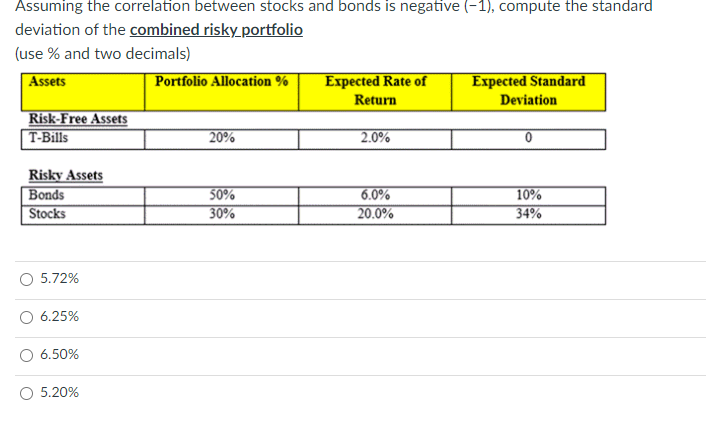

Question: Assuming the correlation between stocks and bonds is negative (-1), compute the standard deviation of the combined risky_portfolio (use % and two decimals) Assets Portfolio

Assuming the correlation between stocks and bonds is negative (-1), compute the standard deviation of the combined risky_portfolio (use % and two decimals) Assets Portfolio Allocation % Expected Rate of Expected Standard Return Deviation Risk-Free Assets T-Bills 20% 2.0% 0 Risky Assets Bonds Stocks 10% 50% 30% 6.0% 20.0% 34% 5.72% 6.25% 6.50% 5.20%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock