Question: All one question. Part 1 is background info on the company and is asking to estimate the price GCL may get for Fleet as

All one question. Part 1 is background info on the company and is asking to "estimate the price GCL may get for Fleet as of January 1, 2008"?

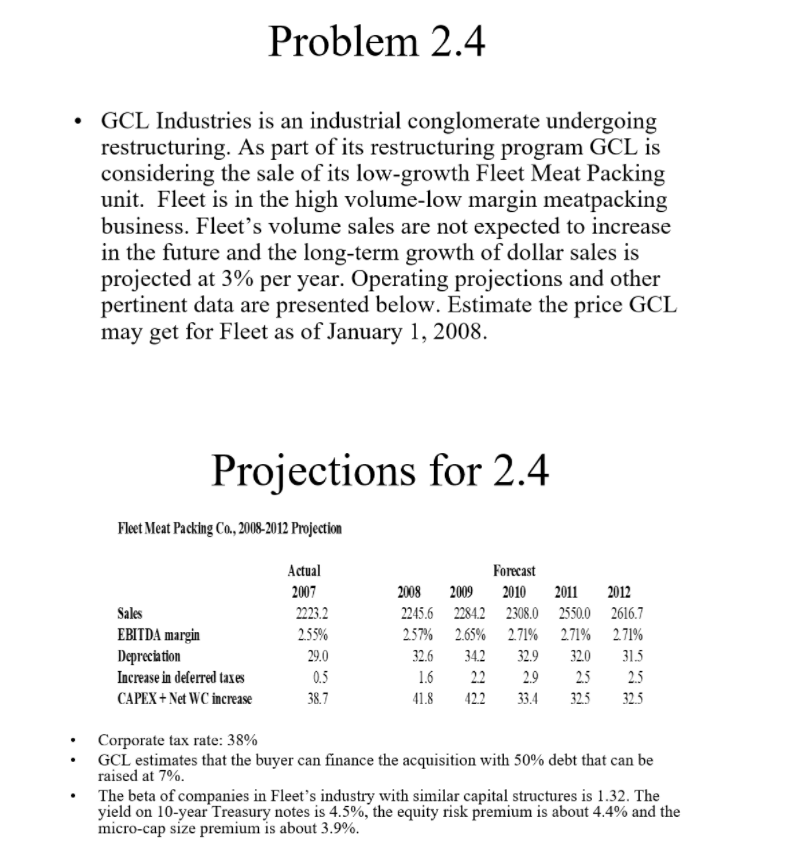

Problem 2.4 GCL Industries is an industrial conglomerate undergoing restructuring. As part of its restructuring program GCL is considering the sale of its low-growth Fleet Meat Packing unit. Fleet is in the high volume-low margin meatpacking business. Fleets volume sales are not expected to increase in the future and the long-term growth of dollar sales is projected at 3% per year. Operating projections and other pertinent data are presented below. Estimate the price GCL may get for Fleet as of January 1, 2008. Projections for 2.4 Fleet Meat Packing Co., 2008-2012 Projection Sales EBITDA margin Depreciation Increase in deferred taxes CAPEX + Net WC increase Actual 2007 2223.2 2.55% 29.0 0.5 387 Forecast 2008 2009 2010 2011 2012 2245.6 2284.22308.0 2550.0 2616.7 257% 2.65% 2.71% 2.71% 2.71% 32.6 34.2 32.9 32.0 315 1.6 2.2 2.9 25 422 33.4 323 32.5 25 11.8 Corporate tax rate: 38% GCL estimates that the buyer can finance the acquisition with 50% debt that can be raised at 7%. The beta of companies in Fleet's industry with similar capital structures is 1.32. The yield on 10-year Treasury notes is 4.5%, the equity risk premium is about 4.4% and the micro-cap size premium is about 3.9%. Problem 2.4 GCL Industries is an industrial conglomerate undergoing restructuring. As part of its restructuring program GCL is considering the sale of its low-growth Fleet Meat Packing unit. Fleet is in the high volume-low margin meatpacking business. Fleets volume sales are not expected to increase in the future and the long-term growth of dollar sales is projected at 3% per year. Operating projections and other pertinent data are presented below. Estimate the price GCL may get for Fleet as of January 1, 2008. Projections for 2.4 Fleet Meat Packing Co., 2008-2012 Projection Sales EBITDA margin Depreciation Increase in deferred taxes CAPEX + Net WC increase Actual 2007 2223.2 2.55% 29.0 0.5 387 Forecast 2008 2009 2010 2011 2012 2245.6 2284.22308.0 2550.0 2616.7 257% 2.65% 2.71% 2.71% 2.71% 32.6 34.2 32.9 32.0 315 1.6 2.2 2.9 25 422 33.4 323 32.5 25 11.8 Corporate tax rate: 38% GCL estimates that the buyer can finance the acquisition with 50% debt that can be raised at 7%. The beta of companies in Fleet's industry with similar capital structures is 1.32. The yield on 10-year Treasury notes is 4.5%, the equity risk premium is about 4.4% and the micro-cap size premium is about 3.9%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts