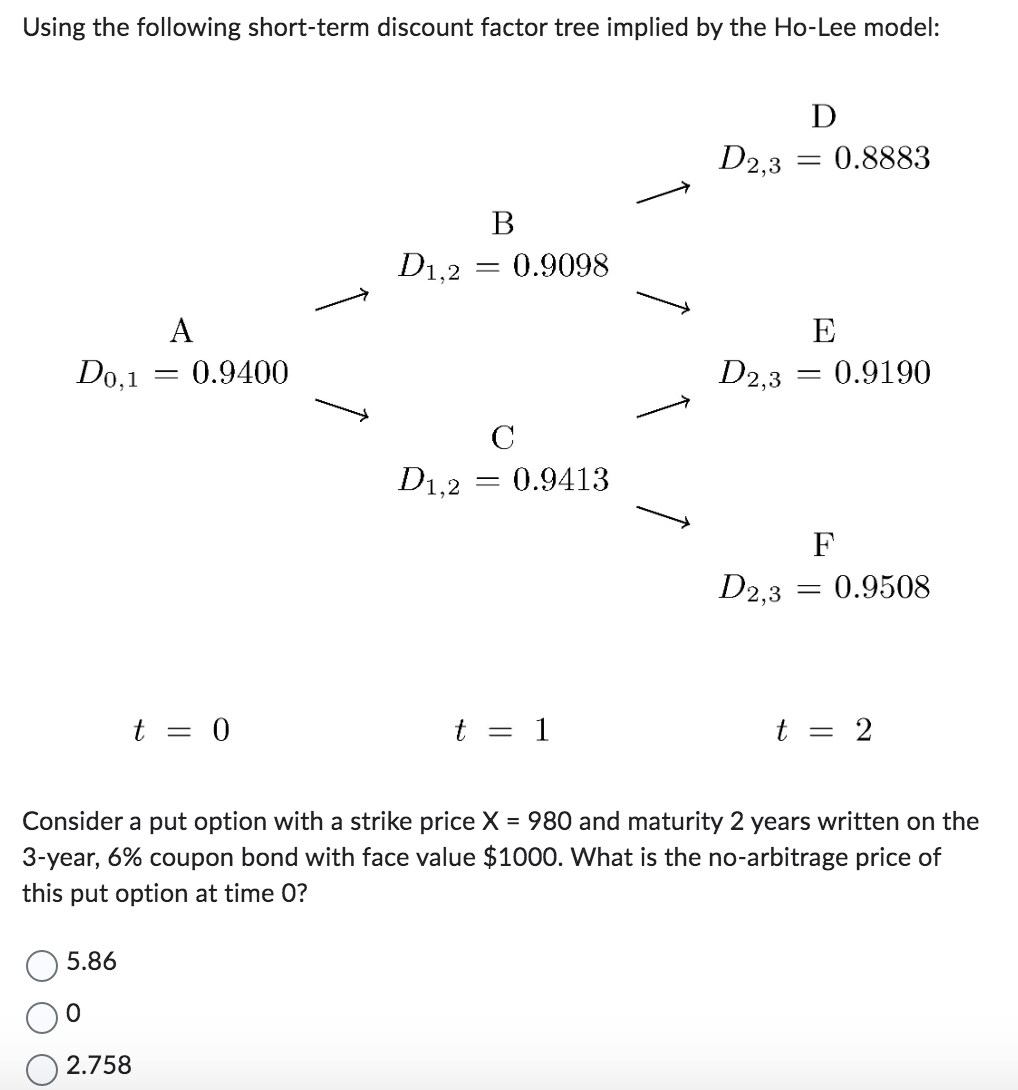

Question: Answer options: 5.86 0 2.758 10.76 Using the following short-term discount factor tree implied by the Ho-Lee model: =0=1=c Consider a put option with a

Answer options:

5.86

0

2.758

10.76

Using the following short-term discount factor tree implied by the Ho-Lee model: =0=1=c Consider a put option with a strike price X=980 and maturity 2 years written on the 3-year, 6% coupon bond with face value $1000. What is the no-arbitrage price of this put option at time 0 ? 5.86 0 2.758

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock