Question: Can someone fix the errors? import numpy as np from scipy.optimize import fsolve from scipy.interpolate import interp2d from typing import Callable class BSMPDESolver: def __init__(self,

Can someone fix the errors?

import numpy as np

from scipy.optimize import fsolve

from scipy.interpolate import interp2d

from typing import Callable

class BSMPDESolver:

def __init__(self, spot_price, strike_price, maturity, volatility, interest_rate, dividend_yield, payoff_function: Callable):

self.S = spot_price

self.K = strike_price

self.T = maturity

self.sigma = volatility

self.r = interest_rate

self.q = dividend_yield

self.payoff_function = payoff_function

def solve_pde(self, option_type='European', grid_size=(100, 100)):

M, N = grid_size

dt = self.T / M

dS = (2 * self.S) / N

# Initialize grid

S_values = np.linspace(0, 2 * self.S, N + 1)

t_values = np.linspace(0, self.T, M + 1)

grid = np.zeros((M + 1, N + 1))

# Set boundary conditions

grid[:, 0] = self.payoff_function(S_values)

grid[:, -1] = 0 if option_type == 'European' else self.K - S_values[-1]

# Solve the implicit finite difference scheme

for i in range(M - 1, 0, -1):

A = self._build_coefficient_matrix(grid[i + 1, 1:-1], dS, dt)

B = self._build_rhs_vector(grid[i + 1, 1:-1], dS, dt, S_values[1:-1], t_values[i])

grid[i, 1:-1] = fsolve(A, B)

return S_values, t_values, grid

def _build_coefficient_matrix(self, u_next, dS, dt):

sigma2 = self.sigma**2

r = self.r

q = self.q

alpha = 0.5 * dt * (sigma2 * np.arange(1, len(u_next) + 1)**2 - (r - q) * np.arange(1, len(u_next) + 1))

beta = 1 + dt * (sigma2 * np.arange(1, len(u_next) + 1)**2 + r)

gamma = -0.5 * dt * (sigma2 * np.arange(1, len(u_next) + 1)**2 + (r - q) * np.arange(1, len(u_next) + 1))

A = np.diag(alpha, -1) + np.diag(beta) + np.diag(gamma, 1)

return A

def _build_rhs_vector(self, u_next, dS, dt, S_values, t):

sigma2 = self.sigma**2

r = self.r

q = self.q

b = u_next.copy()

b[0] -= 0.5 * dt * (sigma2 * 1**2 - (r - q) * 1) * (self.payoff_function(S_values[0]) - self.payoff_function(S_values[0] - dS))

b[-1] -= 0.5 * dt * (sigma2 * len(u_next)**2 + (r - q) * len(u_next)) * (self.K - S_values[-1])

return b

# Example usage:

if __name__ == "__main__":

def payoff_function(S):

return np.maximum(0, S - 100) # Example payoff function (call option)

bsm_solver = BSMPDESolver(spot_price=100, strike_price=100, maturity=1, volatility=0.2, interest_rate=0.05, dividend_yield=0.02, payoff_function=payoff_function)

S_values, t_values, option_prices = bsm_solver.solve_pde(option_type='European')

# Print or visualize the results as needed

print(option_prices)

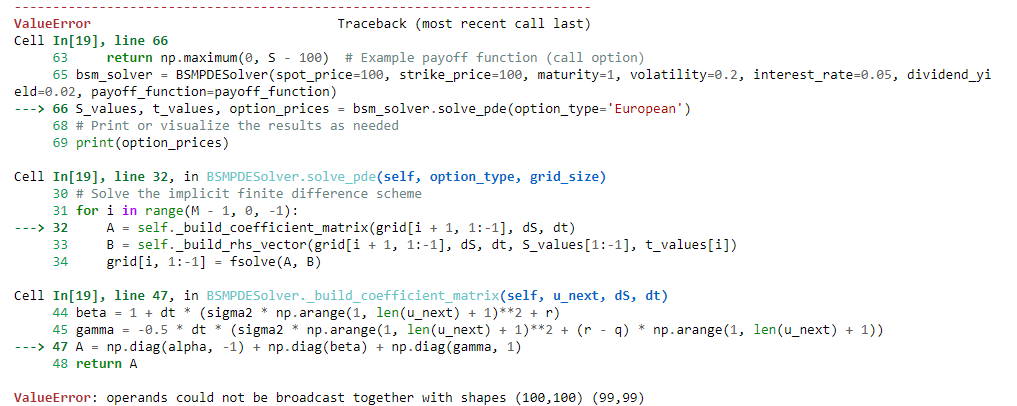

ValueError Traceback (most recent call last) Cell In[19], line 66 63 return np.maximum( , S - 100) \# Example payoff function (call option) 65 bsm_solver = BSMPDESolver(spot_price =100, strike_price =100, maturity =1, volatility =0.2, interest_rate =0.05, dividend_yi eld =0.02, payoff_function=payoff_function) ---> 66 S_values, t_values, option_prices = bsm_solver.solve_pde(option_type='European ') 68 \# Print or visualize the results as needed 69 print(option_prices) Cell In[19], line 32, in BSMPDESolver.solve_pde(self, option_type, grid_size) 30 \# Solve the implicit finite difference scheme 31 for i in range( M1,0,1) : --> 32A= self._build_coefficient_matrix(grid[i +1,1:1],ds,dt) 34grid[i,1:1]=fsolve(A,B) Cell In[19], line 47, in BSMPDESolver._build_coefficient_matrix(self, u_next, dS, dt) 44 beta =1+dt( sigma2 * np.arange \( (\overline{1} \text {, len(u_next) }+1)^{* * 2}+r \) ) 45 gamma =0.5dt( sigma2 np.arange (1, len (unext )+1)2+(rq) np.arange (1, len(u_next) +1)) 48 return A ValueError: operands could not be broadcast together with shapes (100,100)(99,99)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts