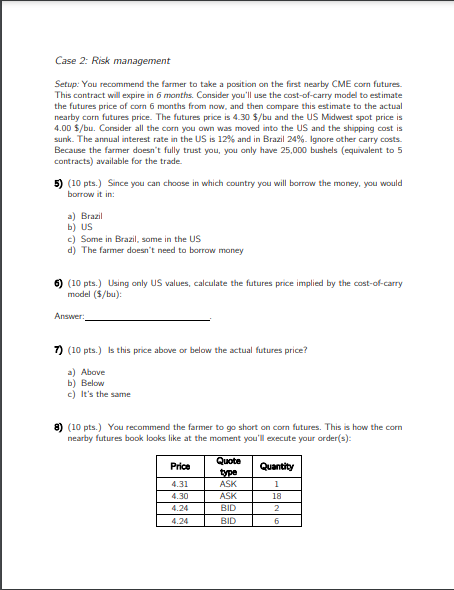

Question: Case 2: Risk management Setup: You recommend the farmer to take a position on the first nearby CME corn futures. This contract will expire in

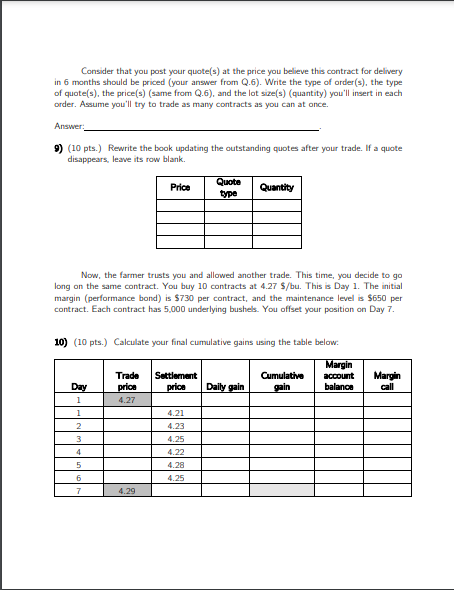

Case 2: Risk management Setup: You recommend the farmer to take a position on the first nearby CME corn futures. This contract will expire in 6 months. Consider you'll use the cost-of-carry model to estimate the futures price of corn 6 months from now and then compare this estimate to the actual nearby corn futures price. The futures price is 4.30 $/bu and the US Midwest spot price is 4.00 $/bu. Consider all the corn you own was moved into the US and the shipping cost is sunk. The annual interest rate in the US is 12% and in Brazil 24%. Ignore other carry costs. Because the farmer doesn't fully trust you, you only have 25,000 bushels (equivalent to 5 contracts) available for the trade 5) (10 pts.) Since you can choose in which country you will borrow the money, you would borrow it in: a) Brazil b) US c) Some in Brazil, some in the US d) The farmer doesn't need to borrow money 6) (10 pts.) Using only US values, calculate the futures price implied by the cost-of-carry model ($/bu) Answer: 7) (10 pts.) Is this price above or below the actual futures price? a) Above b) Below c) It's the same 8) (10 pts.) You recommend the farmer to go short on corn futures. This is how the corn nearby futures book looks like at the moment you'll execute your order(s): Price 4.31 4.30 4.24 4.24 Quote type ASK ASK BID BID Quantity 1 18 2 6 Consider that you post your quote(s) at the price you believe this contract for delivery in 6 months should be priced (your answer from Q.6). Write the type of order(s), the type of quote(s), the price(s) (same from Q.6), and the lot size(s) (quantity) you'll insert in each order. Assume you'll try to trade as many contracts as you can at once. Answer: 9) (10 pts.) Rewrite the book updating the outstanding quotes after your trade. If a quote disappears, leave its row blank. Quote Price Quantity type 91 Now, the farmer trusts you and allowed another trade. This time, you decide to go long on the same contract. You buy 10 contracts at 4.27 $/bu. This is Day 1. The initial margin (performance bond) is $730 per contract, and the maintenance level is $650 per contract. Each contract has 5,000 underlying bushels. You offset your position on Day 7. Margin 10) (10 pts.) Calculate your final cumulative gains using the table below: Margin Trade Settlement Cumulative account Day prica price Daily gain gain balance 1 4.27 1 4.21 2 4.25 4 4.22 5 4.28 4.25 7 4.29 3 6 Case 2: Risk management Setup: You recommend the farmer to take a position on the first nearby CME corn futures. This contract will expire in 6 months. Consider you'll use the cost-of-carry model to estimate the futures price of corn 6 months from now and then compare this estimate to the actual nearby corn futures price. The futures price is 4.30 $/bu and the US Midwest spot price is 4.00 $/bu. Consider all the corn you own was moved into the US and the shipping cost is sunk. The annual interest rate in the US is 12% and in Brazil 24%. Ignore other carry costs. Because the farmer doesn't fully trust you, you only have 25,000 bushels (equivalent to 5 contracts) available for the trade 5) (10 pts.) Since you can choose in which country you will borrow the money, you would borrow it in: a) Brazil b) US c) Some in Brazil, some in the US d) The farmer doesn't need to borrow money 6) (10 pts.) Using only US values, calculate the futures price implied by the cost-of-carry model ($/bu) Answer: 7) (10 pts.) Is this price above or below the actual futures price? a) Above b) Below c) It's the same 8) (10 pts.) You recommend the farmer to go short on corn futures. This is how the corn nearby futures book looks like at the moment you'll execute your order(s): Price 4.31 4.30 4.24 4.24 Quote type ASK ASK BID BID Quantity 1 18 2 6 Consider that you post your quote(s) at the price you believe this contract for delivery in 6 months should be priced (your answer from Q.6). Write the type of order(s), the type of quote(s), the price(s) (same from Q.6), and the lot size(s) (quantity) you'll insert in each order. Assume you'll try to trade as many contracts as you can at once. Answer: 9) (10 pts.) Rewrite the book updating the outstanding quotes after your trade. If a quote disappears, leave its row blank. Quote Price Quantity type 91 Now, the farmer trusts you and allowed another trade. This time, you decide to go long on the same contract. You buy 10 contracts at 4.27 $/bu. This is Day 1. The initial margin (performance bond) is $730 per contract, and the maintenance level is $650 per contract. Each contract has 5,000 underlying bushels. You offset your position on Day 7. Margin 10) (10 pts.) Calculate your final cumulative gains using the table below: Margin Trade Settlement Cumulative account Day prica price Daily gain gain balance 1 4.27 1 4.21 2 4.25 4 4.22 5 4.28 4.25 7 4.29 3 6

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts