Question: Business Financial Management -- Practice Problem 15 15) [18 points] Consider the following table: Securig Expected Return Beta Standard Deviation Risk-free Asset 2% 0% Market

![Business Financial Management -- Practice Problem 15 15) [18 points] Consider](https://s3.amazonaws.com/si.experts.images/answers/2024/06/6665c49a20e89_4976665c499f1c68.jpg)

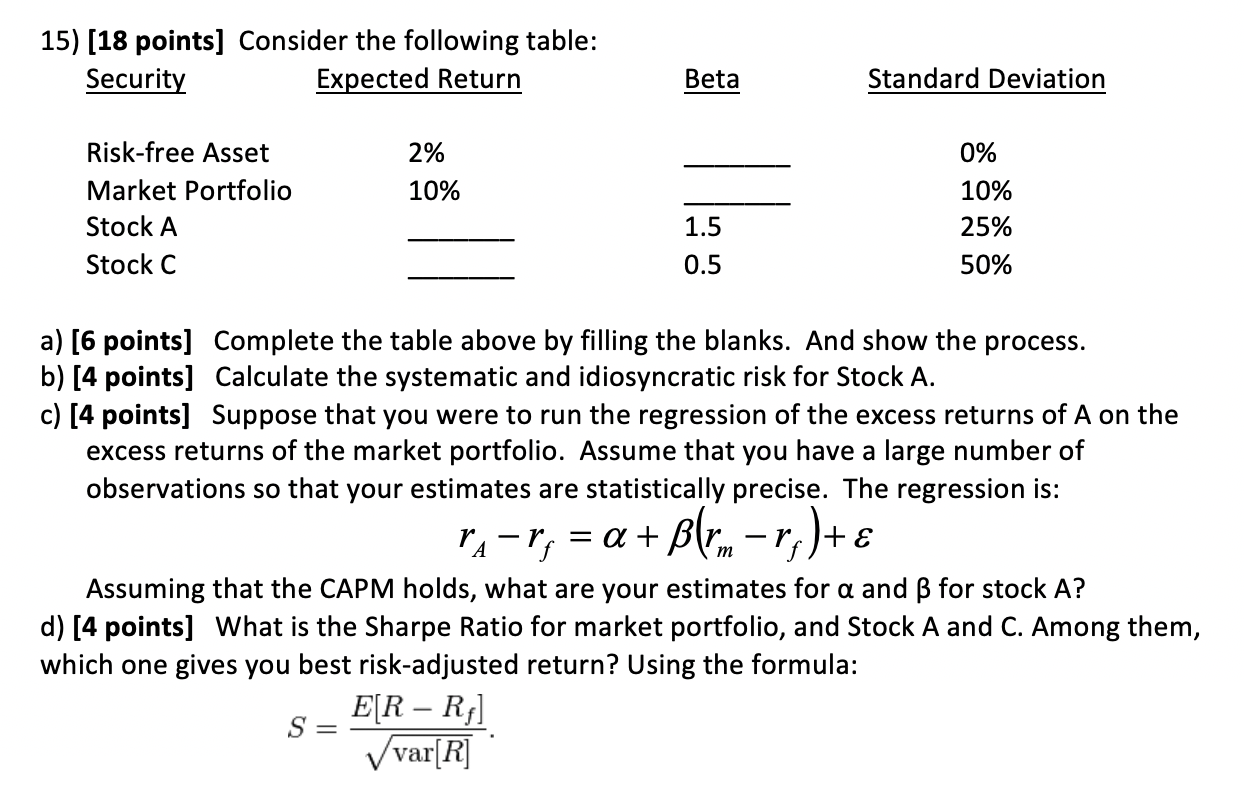

Business Financial Management -- Practice Problem 15

15) [18 points] Consider the following table: Securig Expected Return Beta Standard Deviation Risk-free Asset 2% 0% Market Portfolio 10% 10% Stock A 1.5 25% Stock C 0.5 50% a) [6 points] Complete the table above by filling the blanks. And show the process. b) [4 points] Calculate the systematic and idiosyncratic risk for Stock A. c) [4 points] Suppose that you were to run the regression of the excess returns of A on the excess returns of the market portfolio. Assume that you have a large number of observations so that your estimates are statistically precise. The regression is: rA rf = a+(rm rf)+8 Assuming that the CAPM holds, what are your estimates for a and B for stock A? d) [4 points] What is the Sharpe Ratio for market portfolio, and Stock A and C. Among them, which one gives you best risk-adjusted return? Using the formula: 3 _ ismRf] _ T

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts