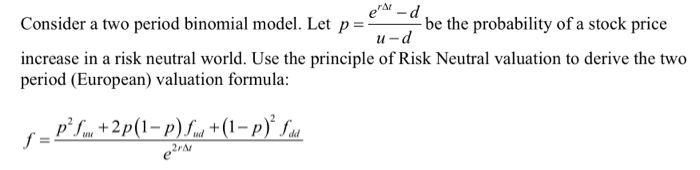

Question: Consider a two period binomial model. Let p=> be the probability of a stock price u-d increase in a risk neutral world. Use the principle

Consider a two period binomial model. Let p=> be the probability of a stock price u-d increase in a risk neutral world. Use the principle of Risk Neutral valuation to derive the two period (European) valuation formula: p? Sm+2p(1-p) f+(1-p) Sad 2211 Consider a two period binomial model. Let p=> be the probability of a stock price u-d increase in a risk neutral world. Use the principle of Risk Neutral valuation to derive the two period (European) valuation formula: p? Sm+2p(1-p) f+(1-p) Sad 2211

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock