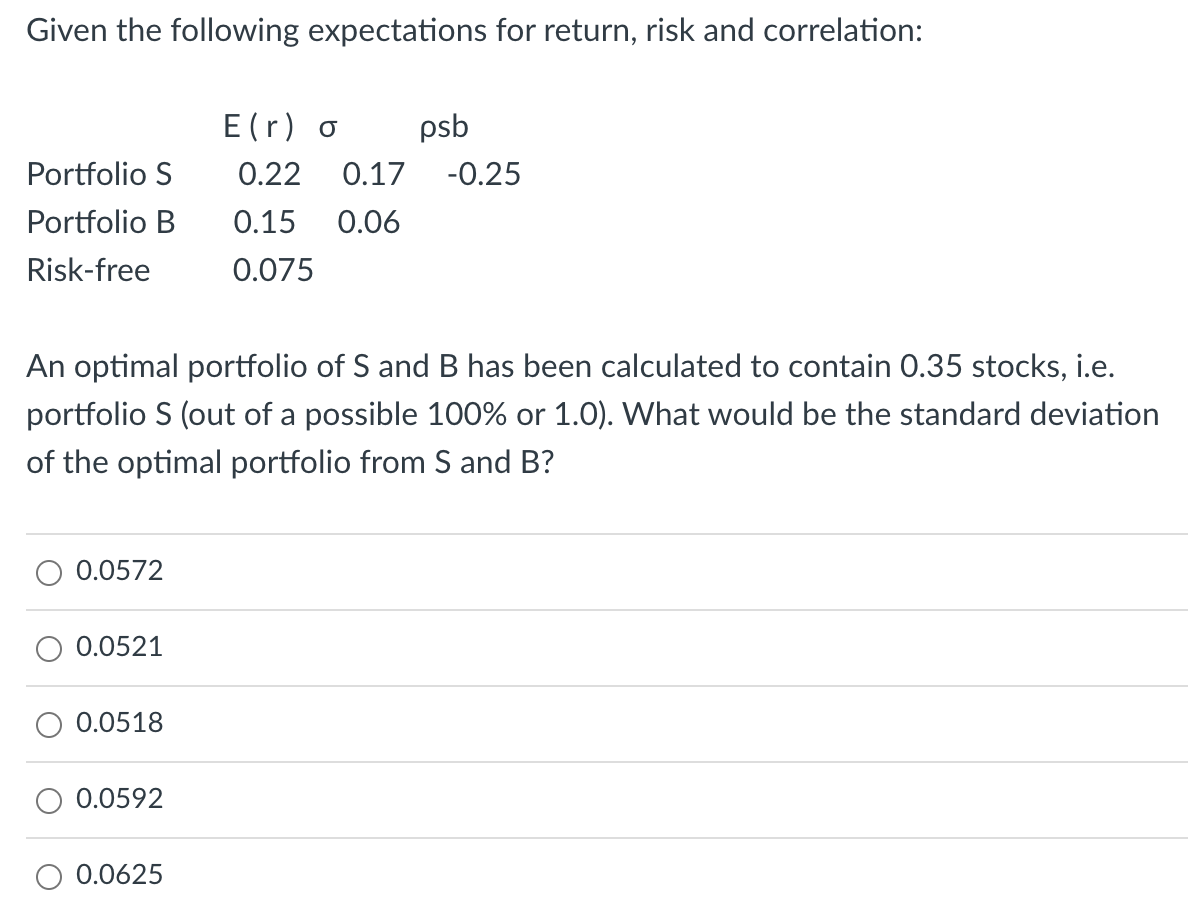

Question: Given the following expectations for return, risk and correlation: E (r) o psb Portfolio S 0.22 0.17 -0.25 Portfolio B 0.15 0.06 Risk-free 0.075 An

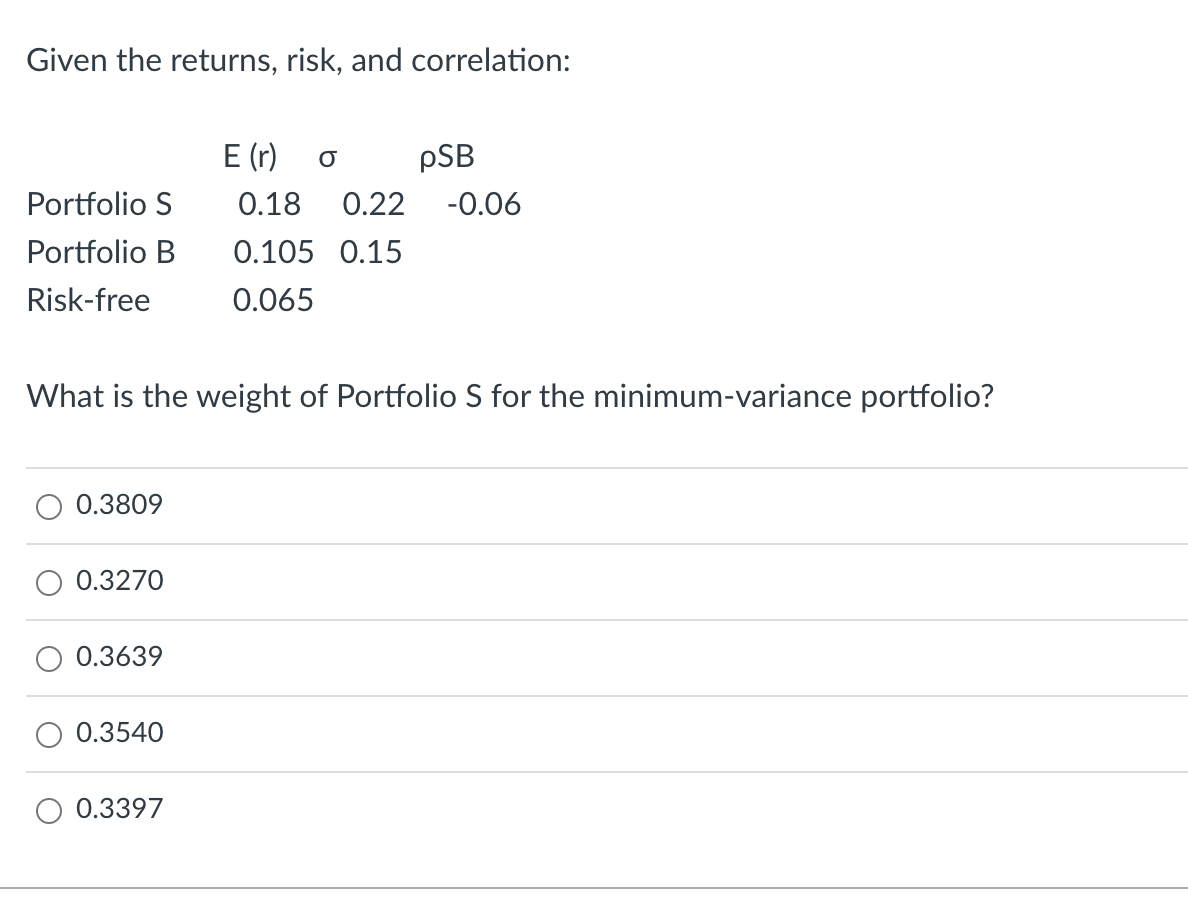

Given the following expectations for return, risk and correlation: E (r) o psb Portfolio S 0.22 0.17 -0.25 Portfolio B 0.15 0.06 Risk-free 0.075 An optimal portfolio of S and B has been calculated to contain 0.35 stocks, i.e. portfolio S (out of a possible 100% or 1.0). What would be the standard deviation of the optimal portfolio from S and B? 0.0572 0.0521 0.0518 0.0592 0.0625 Given the returns, risk, and correlation: E (r) O pSB Portfolio S 0.18 0.22 -0.06 Portfolio B 0.105 0.15 Risk-free 0.065 What is the weight of Portfolio S for the minimum-variance portfolio? 0.3809 0.3270 0.3639 0.3540 0.3397

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock