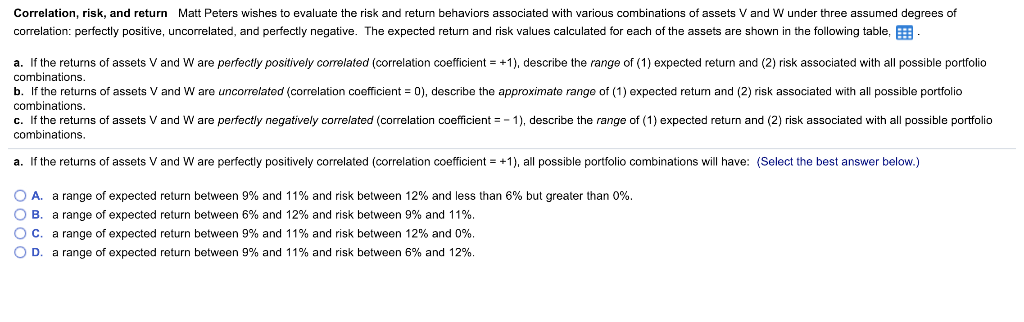

Question: Asset Expected return Risk (standard deviation) V 9% 6% W 11% 12% Correlation, risk, and return Matt Peters wishes to evaluate the risk and return

Asset Expected return Risk (standard deviation)

Asset Expected return Risk (standard deviation)

V 9% 6%

W 11% 12%

Correlation, risk, and return Matt Peters wishes to evaluate the risk and return behaviors associated with various combinations of assets V and W under three assumed degrees of correlation: perfectly positive, uncorrelated, and perfectly negative. The expected return and risk values calculated for each of the assets are shown in the following table. a. If the returns of assets V and W are perfectly positively correlated (correlation coefficient +1), describe the range of (1) expected return and (2) risk associated with all possible portfolio combinations. b. If the returns of assets V and W are uncorrelated (correlation coefficient 0), describe the approximate range of (1) expected retum and (2) risk associated with all possible portfolio combinations c. If the returns of assets V and W are perfectly negatively correlated (correlation coefficient1), describe the range of (1) expected return and (2) risk associated with all possible portfolio combinations. a. If the retuns of assets V and W are perfectly positively correlated (correlation coefficient+1), all possible portolio combinations will have: (Select the best answer below.) O A O B. O C. a range of expected return between 9% and 11% and risk between 12% and less than 5% but greater than 0 a range of expected return between 6% and 12% and risk between 9% and 11%, a range of expected return between 9% and 11% and risk between 12% and 0%. D. a range of expected return between 9% and 11% and risk between 6% and 12%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts