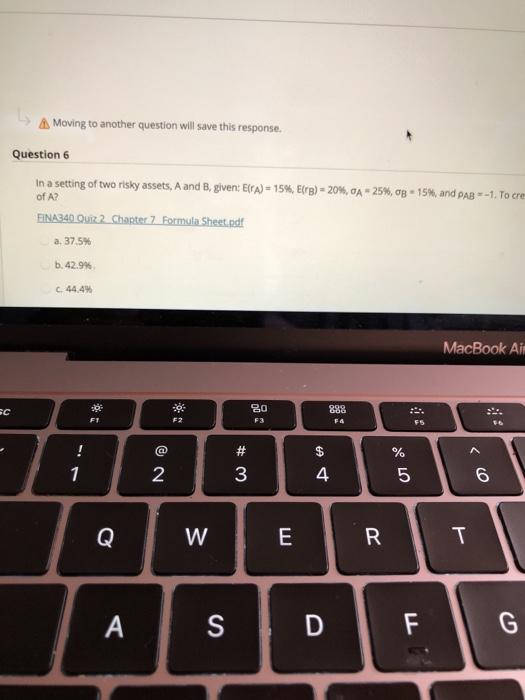

Question: A Moving to another question will save this response. Question 6 In a setting of two risky assets, A and B, given: EFA) = 15%,

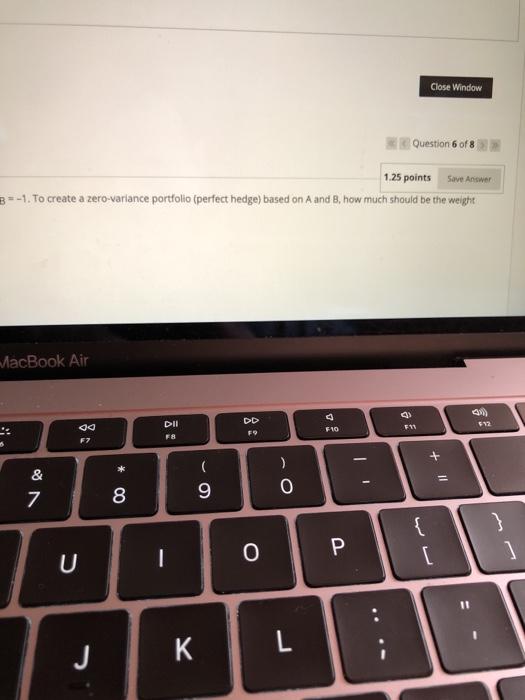

A Moving to another question will save this response. Question 6 In a setting of two risky assets, A and B, given: EFA) = 15%, Erg) - 20%,0A - 25%, og 154, and Pag --1. To cre of A? FINA340 Quiz 2 Chapter 7 Formula Sheet.pdf a. 37.5% b.42.9% C. 44.4 MacBook Ain * C go F3 898 FA FI F2 65 $ % > # ~ 1 2 4 5 6 W E R T A S D F G Close Window Question 6 of 8 1.25 points Save Answer B=-1. To create a zero-variance portfolio (perfect hedge) based on A and B. how much should be the weight MacBook Air DII F10 FM ad F7 FO 6 & 7 * 00 ( 9 ) 0 } { [ I O ] J L

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock