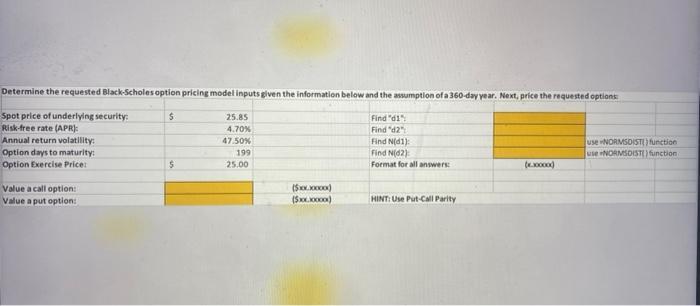

Question: Determine the requested Black-Scholes option pricing model inputs given the information below and the assumption of a 360-day year. Next, price the requested options:

Determine the requested Black-Scholes option pricing model inputs given the information below and the assumption of a 360-day year. Next, price the requested options: $ Spot price of underlying security: Risk-free rate (APR): Annual return volatility: Option days to maturity: Option Exercise Price: Value a call option: Value a put option: $ 25.85 4.70% 47.50% 199 25.00 ($100.000000) ($xx.10000) Find "d1% Find "d2": Find N(1): Find N(62) Format for all answers: HINT: Use Put-Call Parity use NORMSDIST() function use NORMSDIST() function

Step by Step Solution

3.49 Rating (149 Votes )

There are 3 Steps involved in it

To calculate the requested BlackScholes option pricing model inputs and price the options well use t... View full answer

Get step-by-step solutions from verified subject matter experts