Question: can you please help me with option c Consider two securities that pay risk-free cash flows over the next two years and that have the

can you please help me with option c

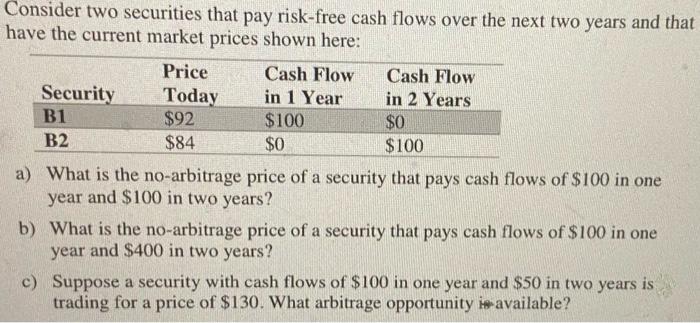

Consider two securities that pay risk-free cash flows over the next two years and that have the current market prices shown here: a) What is the no-arbitrage price of a security that pays cash flows of $100 in one year and $100 in two years? b) What is the no-arbitrage price of a security that pays cash flows of $100 in one year and $400 in two years? c) Suppose a security with cash flows of $100 in one year and $50 in two years is trading for a price of $130. What arbitrage opportunity in available

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock