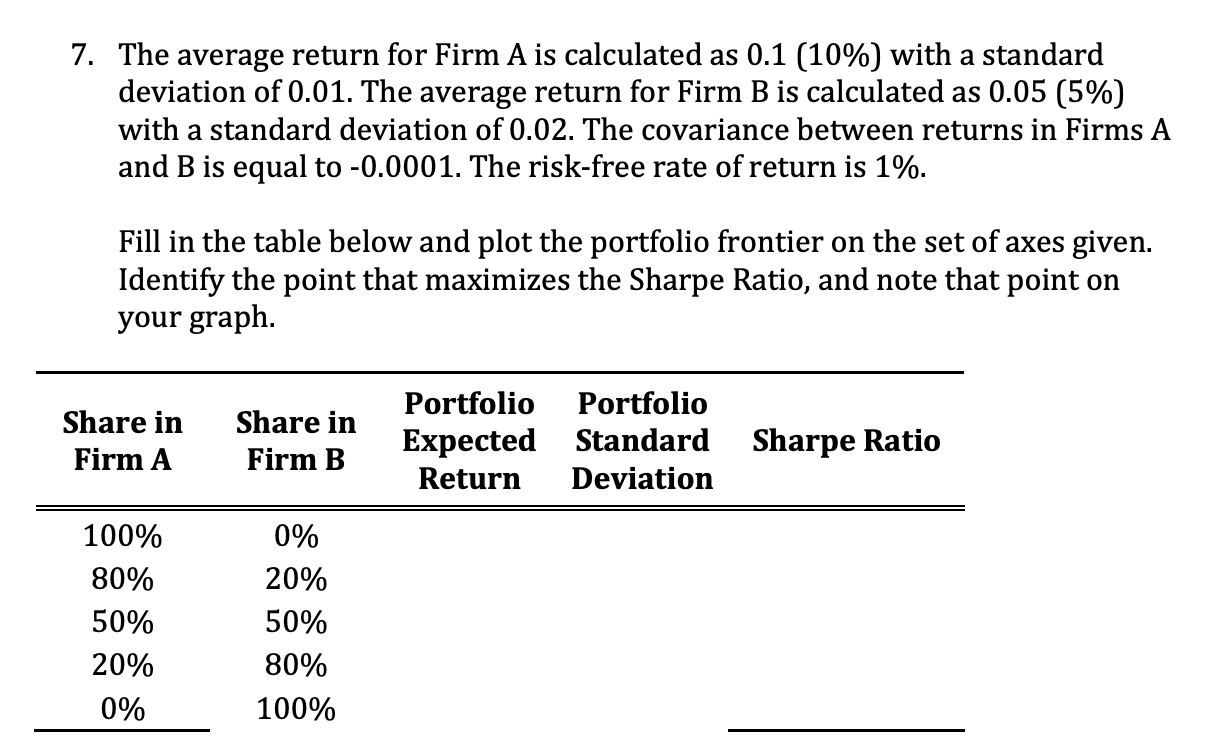

Question: 7. The average return for Firm A is calculated as 0.1 (10%) with a standard deviation of 0.01. The average return for Firm B is

7. The average return for Firm A is calculated as 0.1 (10%) with a standard deviation of 0.01. The average return for Firm B is calculated as 0.05 (5%) with a standard deviation of 0.02. The covariance between returns in Firms A and B is equal to -0.0001. The risk-free rate of return is 1%. Fill in the table below and plot the portfolio frontier on the set of axes given. Identify the point that maximizes the Sharpe Ratio, and note that point on your graph. Share in Firm A Share in Firm B Portfolio Expected Return Portfolio Standard Deviation Sharpe Ratio 100% 80% 50% 20% 0% 0% 20% 50% 80% 100%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock