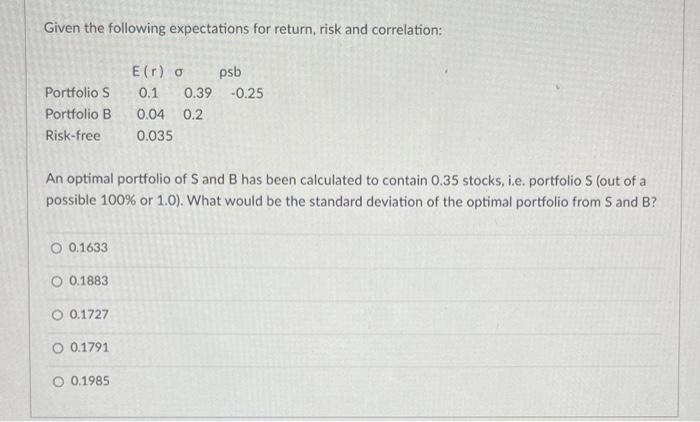

Question: Given the following expectations for return, risk and correlation: An optimal portfolio of S and B has been calculated to contain 0.35 stocks, i.e. portfolio

Given the following expectations for return, risk and correlation: An optimal portfolio of S and B has been calculated to contain 0.35 stocks, i.e. portfolio S (out of a possible 100% or 1.0 ). What would be the standard deviation of the optimal portfolio from S and B ? 0.1633 0.1883 0.1727 0.1791 0.1985

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock