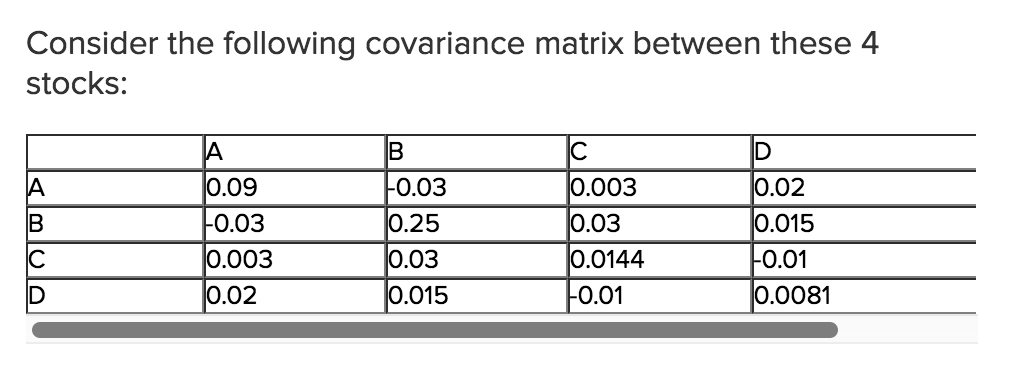

Question: Consider the following covariance matrix between these 4 stocks: 0.09 0.03 0.003 0.02 0.03 0.25 0.03 0.015 0.003 0.03 0.0144 0.02 0.015 0.01 0.0081 0.01

Consider the following covariance matrix between these 4 stocks: 0.09 0.03 0.003 0.02 0.03 0.25 0.03 0.015 0.003 0.03 0.0144 0.02 0.015 0.01 0.0081 0.01 Consider the following covariance matrix between these 4 stocks: 0.09 0.03 0.003 0.02 0.03 0.25 0.03 0.015 0.003 0.03 0.0144 0.02 0.015 0.01 0.0081 0.01

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock