Question: Form a long butterfly spread using the three call options in the table below. Price DELTA GAMMA THETA VEGA RHO ci X= $90 T =

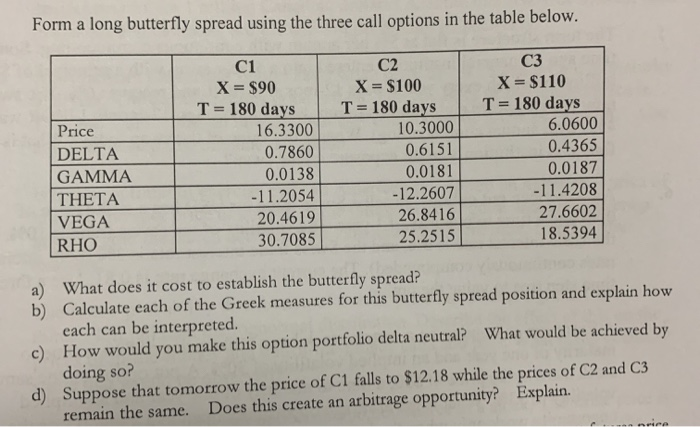

Form a long butterfly spread using the three call options in the table below. Price DELTA GAMMA THETA VEGA RHO ci X= $90 T = 180 days 16.3300 0.7860 0.0138 -11.2054 20.4619 30.7085 C2 X= $100 T= 180 days 10.3000 0.6151 0.0181 -12.2607 26.8416 25.2515 C3 X = $110 T= 180 days 6.0600 0.4365 0.0187 -11.4208 27.6602 18.5394 a) What does it cost to establish the butterfly spread? b) Calculate each of the Greek measures for this butterfly spread position and explain how each can be interpreted. c) How would you make this option portfolio delta neutral? What would be achieved by doing so? d) Suppose that tomorrow the price of C1 falls to $12.18 while the prices of C2 and C3 remain the same. Does this create an arbitrage opportunity? Explain. vire Form a long butterfly spread using the three call options in the table below. Price DELTA GAMMA THETA VEGA RHO ci X= $90 T = 180 days 16.3300 0.7860 0.0138 -11.2054 20.4619 30.7085 C2 X= $100 T= 180 days 10.3000 0.6151 0.0181 -12.2607 26.8416 25.2515 C3 X = $110 T= 180 days 6.0600 0.4365 0.0187 -11.4208 27.6602 18.5394 a) What does it cost to establish the butterfly spread? b) Calculate each of the Greek measures for this butterfly spread position and explain how each can be interpreted. c) How would you make this option portfolio delta neutral? What would be achieved by doing so? d) Suppose that tomorrow the price of C1 falls to $12.18 while the prices of C2 and C3 remain the same. Does this create an arbitrage opportunity? Explain. vire

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts