Question: Actuarial Math/ Financial Math Problem: Binomial Tree Pricing Model Bonus Problem 2 (Optional, 25 marks) (*This problem is related to the materials in Topic 1

Actuarial Math/ Financial Math Problem: Binomial Tree Pricing Model

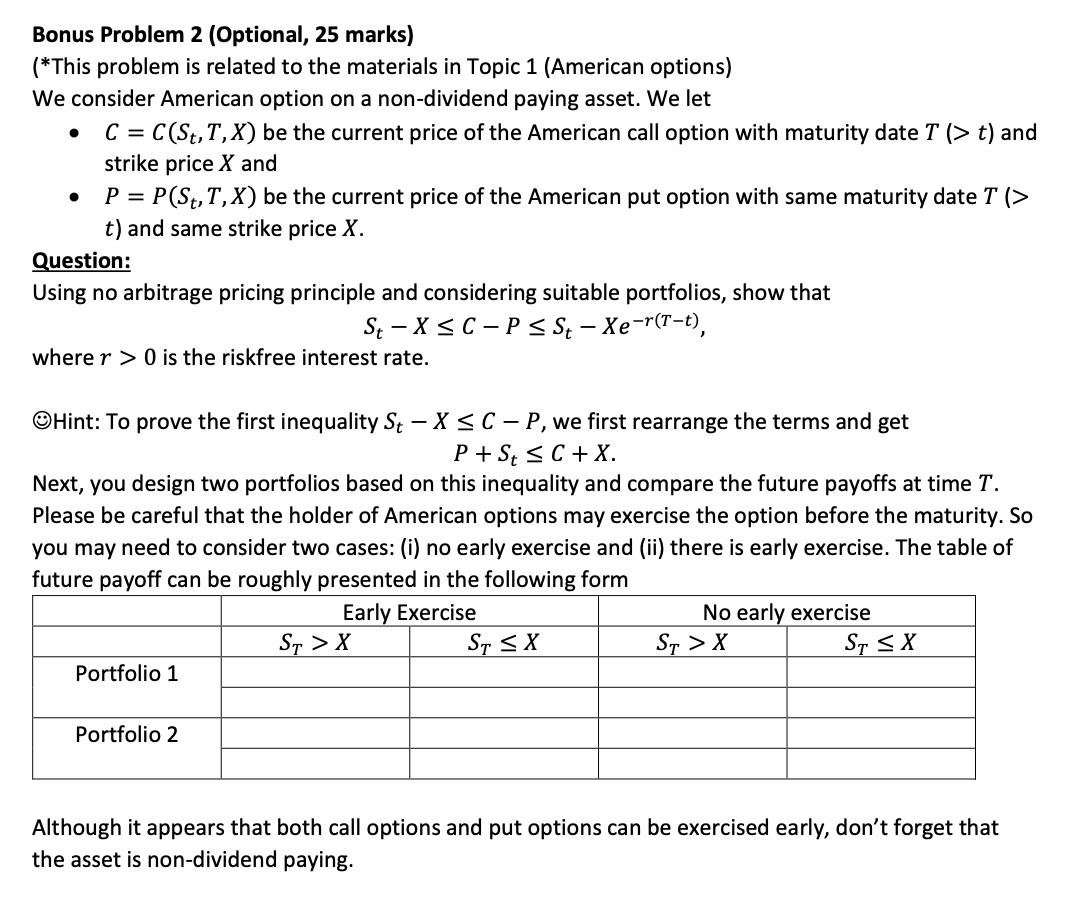

Bonus Problem 2 (Optional, 25 marks) (*This problem is related to the materials in Topic 1 (American options) We consider American option on a non-dividend paying asset. We let C = C(St, T, X) be the current price of the American call option with maturity date T (>t) and strike price X and P = P(St, T, X) be the current price of the American put option with same maturity date T (> t) and same strike price X. Question: Using no arbitrage pricing principle and considering suitable portfolios, show that St - XSC-PS St Xe-r(T-t), wherer > 0 is the riskfree interest rate. Hint: To prove the first inequality St - XSC P, we first rearrange the terms and get P + St X St SX St > X Sy SX Portfolio 1 Portfolio 2 Although it appears that both call options and put options can be exercised early, don't forget that the asset is non-dividend paying. Bonus Problem 2 (Optional, 25 marks) (*This problem is related to the materials in Topic 1 (American options) We consider American option on a non-dividend paying asset. We let C = C(St, T, X) be the current price of the American call option with maturity date T (>t) and strike price X and P = P(St, T, X) be the current price of the American put option with same maturity date T (> t) and same strike price X. Question: Using no arbitrage pricing principle and considering suitable portfolios, show that St - XSC-PS St Xe-r(T-t), wherer > 0 is the riskfree interest rate. Hint: To prove the first inequality St - XSC P, we first rearrange the terms and get P + St X St SX St > X Sy SX Portfolio 1 Portfolio 2 Although it appears that both call options and put options can be exercised early, don't forget that the asset is non-dividend paying

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts