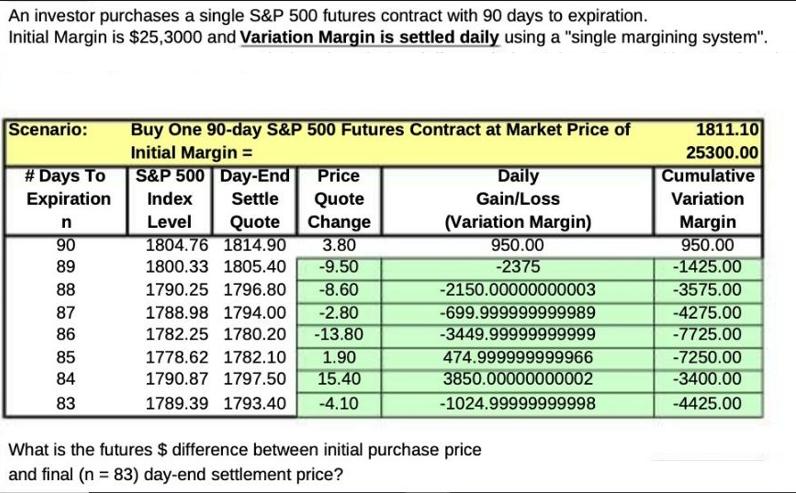

An investor purchases a single S&P 500 futures contract with 90 days to expiration. Initial Margin...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

SOLUTION To calculate the futures dollar difference between the initial purchase price and the final dayend settlement price n 83 we need to consider the variation margin settlements The initial margi... View the full answer

Related Book For

Fundamentals of Investment Management

ISBN: 978-0078034626

10th edition

Authors: Geoffrey Hirt, Stanley Block

Posted Date: