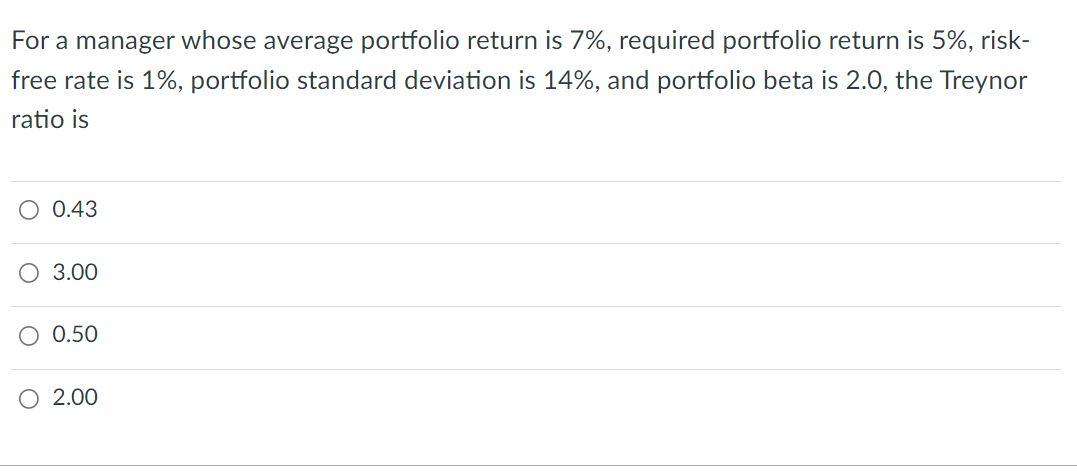

Question: For a manager whose average portfolio return is 7%, required portfolio return is 5%, risk- free rate is 1%, portfolio standard deviation is 14%, and

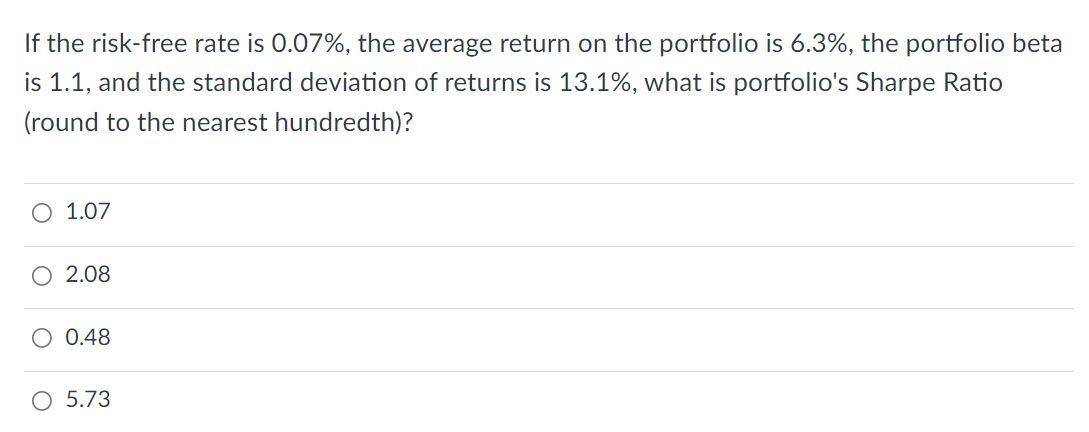

For a manager whose average portfolio return is 7%, required portfolio return is 5%, risk- free rate is 1%, portfolio standard deviation is 14%, and portfolio beta is 2.0, the Treynor ratio is O 0.43 3.00 0.50 O 2.00 If the risk-free rate is 0.07%, the average return on the portfolio is 6.3%, the portfolio beta is 1.1, and the standard deviation of returns is 13.1%, what is portfolio's Sharpe Ratio (round to the nearest hundredth)? 01.07 2.08 0.48 5.73

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock