Question: Dear tutor, I would like to know how to this question step by step. Thank you Question 3 Figure 3.1 shows the daily returns on

Dear tutor,

I would like to know how to this question step by step. Thank you

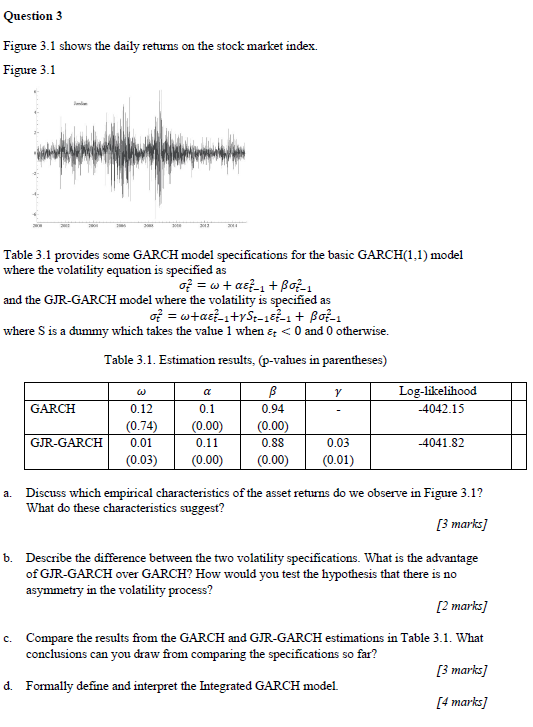

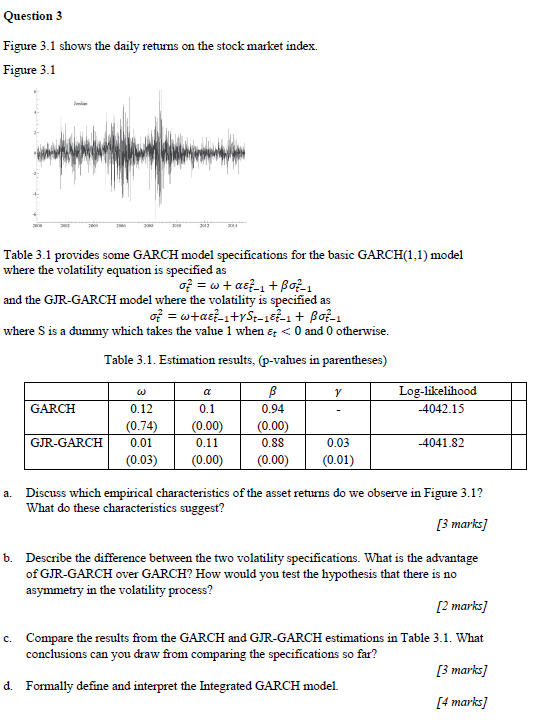

Question 3 Figure 3.1 shows the daily returns on the stock market index. Figure 3.1 Table 3.1 provides some GARCH model specifications for the basic GARCH(1,1) model where the volatility equation is specified as of = wt act_1 + Boz-1 and the GJR-GARCH model where the volatility is specified as of = wtas-ityS-1-1 + Bot-1 where S is a dummy which takes the value 1 when a,

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock